")

")

In this article we discuss the latest quarterly results from the Business Development Company Blackstone Secured Lending (NYSE:BXSL). The company delivered a 3.5% total NAV return, outperforming the sector once again. Our last update mentioned “significant dividend upside” in the title which has now translated into a 10% base dividend raise.

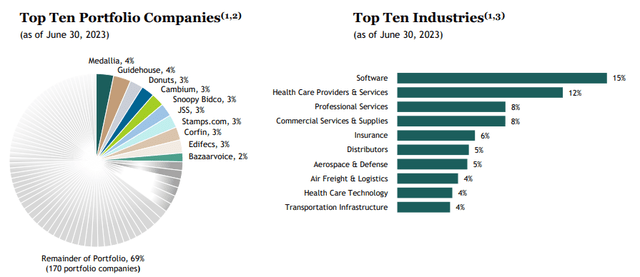

BXSL is one of the largest BDCs with a focus on upper middle-market borrowers. It has the largest exposures to software and healthcare companies, something we see across most other BDCs.

Blackstone

Shortly after reporting results BXSL announced a share offering. On the call, management said that they expect it to be a part of their process in the future if the price remains above the NAV. This is quite common in the BDC space and is a win-win for both management and shareholders. We took the opportunity to move back to BXSL after rotating out earlier.

BXSL is trading at a 4% premium to book value (about 4% rich to the sector average valuation) and a dividend yield of 11.2%.

Quarter Update

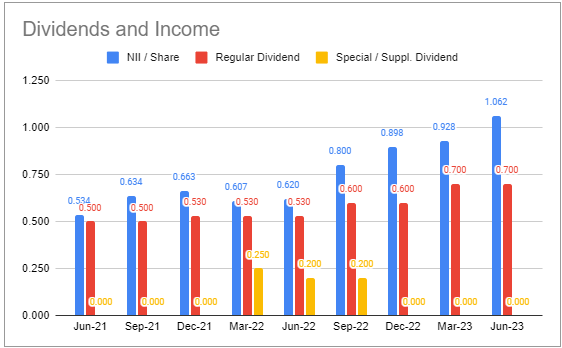

Net investment income increased by over 14% to $1.062.

Systematic Income BDC Tool

This was an unusually sharp jump not only relative to the previous quarter but also relative to other BDCs, most of whom are managing only single-digit net income rises.

A key factor for the sizable rise in net income was a combination of an unusually low level of repayments in Q1 and an unusually high level of repayments in Q2. This was responsible for nearly 8% of total income in Q2. There is some risk of mean reversion here which could pull net income lower in Q3 particularly as 2/3 of the repayments were driven by only two transactions.

Blackstone

Outside of repayments, a strong level of investment income and a drop in interest income due to a fall in leverage all combined to put up a strong net income number.

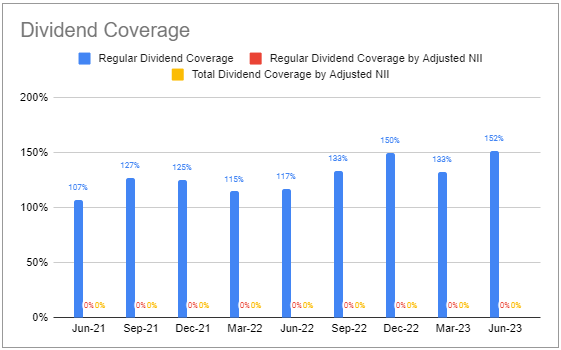

The company covered its Q2 regular dividend of $0.70 by 152%. In our last update we noted that even though BXSL previously hiked its base dividend to $0.70, the total dividend fell because it got rid of previous special dividends. In an environment of rising net income and very high coverage (133% at the end of Q1) we felt confident the company would be forced to either keep raising its base dividend or to introduce supplemental dividends.

Systematic Income BDC Tool

As it happens, BXSL went the base dividend route, increasing the Q3 dividend by 10% to $0.77. That leaves coverage at a still very-high 138%. If we strip out the fee waivers, that comes down to a still very healthy 129%. This suggests further base dividend hikes or a special towards the end of the year.

