")

")

Investment Thesis

With the earnings just around the corner, I wanted to take a look at Analog Devices (NASDAQ:ADI) financials and briefly at the outlook for the rest of the year. The company’s financial metrics show a slightly worrying downtrend in profitability, which I think will not last, however, I would be cautious right now and would like to see the share price coming down a little more to my desired risk/reward profile.

Outlook

Looking through the quarterly reports and analysts’ estimates for the remainder of the year, it doesn’t seem very promising that we will see another high revenue growth, with analysts predicting only around 5% y-o-y growth and then -2% the following year.

It seems like the company is not immune to the negative sentiment in the semiconductor sector. Many, if not all semiconductor companies I covered in the past have been affected by the high inventory levels and low demand for the product, which translated into lower revenues and lower share prices. Many of the companies are predicting that we have seen the worst of the negative sentiment in the first half of the year and that the sector will start to pick up in the last quarter of the year and ’24 and ’25 we will see robust growth in all of the categories in the semiconductor sector. Only time will tell how much growth Analog Devices are going to capture.

I have confidence in the industrial and automotive sectors to deliver decent revenue growth going into ’24 and beyond once the sentiment improves and the customers go through the inventory buildup. The global semiconductor industry is forecasted to grow at around 12% in ’24, which is a nice rebound from the declines we saw in the recent past. The automotive sector is also poised to perform well in ’24 and beyond with Asia-Pacific looking to be the most demanding for automotive semiconductors, more than doubling demand by ’28 from ’20.

In summary, I believe there will be a lot of volatility in the remainder of the year, which may present a buying opportunity if the stock price drops significantly, however, the worst has passed in my opinion and the whole of the semiconductor industry is looking to rebound very strongly in the next year and the company should be able to capture a good part of that growth.

Financials

Just to note, I will be looking at yearly figures, which means all the graphs below will be as of FY22 as that shows a better picture in the long term. I will include the most recent figures for extra color also.

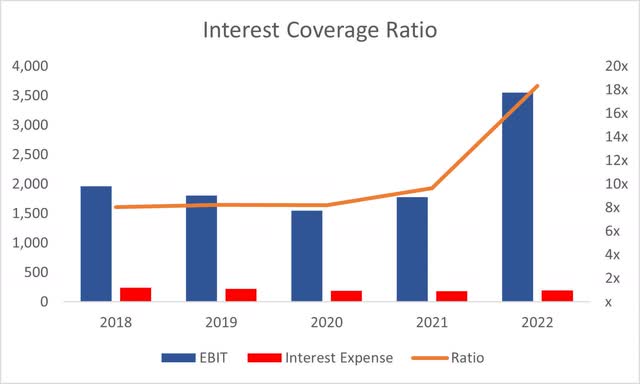

As of Q2 ’23, the company had around $1.17B in cash against $6.5B in long-term debt. A lot of investors may not go any further than that because a lot of them do not like companies that have a lot of debt on their books. I think debt is fine as long as it’s manageable and in the case of ADI, it is more than manageable. The interest coverage ratio at the end of FY22 stood at around 18x, meaning operating income was able to cover the annual interest expense 18 times over. For reference, an interest coverage ratio of 2x is considered healthy. Sure, it would be great if the company de-levers further, however, even at this point, the company is at no risk of insolvency.

Interest Coverage Ratio (Author)

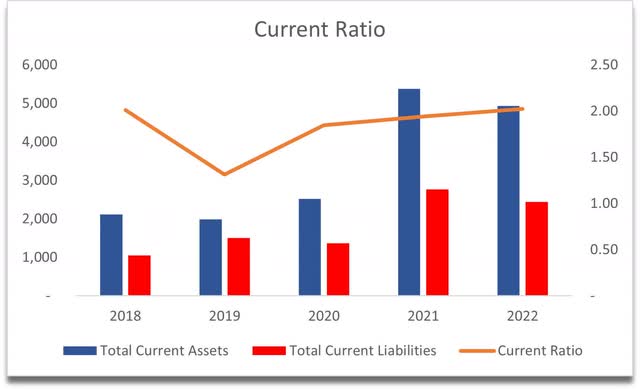

ADI’s current ratio has been decent over the years too, which stood right at that range that I like companies to be in, which is around 1.5-2.0. This tells me that the company is not sitting on a huge pile of cash that could be allocated for further growth of the company. The company’s ratio was at 2 at the end of FY22, which means it can cover its short-term obligations twice over.

