")

All figures are in $ USD unless otherwise noted.

All financial figures come from Capital IQ unless otherwise noted.

Investment Thesis

I believe ONEOK Inc. (NYSE:OKE) will benefit from the competitive advantages that the proposed Magellan acquisition provides. If ONEOK can manage its debt load in a prudent style as well as maintain a reasonable dividend strategy, it appears there are a variety of catalysts that could pave the way for ONEOK to produce outsized returns.

Pending Acquisition of Magellan & Introduction

On May 14, 2023, ONEOK entered into an agreement to purchase Magellan Midstream (MMP) in a cash-and-stock transaction consisting of 63% stock and 37% cash (1 share of MMP = 0.667 shares of OKE + $25.00 cash). The cash portion of the transaction is expected to be funded through the issuance of notes. The expected purchase price is approximately $67.50 per Magellan share, representing a 22% premium to Magellan’s closing price on May 12, 2023.

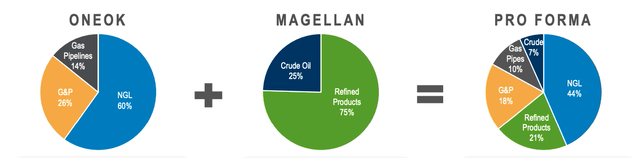

Magellan’s operations consist of the transportation, storage, and distribution of refined petroleum products and crude oil. Approximately 75% of their business is through the refined petroleum segment with the remaining 25% through the crude oil segment. They own the longest refined petroleum products pipeline system in the United States stretching 9,800 miles with 54 terminals.

ONEOK currently operates through three operating segments: their NGL segment (~60%), Natural Gas Pipelines segment (~14%), and Natural Gas Gathering and Processing segment (~26%). All of ONEOK’s operations occur within the United States.

Pending approval of the transaction, ONEOK’s operations will be closer to:

ONEOK Forecasted Operations Pending Acquisition (ONEOK Acquisition Presentation – Slide 8)

The pending acquisition would significantly diversify ONEOK’s operations and would likely result in them becoming one of the five largest oil and gas storage and transportation companies in the world competing with the likes of Enbridge (ENB), Enterprise Products (EPD), and The Williams Companies (WMB). The larger scale should enhance ONEOK’s presence in the market increasing the viability of their credit profile.

ONEOK expects the deal to add around 3% to 7% to EPS from 2025 through to 2027. The acquisition is expected to provide around $200 million in annual synergy cost savings and should increase annual free cash flow after dividends to ~$1 billion from 2024-2027.

I think that ONEOK is paying a significant premium for Magellan however, the competitive position that ONEOK would gain carries a value which is why they were willing to pay such a premium.

Concerns & Risks

My concerns with ONEOK and the pending acquisition are the amount of debt they currently have and the potential risk of not realizing the anticipated synergies.

ONEOK currently bears a hefty debt-to-equity ratio of 177.6%, in contrast to its peers’ 62.6%, underscoring the substantial debt burden that the company shoulders. With total debt reaching $12.821 billion and an additional anticipated $5.1 billion from note issuance, coupled with a net debt assumption of $5 billion from Magellan, the acquisition’s fruition would hoist ONEOK’s debt to an approximate $23 billion.

ONEOK projects that their net debt to EBITDA ratio will reach 4.0x by the end of 2024, well above the peer group’s modest 0.4x in 2022. While ONEOK plans to curtail this ratio to 3.5x by 2026, the current economic landscape is barred by high-interest rates. Given these circumstances, I believe the potential elevation of ONEOK’s debt multiples, which could venture into risky territory, especially as counterparts within this cohort have been steering towards debt reduction is one key concern to look out for. ONEOK is also targeting a 3.5x debt-to-EBITDA ratio as one of their capital allocation priorities which leads me to believe the focus on paying down debt will become a priority if this transaction goes through.

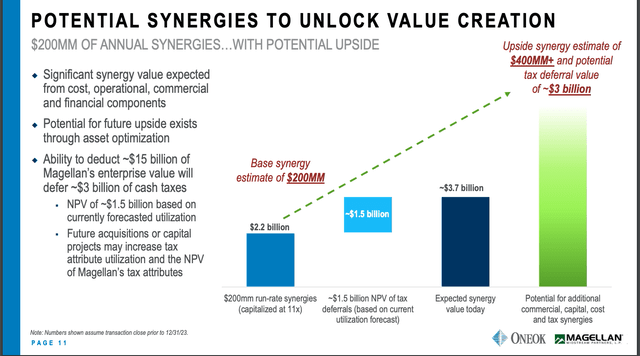

Assuming the debt burden doesn’t pose any issues for ONEOK, I turn my attention to the potential risk that synergies don’t materialize:

Potential Synergies of Acquisition (ONEOK Acquisition Presentation – Slide 11)

The current payout ratio, standing at 69.5% over the last twelve months, presents an encouraging picture, especially when compared to ONEOK’s target of maintaining a payout ratio below 85%. However, supposing the anticipated synergies fail to materialize as expected, I hold the view that it could potentially place ONEOK in a challenging predicament. The company would then be confronted with a decision between debt reduction and moderating their dividend growth trajectory. In more severe instances, there could even be a need to consider a dividend reduction.