Management views high dividend coverage as an asset since it allows for both NAV growth (and its positive impact on valuation) as well as income compounding as the spillover can be reinvested into new loans. These benefits outweigh the 4% excise tax that would be levied on some of the retained cash.

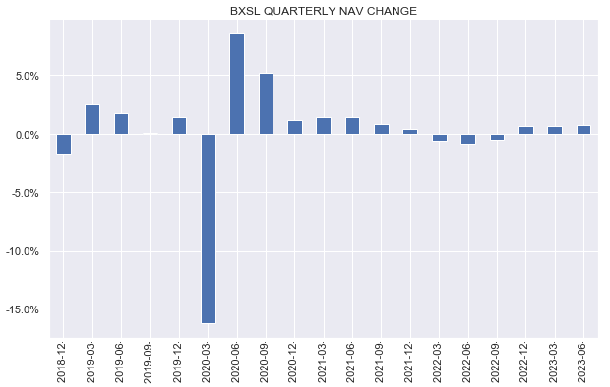

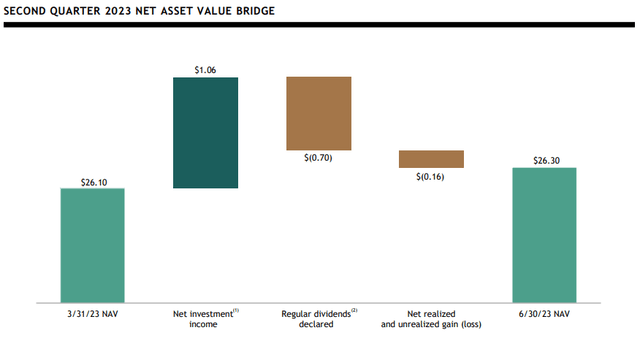

The NAV rose for the third straight quarter.

Systematic Income

This was primarily due to a large amount of retained income (i.e., net income in excess of the dividend) which more than offset a small amount of unrealized depreciation (there were net realized gains for the quarter).

Blackstone

The NAV is now at a new high since the company IPO’d – a great result in what has been a fairly difficult market period since 2022.

Income Dynamics

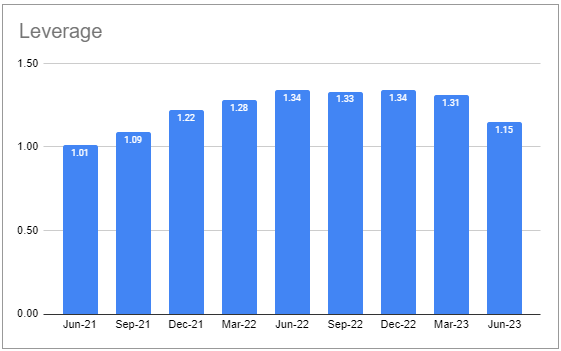

Leverage fell sharply over the quarter to 1.15x – the second consecutive quarterly drop. It is currently in the middle of the 1-1.25x range. The drop was due to both a relatively large level of repayments as well as a capital raise.

Systematic Income BDC Tool

At the end of the quarter the company had 65% of its debt in floating-rate format – one of the lowest in the sector and a great place to be given the current rate environment. However, the $400m 3.65% 2023 bond matured in July which pushed its fixed-rate debt profile to 55% – still above the sector average, but less impressive than before. The 2023 bond featured the highest coupon across its unsecured debt stack, so the net income headwind will be less than it could have been.

On the management call, which was held after the maturity of the 2023 bond, the company boasted about its 64% of drawn debt in unsecured bonds but failed to mention that this 64% figure included a bond that matured the previous month – a poor practice in our view.

The next bond maturity is in October 2026 which leaves the company among the best placed in the sector. Few if any BDCs will have a lower level of interest expense over the next few years.

99% of the company’s portfolio is in floating-rate loans – above the 96% median figure, which will allow it to take advantage of short-term rates that will continue to provide a net income tailwind over the next quarter, at the very least.

