")

")

Introduction

On June 5, I wrote an article titled CF Industries: Why I Believe In A Return To All-Time Highs. Since then, CF Industries (NYSE:CF) has risen 22%, beating the S&P 500 by roughly 17 points.

Since early June, I have written a number of articles on potash and phosphate fertilizer producers that all showed the same developments: falling prices but a strong demand outlook.

The same goes for CF Industries. While margins are currently under fire from lower nitrogen fertilizer prices, the company is seeing strong demand thanks to improved affordability and global trade issues. On top of that, it’s the go-to stock to benefit from a shift in natural gas price differentials between Europe and North America, as North America is one of the few places in the world where affordable nitrogen can be produced to feed the world (literally).

In this article, we’ll discuss all of these issues and assess my call that CF is poised to retake its all-time high the moment it gets support from higher prices/margins.

What Happened In 2Q23/1H23?

The second quarter wasn’t great – although it depends on how you look at it.

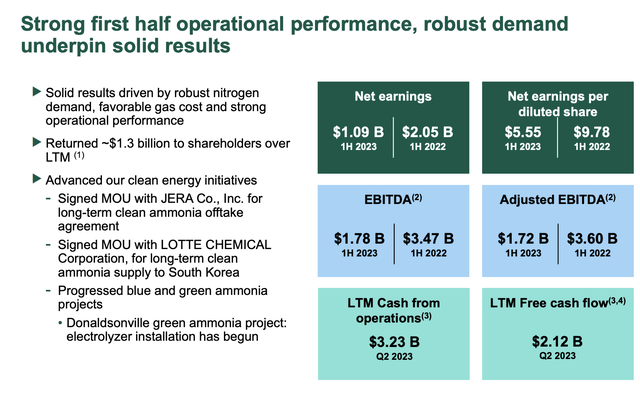

In the first half of 2023, CF Industries reported net earnings attributable to common stockholders of around $1.1 billion, which translates to $5.55 per diluted share. The company’s EBITDA fell to $1.8 billion, while adjusted EBITDA was $1.7 billion.

These numbers are way lower than the numbers the company revealed in the first six months of 2022.

CF Industries

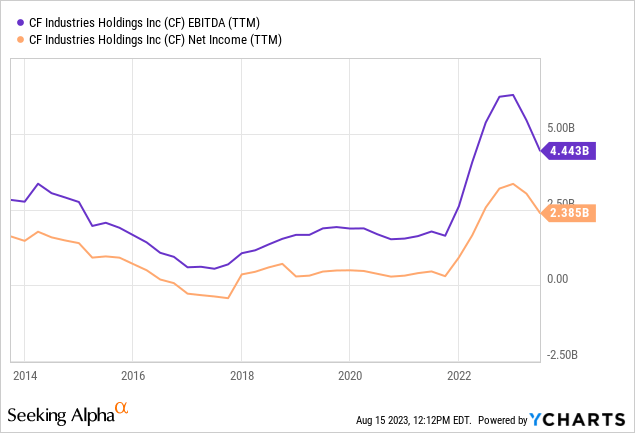

However, when looking at the bigger picture, we see that CF is still crushing the numbers it reported before Russia set foot in Ukraine last year – excluding Crimea, which it annexed a while ago.

Moreover, trailing 12-month net cash from operations came in at $3.2 billion, with free cash flow reaching $2.1 billion.

During its earnings call, the company emphasized its ability to sell more products than it produced, leading to low inventories by the end of the first half.

This efficient management and utilization of resources have positioned CF Industries well for the remainder of 2023 and extending into 2024.

This brings me to the company’s outlook, which is way more important than what happened in 2Q23. After all, everyone knew that the second quarter/first half would be weak due to lower margins. It’s why the company was able to beat GAAP EPS estimates of $2.10 by $0.60.

The Outlook Remains Rock Solid

Let’s start with energy differentials – my favorite topic, as it includes energy and agriculture fundamentals.