It’s worth acknowledging that acquisitions of this magnitude inherently carry heightened risk factors. In this context, I emphasize the importance of ONEOK adopting a prudent approach to debt management, coupled with a commitment to fully realizing the synergies arising from the acquisition. Any misalignment in either of these aspects could conceivably steer ONEOK towards a dangerous financial position.

Catalysts

Fee-Based Revenue & Attractive Trading Multiples

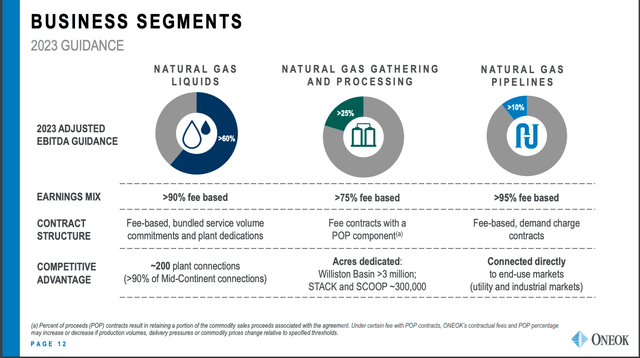

Assessing the valuation of commodity-based companies can prove challenging due to the unpredictable nature of commodity prices. However, ONEOK has minimal exposure to commodity pricing risks. Over 90% of their NGL business operates on a fee-based model, while more than 75% of the Natural Gas Gathering and Processing segment follows suit. Additionally, over 95% of their Natural Gas Pipelines business operates on a fee-based structure. This limited reliance on direct commodity pricing, coupled with their strategic hedging practices, provides ONEOK with a notable level of stability and predictability in their cash flows.

ONEOK Business Segments (August Investor Presentation – Slide 12)

The fee-based structure adopted by ONEOK holds notable advantages, primarily in bolstering the predictability of cash flows. Moreover, this approach substantially enhances ONEOK’s ability to offer lenders and shareholders a transparent and comprehensive view of their capacity to fulfill debt obligations.

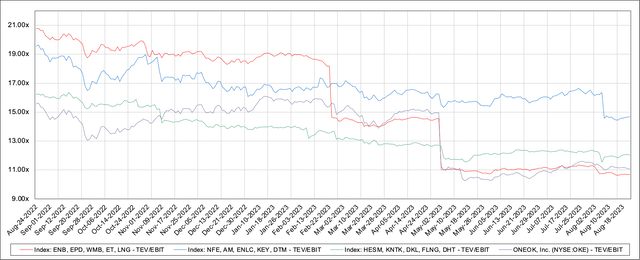

To assess trading multiples, I’ve formulated three distinct indices comprising peer companies in relation to ONEOK. Each index is structured based on both company size and regional operational focus. This approach accounts for the potential premium associated with larger enterprises and ensures uniform comparisons, all within the context of operations primarily confined to the USA and Canada:

- Index A (Marketcap > $10 billion): Red

- Enbridge (NYSE:ENB), Enterprise Products (NYSE:EPD), The Williams Companies (NYSE:WMB), Energy Transfer (NYSE:ET), and Cheniere Energy (NYSE:LNG).

- Index B ($2 billion < Marketcap < $10 billion): Blue

- New Fortress Energy (NASDAQ:NFE), Antero Midstream (NYSE:AM), EnLink Midstream (NYSE:ENLC), Keyera (TSX:KEY:CA), and DT Midstream (NYSE:DTM).

- Index C ($250 million < Marketcap < $2 billion): Green

- Hess Midstream (NYSE: HESM), Kinetik Holdings (NYSE: KNTK), Delek Logistics (NYSE: DKL), Flex LNG (NYSE: FLNG), and DHT Holdings (NYSE: DHT).

Over the course of the past year, Index A has maintained an average TEV/EBIT multiple of 15.68x, while Index B exhibited a multiple of 16.7x, and Index C stood at 13.57x. In comparison, ONEOK’s average multiple over the same period was 13.65x. Despite the market capitalization suggesting closer alignment with Index A, the multiples reveal a different narrative. ONEOK’s multiple has consistently trailed Index A’s by approximately 15%, and interestingly, it has also only traded slightly higher than Index C by around 0.58% over the observed year.

