Q4 2025 Earnings Call Transcript")

")

I cover a lot of companies where management knows the industry very well. But similar to HighPeak Energy, Inc. (NASDAQ:HPK), that knowledge often does not include up-to-date information on the debt markets or sometimes how the finance world works in general. That lack of knowledge sometimes leads to a “last minute” rush to get accomplished what should have been accomplished long before now.

I had written previously that this management built and sold companies before. But things change, and a failure to anticipate change can have costs. One of those potential costs that probably could have been avoided was the recent offering of common stock.

Management furthermore tried to reduce the significance of the debt issues by purchasing a lot of common stock. The market reaction to this was of course to send the stock price higher. But unless management gets this debt issue “under control” and “out of the way,” those gains could easily erase.

Most likely the common stock offering was done because the debt market has been very sticky about lending money to oil and gas startups. Even though management has a history, it is very possible that they were engaging in a strategy that the market no longer accepts. Therefore, it would have behooved management to have whatever equity and debt raises needed well ahead of time.

The other possibility here is that interest rates have been rising steadily as the inflation battle is fought. Management may have wanted to wait out that battle in the hopes that interest rates may decline.

There are other possibilities as well. But whatever the reason, waiting for a deadline is not good in the finance world and can cost either through the issuance of equity, as just happened or a higher interest rate on whatever debt is going to be negotiated. In this case, there was a clause about a preliminary retirement of some notes by June 30. Since that deadline was missed, there most likely will be a fee charged and perhaps another half point on the eventual interest rate.

None of this is, of course, a company wrecker. But all of it is costs and possibly some ill-will that could have been avoided by managing the finances a little better.

Oftentimes, company management (and hence company building) is like a game of chess in that the winner of the game of chess is said to be the one that makes the second-to-last mistake. Many managements do well if they can do a lot more good than damage.

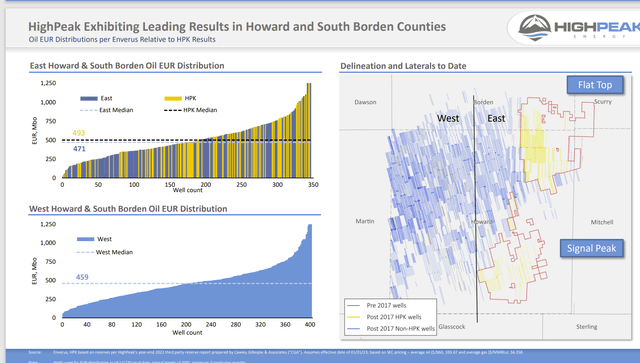

Howard County Location

In this case, the company has leases in a fantastic location (and a lot of them for the size of the company).

HighPeak Energy Lease Location Map And Well Characteristics (High Peak Energy Corporate Presentation May 15, 2023)

This location is good enough that some of the larger companies I follow are now either buying or looking to buy in the area. Paybacks are fast enough that you can borrow to drill with the idea of reaching a very comfortable level of production that easily repays the debt back. In fact, this was long the preferred way to convert from a startup to an ongoing upstream company.

However, the debt market put an end to this idea, probably sometime after the 2018 oil price rally unexpectedly aborted (after a short duration). Then came the 2020 challenges, which really put an end to borrowing for much of the industry in general. Simply stated, the costs to do what used to be easy to do became too high to be viable. It is possible that this management is just finding that out.

Management tried to sell some notes on the private market. But that appears to be taking more time than management planned. In fact, it may not be possible to do such an offering on anything close to the terms that management envisioned.

That puts management back to square one. Usually when you end up where you started, it is time to do a stock offering to boost the company liquidity. That would strengthen the company position considerably. That is where we are now. Whether this offering will be enough is anyone’s guess.

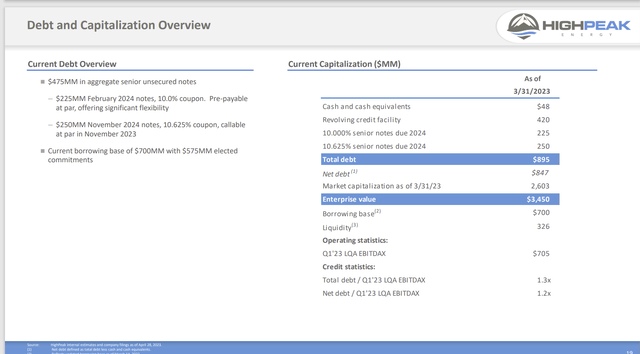

Debt Ratios

The company has middling debt ratios. But the debt market wants good debt ratios at considerably more conservative pricing than is the current case.

HighPeak Energy Debt And Capitalization Summary (High Peak Energy May 15, 2023, Corporate Presentation)

To me, it looks as though management thought the company could handle more debt to get to a better production level that would optimize costs. Instead, management is likely discovering that they were lucky to get this far along with that strategy. The debt market no longer likes that idea at all, regardless of the feasibility.

Most likely investors will have to wait to see the effects of the refinancing to determine things like exit rate and future growth. To me, the strategy that management explained was very old-fashioned; so, it did not meet current debt market expectations. Therefore, there could be a new plan once all of this gets settled.

It should be noted that generally banks do not cause an extreme solution. Instead, they normally charge a fee and raise the interest rate. The real worry would be that the debt market becomes more intractable the longer this goes on because management is overplaying its hand.

As long as management and the banks get to a likely agreeable point and the debt gets refinanced accordingly, then the outlook here remains bright. The company did suffer a few dents and bruises from this experience. But many small company managements often make a few mistakes along the way.

The key for investors to determine is if management is mainly correct or if there are such serious management defects that the company has a reasonable chance of not surviving the (or thriving during) the mistakes that management is capable of.

Summary

HighPeak Energy, Inc. has some of the best acreage in Texas. For the price management paid, this acreage is likely to turn out to be an excellent investment. The acreage appears to be very comparable to Reeves County. But Reeves County acreage is far more expensive.

The acreage that the company has can also keep management very busy for a long time. Since the acreage appears to be very profitable, that should be good news.

That alone should mean that the company can absorb a few financing errors and still have a rather robust future. As long as that is the case, then this issue is likely to be a strong buy when the debt-financing issues get resolved.

However, when this ends, management needs to demonstrate that they will not do anything close to this a second time. The market has changed, and management needs to change with the new conditions. That should be straightforward. But time will tell.

It should be noted that management did not start this company to meet some of the pricing objectives out there. Most managements go into business to “make a killing.” A typical example of that would be a goal of the stock price to triple over a five-year period, which is a 25% compounded return (roughly).

Now, HighPeak Energy, Inc. management could certainly fall short. But given the past history of this management building and selling companies for a decent profit, the thing for most shareholders to consider (even with the debt issues) is to consider hanging on until management sells the company. They are very likely to be pleased at the results even though the debt issues raise the risk at the current time.

Read the full article here

Q4 2025 Earnings Call Transcript")

")

")

")