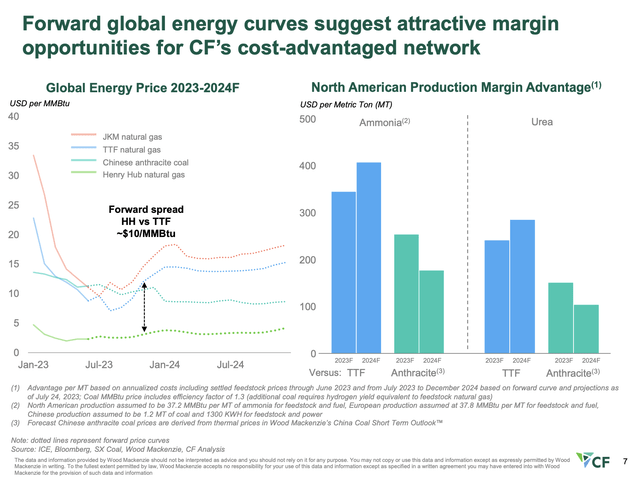

In its 2Q23 earnings call, CF Industries noted that the global nitrogen cost curve has steepened due to changes in the energy markets, providing the company’s North American manufacturing network with a distinct margin advantage.

The overview below shows a margin advantage of $300 to $400 per ton compared to European and high-cost Asian production. This advantageous position, combined with optimal operating rates and network flexibilities, positions CF Industries to drive robust cash generation for years to come.

CF Industries

The company intends to utilize this strong financial foundation to pursue disciplined growth investments while returning substantial capital to shareholders.

The energy price differentials are a big issue and could get much wider if Europe gets a cold winter. After all, Europe is fully dependent on LNG imports, as it doesn’t get Russian gas anymore.

It’s also one of the reasons why CF Industries is looking to close its plant in the United Kingdom.

CF Industries recently proposed the permanent closure of the ammonia plant at the Billingham complex in the U.K. The decision is primarily driven by the structural disadvantage faced by European ammonia production due to high energy and carbon costs.

Google News

So far, CF Industries has been importing ammonia since late 2022 for the production of UAN fertilizer and nitric acid at the site.

This move is expected to have a positive impact on gross margins when compared to producing ammonia at Billingham.

Given these developments, my opinion is that energy differentials are the biggest bull case going forward.

It also helps that other factors are bullish for the company.

For example, during its earnings call, the company highlighted a solid spring application season, indicating a strong global demand outlook for the second half of the year.

Despite some customers deferring purchases until the last moment, North America experienced substantial demand with increased planted acres for corn and wheat compared to the previous year.

Notably, net imports were lower than before, leading to the belief that North American inventory levels are historically low and in need of replenishment. CF’s own numbers confirm this.

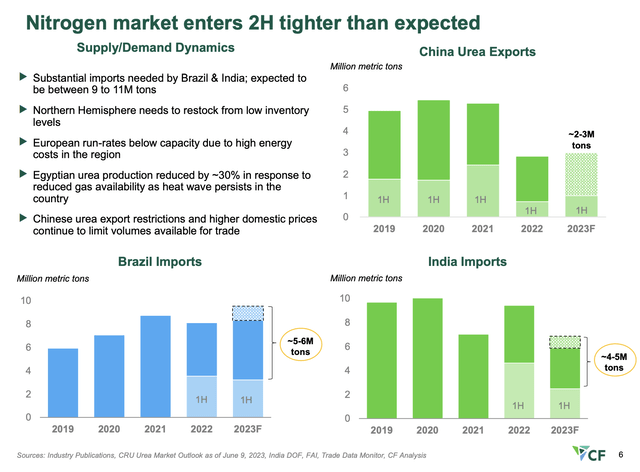

Furthermore, this trend is emphasized by the anticipated competition between India and Brazil for urea in preparation for their upcoming planting season.

CF Industries

As projected, Brazil is seeking 5 to 6 million more tons of urea, while India aims to secure another 4 to 5 million tons by year-end.