TEV/EBIT Multiples – Midstream Oil & Gas (Capital IQ)

When expanding this analysis over a span of three years, the average multiples becomes more distinct. ONEOK’s multiple has consistently lagged behind Index A’s by approximately 8.9%, while conversely, it has exhibited an elevation of around 35% compared to Index C. The illustration provided above underscores the disparity in ONEOK’s trading position relative to the respective peer groups. This discrepancy in valuation could potentially be attributed to the impending acquisition; However, I am inclined to believe that ONEOK should be positioned closer to the trading multiples of Index A. I highlight this further because the acquisition would likely propel them further in alignment with the peer companies in Index A.

Increasing United States Production & Narrow Moat

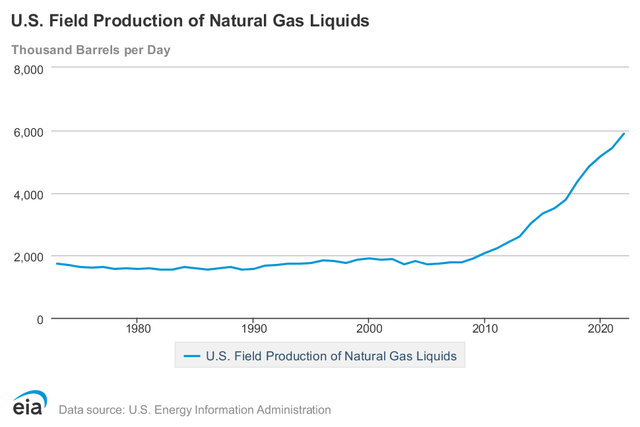

Production of NGLs in the United States has been increasing significantly since COVID-19:

U.S. NGL Field Production (EIA)

Monthly data from the EIA suggests that it’s continuing to grow with May 2023 production being approximately 7.8% higher than May 2022. This is great news for ONEOK because it means their shipping volumes are increasing which should translate into higher revenues. Notably, the U.S. is expected to continue increasing gas and oil production because of production cuts from OPEC which are being done in an effort to prop up the oil market. As long as WTI and gas prices remain where they are, O&G exploration seems to be profitable and the United States is at the forefront of this.

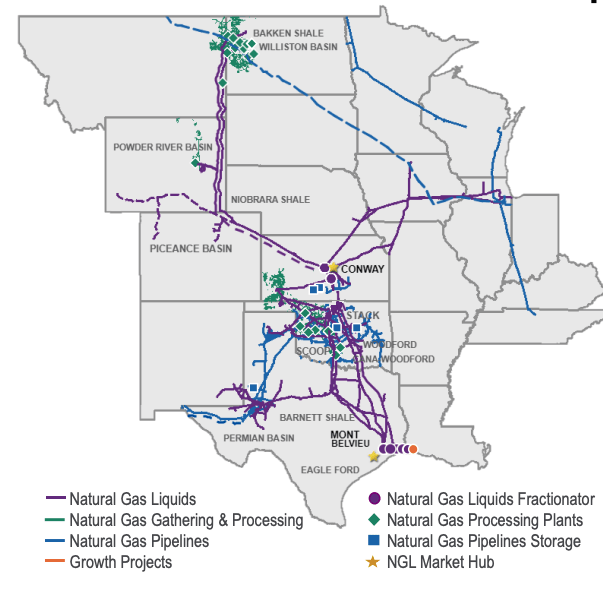

Considering the competitive advantages that ONEOK currently has in the NGL market which include factors such as greater than 90% of Mid-Continent connections and roughly 10% of U.S. natural gas production being reliant on ONEOK’s infrastructure, it’s evident that they carry a narrow moat in this sector.

Map of ONEOK’s Operations (August Investor Presentation – Slide 9)

With the acquisition pending for Magellan, their exposure in the American energy infrastructure market will significantly increase. The result of this is a wide moat in the NGL market potentially providing ONEOK with a stronger ability to control pricing among other competitive advantages.

Conclusion

I believe that ONEOK is overpaying for the acquisition of Magellan on paper and that there is a great deal of risk with the acquisition including failure to realize synergies, and the significant debt load they will carry if the acquisition goes through. I also see ONEOK benefiting from the acquisition because it will position the company to be one of the leaders in the energy transportation sector. Measuring the value of the competitive advantages they might receive from such an acquisition is extremely difficult however, I believe their long-lived assets will produce substantial cash flows giving further support to their dividend and ability to pay debt. Attractive trading multiples and fee-based revenue ensure a small margin of safety while production growth in the United States makes the future for ONEOK robust.

Disclaimer: This article is not financial advice, I encourage all prospective investors to consult a professional before making any investment decisions.

Read the full article here

")

")

")

")