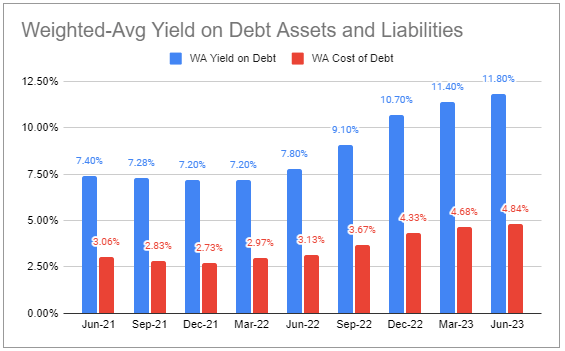

The weighted average asset yield rose to 11.8%, primarily as a result of the continued rise in base rates

Systematic Income BDC Tool

New deals are coming into the portfolios at an average yield of 12.4% – 0.6% above the overall portfolio yield, adding a small tailwind to net income.

Portfolio Quality

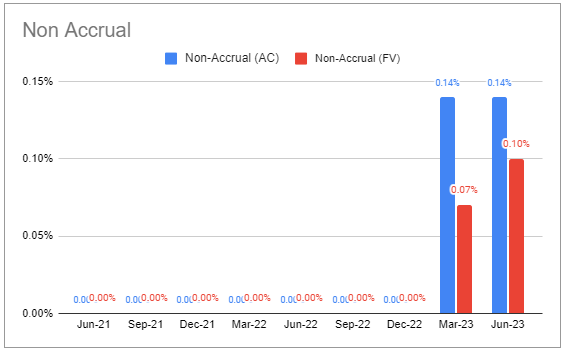

Non-accruals remain at rock-bottom levels.

Systematic Income BDC Tool

There were two performance-related amendments during the quarter. For one situation management expects a full recovery of principal while for the other there is a positive trend in the performance of the affected business.

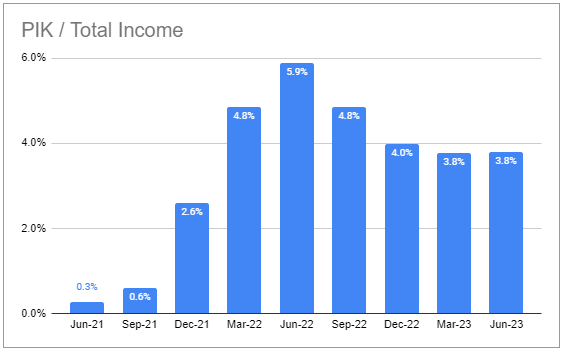

PIK remained well-behaved and below the sector average.

Systematic Income BDC Tool

Trailing 12-month average interest coverage was 2x. About 2% of the portfolio had coverage below 1x. At 5% rates – where we are now – the company says about 8% of the portfolio will have coverage below 1x.

The company’s focus on high EBITDA companies ($183m weighted average) with a high level of sponsor support (85% of loans are to companies owned by private equity or other sponsors) is strategic. The company points to evidence which shows that larger companies have a lower default rate while sponsors can provide another level of support to a struggling company, making it less likely to go under.

Return And Valuation Profile

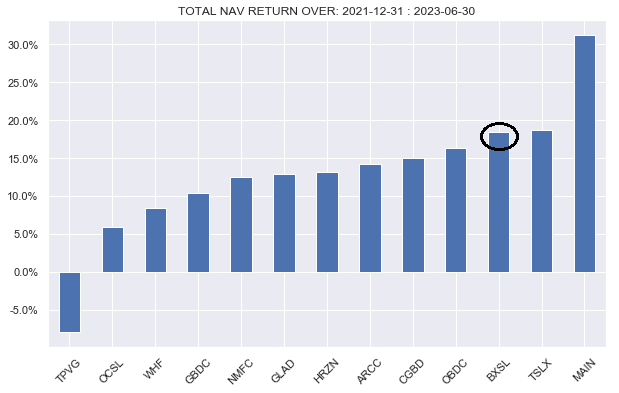

Of the companies whose Q2 earnings we have processed so far, BXSL stands out in its total NAV return since it began trading – besting stalwarts like ARCC and nearly matching the high-flyer TSLX.