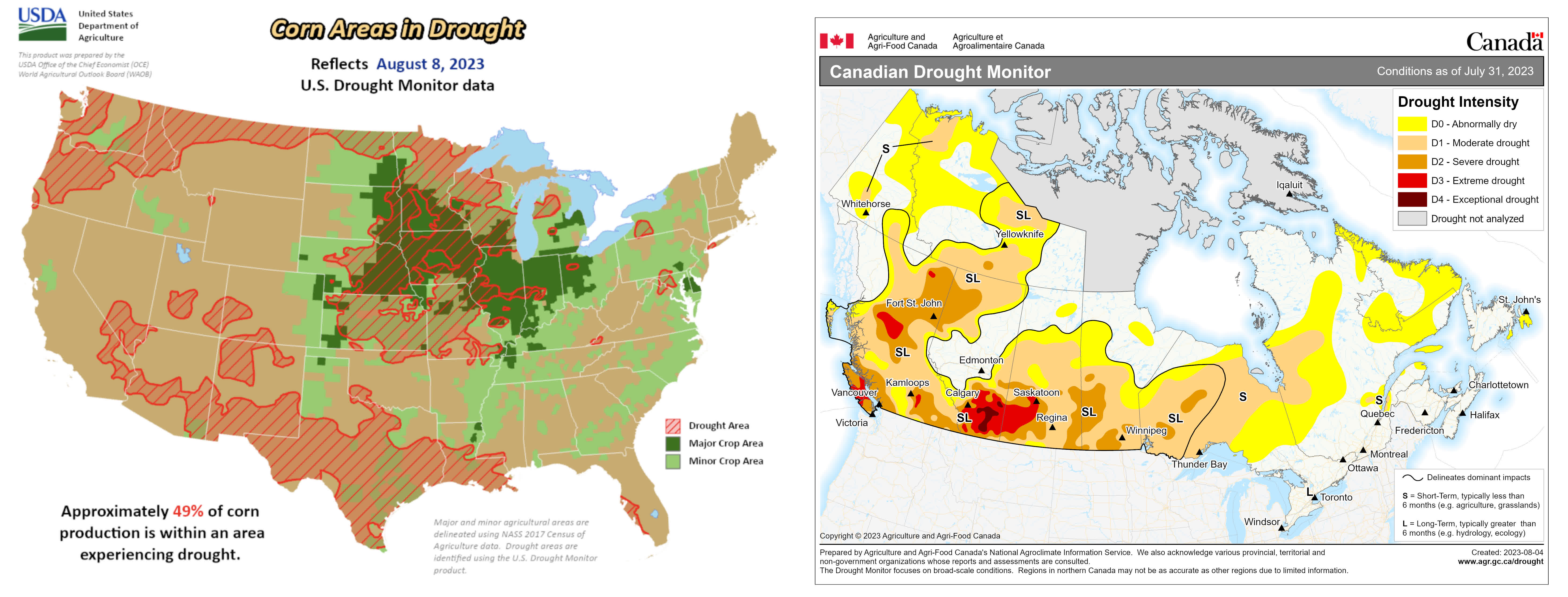

On top of that, the company saw that the positive farm economics landscape continues to drive strong demand. Despite a consensus expectation for slight improvements in global grain stocks for 2023, factors such as drought in the United States and ongoing effects of the Ukraine conflict are maintaining attractive grain prices for farmers.

The chart below shows severe droughts in major crop areas in both the United States and Canada.

USDA, Government of Canada

These market dynamics have led to a surge in urea spot prices through July, subsequently impacting other nitrogen-based products.

CF Industries capitalized on this demand, as it secured domestic and export sales orders into the fourth quarter.

The company also successfully raised prices for subsequent layers and achieved goals for the initial UAN fill offer in North America.