Current Ratio (Author)

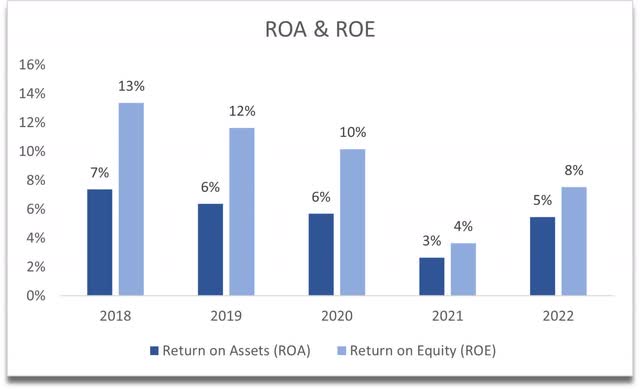

In terms of efficiency and profitability, the company’s ROA and ROE have been experiencing a long-term downtrend for the last 5 years or so, which is not very promising. ROA sits at around my minimum of 5%, but ROE is slightly below my minimum of 10%. I can see that it has improved from the bottom of FY21, which is promising.

ROA and ROE (Author)

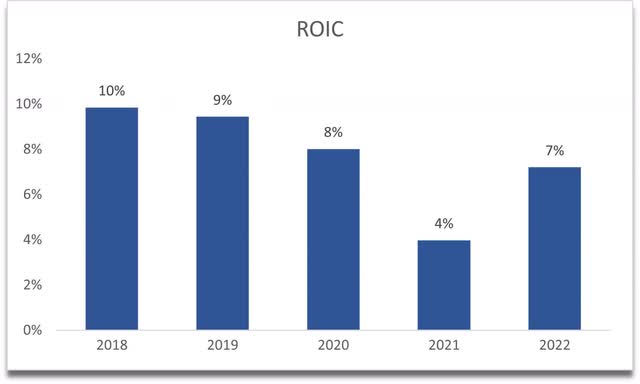

The same story can be said about the return on invested capital. It has been coming down in the recent past and is experiencing a rebound in FY22, which I think will continue going forward and will reach new highs in FY24.

ROIC (Author)

Overall, the company is in a decent situation financially, with rebounding profitability and efficiency metrics, which I believe will reach new highs in ’24. I think the company is well equipped for any further economic downturn that we may see shortly.

Valuation

I am surprised that the revenue assumptions of the analysts are so low going forward. The 60% revenue growth experienced in FY22 was due to an acquisition, so I wouldn’t have expected such growth to continue, however, a 5% growth in revenues in ’23, -2% in ’24, and 6% in ’25 hardly screams a company deserves a high multiple in my opinion.

So, for my base case, I went with a 6.5% CAGR for the next decade. For the optimistic case, I went with 10.3% CAGR, while for the conservative case, I went with 4.5% CAGR for the next decade.

In terms of margins, I decided to average gross margins to 75%, while operating margins will average at around 48.5% over the next decade. This will bring net margins from around 38% in FY23 to around 40% by FY32. I don’t think I could have increased margins anymore simply because I like to keep it more conservative to give myself more room for error.

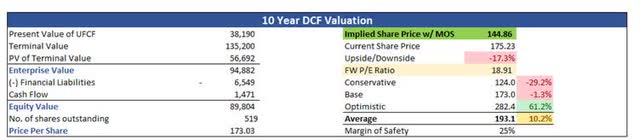

On top of these estimates, I will add a 25% margin of safety to be even safer. With that said, Analog Devices’ intrinsic value is around $144.86 a share, meaning that currently it is a little expensive to start a position and the risk/reward profile is not very attractive at these prices.

Intrinsic Value (Author)

Closing Comments

If the company’s revenues grow much better than analysts predict, the company could be worth a lot more than what it is trading at now, however, seeing that the headwinds persist I had to assign a little bit more of a margin safety and I believe that the company may reach that intrinsic value in the near future, at which point I believe the risk/reward is worth it and I would be opening a small position to test the waters once it gets there.

For now, I don’t believe it is a good time to start a position, considering that the volatility is going to be high because the company is due to report earnings on the 23rd of August. If we see weak guidance in the report, I can see the share price coming down to $140s by the end of the year.

In the long term, I have confidence in the semiconductor industry as it is one of the most valuable sectors these days and it will experience another high growth in the near future, just like it did before.

Read the full article here

")

")

")

")

")

2026-04-01")