Systematic Income

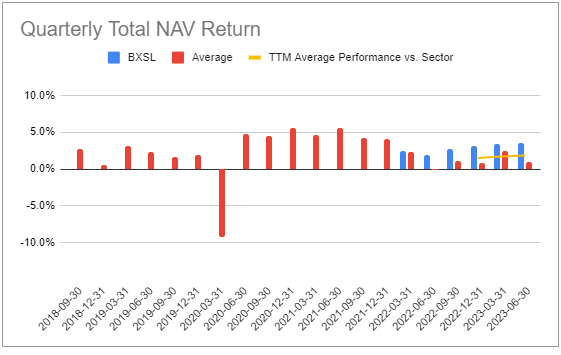

The company has outperformed the sector in all the quarters since it IPO’d.

Systematic Income BDC Tool

Stance And Takeaways

BXSL remains an attractive higher-quality BDC. The portfolio is allocated almost entirely to first-lien assets while 95% of portfolio companies have sponsors which can provide additional support. Weighted-average LTV of the portfolio is sub-50% and non-accruals remain near zero.

Given the size of the broader Blackstone umbrella, BXSL also has a large “bench” of people to support its portfolio companies. Another attractive feature of BXSL is its diversified portfolio. BXSL has 180 portfolio companies in the portfolio vs. 127 for the median BDC in our coverage.

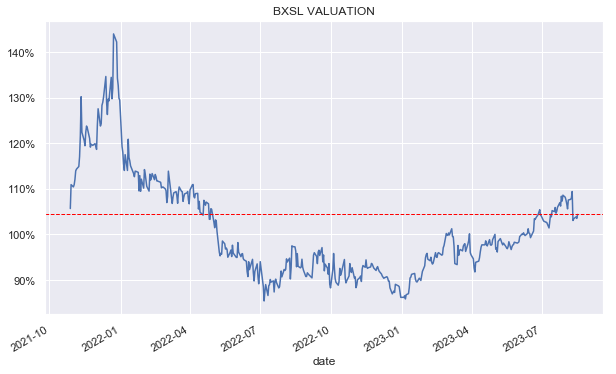

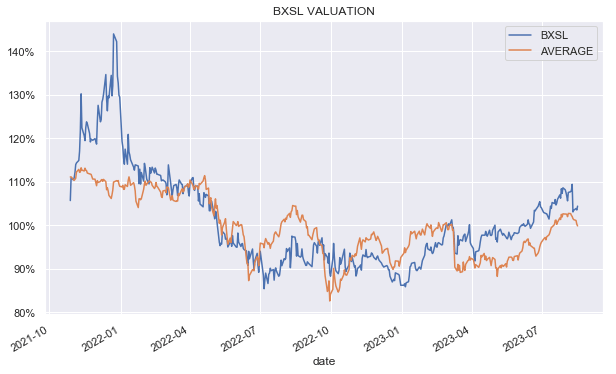

BXSL has not escaped investor attention and has steadily rallied from its amazingly cheap valuation over the second half of 2022 when it traded down to a double-digit discount to book value.

Systematic Income

We can see this even better relative to the broader sector in the chart below. The stock used to trade below the sector average valuation in 2022 which was the period when we added to our position several times. Given its continued strong track record we don’t expect the company to be as big a bargain as it was a year ago.

Systematic Income

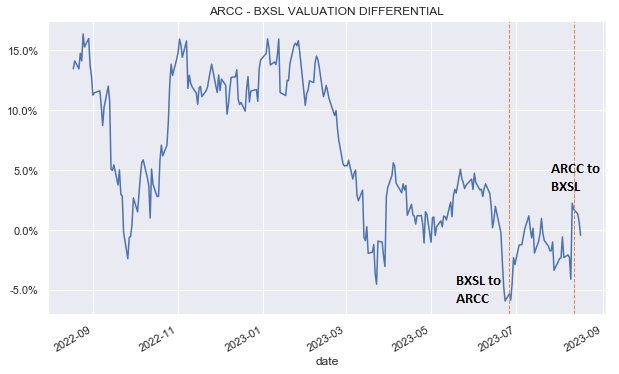

That said, there are still some relative value opportunities. For instance, we rotated from BXSL to ARCC when BXSL traded out to a 5% higher premium than ARCC. We then moved back to BXSL when ARCC moved out to a 2.5% higher premium. Volatility has not escaped the BDC sector, and we expect these relative value opportunities to generate significant value in the Portfolios.

Systematic Income

Read the full article here

")

")

")

")

")

2026-04-01")

")