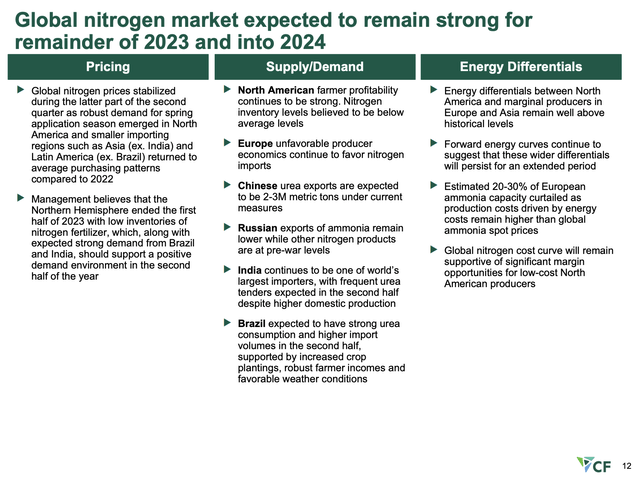

On top of favorable demand developments, the company also benefits from supply constraints.

CF Industries

For example, China is expected to participate in upcoming India urea tenders, which is indicative of strong domestic demand that competes for available shipment volume.

Meanwhile, Russian nitrogen tons continue to enter the global market, albeit with limited buyers in regions like Brazil and the United States.

European ammonia production remains below normal due to unfavorable natural gas prices, making the region less competitive on a global scale, as we already briefly discussed.

Valuation

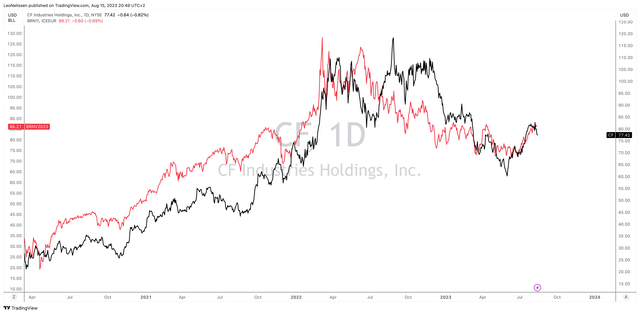

CF had a great run in the past few months. Despite strong fundamentals, the stock is now running into some resistance. As we can see below, this is caused by lower energy prices (the red line shows the Brent crude oil price). Economic growth fears from China are currently causing investors to re-assess what industrial nitrogen demand might look like in the future.

TradingView (CF, Brent Crude Oil)

While the uptrend might be bumpy, I believe that CF Industries is on its way to an all-time high.

I stick to what I wrote in my prior article:

I’m looking for prices between $90 and $100 with a longer-term upside to $120 and $150. That is based on my belief that natural gas prices will enter a long-term uptrend the moment economic growth expectations bottom.

Furthermore, I do not believe that trade restrictions will be eased, which gives CF Industries long-term benefits in both volumes (sales) and pricing.

However, as bullish as the bull case may be, please be careful when trading or investing in CF. CF is highly volatile, and we’re not out of the woods yet.

We could see a 10-20% decline before we move higher again.

My strategy is to keep CF long-term. I started buying fertilizers in 2020, and I don’t expect to sell them anytime soon. I add more on larger corrections as long as my bull case remains intact.

Right now, that seems to be the case.

Takeaway

Despite a somewhat challenging second quarter, CF Industries has navigated energy differentials and market dynamics quite successfully.

The favorable energy cost position in North America, combined with efficient resource management, places the company in a robust cash generation position.

Additionally, the strong global demand outlook for fertilizer, driven by factors like solid spring application seasons and international competition, bodes well for CF Industries.

While market volatility persists, I maintain my long-term perspective on CF Industries.

As energy prices and demand dynamics continue to evolve, the company’s potential for growth and recovery to all-time highs remains compelling.

While short-term fluctuations may occur, my strategy revolves around retaining my CF investments, capitalizing on corrections, and trusting in the bullish trajectory that lies ahead.

Read the full article here

")

")

2026-04-01")

")

")

")

")