")

Editor’s note: Seeking Alpha is proud to welcome Empyrean Research as a new contributor. It’s easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Investment Highlights

I am initiating coverage of Computer Modelling Group (TSX:CMG:CA, OTCPK:CMDXF). CMG is a dominant player in the reservoir simulation software industry, benefiting from significant barriers to entry and high customer switching costs. Recent shifts in CMG’s strategy, led by CEO Pramod Jain, highlight the company’s intent to capitalize on the emerging carbon capture and sequestration (“CCS”) domain, leveraging the headwinds affecting its traditional O&G business. With a substantial cash balance and no debt, CMG is also well-positioned to pursue strategic acquisitions, potentially driving future growth. I believe the market is yet to fully appreciate the major business transformation CMG is executing, presenting an attractive entry point.

Business Overview

What Does CMG Do?

Headquartered in Calgary, CMG is a leading provider of advanced reservoir simulation software to clients in over 60 countries, offering products that cater to different types of reservoirs and recovery processes.

The petroleum industry uses reservoir simulation to gain insights into reservoir behavior under different recovery methods. Through these visual models, experts can predict fluid flow, determine drilling locations, and assess operating conditions, risks, and investment returns. Simulating how a reservoir responds to recovery techniques before actual drilling and chemical injections is more cost-effective and less risky than experimenting on real wells.

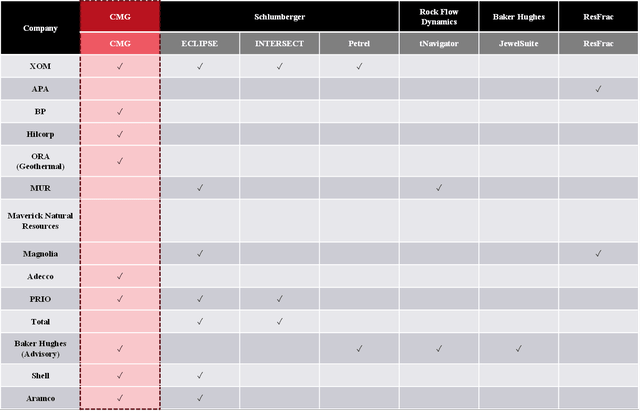

The market is dominated by a few major players: CMG (IMEX, GEM, and STARS), Schlumberger (SLB) (ECLIPSE, INTERSECT, and Petrel), Baker Hughes (BKR) (JewelSuite), Rock Flow Dynamics (tNavigator), and ResFrac.

Due to the high technical complexity of reservoir simulation and its integration with E&P’s extraction process, barriers to entry and switching costs are extremely high.

How Does CMG Make Money?

CMG has three segments (two software and one professional services/consulting). CMG sells two types of software contracts: Annuity & Maintenance (“A&M”), and Perpetual. Within each segment, CMG also breaks out four geographic segments: Canada, US, LatAm, and Eastern Hemisphere (Europe, Africa, Asia, and Australia).

A&M contracts are generally 1-year long and provide customers a set number of user licenses. They also typically include a maintenance component for technical support and allow customers to access the latest versions of CMG’s products each year as they are upgraded. CMG considers A&M revenue to be recurring, though I consider it quasi-recurring. Customers generally renew year-to-year, but A&M revenue can fluctuate significantly as customers scale up or down the number of user licenses they buy based on oil market fundamentals and capital investment plans.

Perpetual license sales are non-recurring, though they sometimes include a separate, recurring maintenance component. Perpetual revenue is extremely lumpy and largely generated in the Company’s Eastern Hemisphere segment.

The Professional Services segment offers training and workshops to help users maximize the value of its products and technical support in complex simulation challenges.

Qualitative Analysis

What is CMG’s Moat?

CMG’s competitive positioning primarily benefits from high barriers to entry and customer switching costs.

The existence of strong barriers to entry in the industry is supported by the limited number of players and the stability of the market structure over time.

The table below shows the major providers of reservoir simulation software and their products (horizontal axis) and which products various energy companies use (vertical axis). This information was gathered from reservoir simulation engineer job postings from each company. It is interesting to note that many companies use multiple simulation products from the top five providers. This is due to the fact that different products are tailored to different types of extraction methods and problem sets. I believe this is beneficial, as it mitigates the risk of losing all of a customer’s business if they are able to overcome the high switching costs of changing software providers (see below).

Author

Switching costs are substantial for the following reasons:

Training and Expertise: Users need to be trained in the new software, which takes time and resources

Integration with Existing Systems: Companies have existing workflows and systems that the new software must be compatible with. Transitioning to new software may require updates or redesigns of these systems

Data Migration: Transferring historical data, models, and reservoir simulations from the old software to the new one

Vendor Relationship and Support: Companies must establish new relationships with the software vendor, which can involve negotiating contracts, and understanding support options

Furthermore, the oil and gas industry is facing a significant shortage of technical and engineering talent. According to Texas Tech’s annual survey of petroleum engineering programs, the number of PetEng grads in 2024 is expected to be only 500 across the US, down ~80% since the peak of ~2,600 in 2017. To compensate for the shrinking PetEng workforce, companies likely lack the manpower to manage a transition to rival software. This is supported by the fact that customers are growing increasingly reliant on CMG’s consulting business, which has accounted for ~43% of revenue growth since FY2012 and has been the fastest-growing segment for the past six years (excluding the perpetual segment due to its lumpy and unpredictable sales cycle).

These competitive advantages have enabled CMG to maintain ~43% and ~47% average EBIT and EBITDA margins, respectively, from FY2013-FY2023 and capital efficiency (n.b., average ~45% ROE from FY2013-FY2023 with no net debt).

Business Transformation: Transition to Energy Transition / CCS

In May 2020, Pramod Jain took over as CEO. In his first shareholder letter, Jain outlined his intent to double down on energy transition and M&A as avenues for growth. In the context of CMG, energy transition primarily means carbon capture and sequestration, which presents similar engineering problems to underground hydrocarbon recovery. Over the past several quarters, the strategy appears to be working. Energy transition accounted for ~22% of Q1 FY2024 revenue, up from ~14% in FY2023. In February 2023, CMG announced the first acquisition in the Company’s history, Unconventional Subsurface Integration, an early-stage AI-based data analytics technology for maximizing asset valuation and production performance of shale reservoirs.

I believe CMG’s renewed focus on CCS and M&A is significant for several reasons.

Firstly, although its core O&G business is highly attractive, it is cyclical and has exhibited almost no topline growth across recent cycles. Because the majority of CMG’s software revenue is derived from 1-year A&M contracts, customers are able to scale their number of user licenses up or down with the commodity cycle at regular intervals. M&A activity across the US and Canada has enabled customers to realize synergies and reduce their number of user licenses over time. The 2015 Oil Crash and recent climate policy changes have also significantly impacted the North American O&G landscape. E&Ps are exercising much more cost and capital discipline, dampening activity and, by extension, CMG’s growth potential.

By exploiting its competitively advantaged position to pursue CCS opportunities, CMG can unlock a large, untapped growth opportunity. The policy changes which have been headwinds for CMG’s core O&G business will act as tailwinds for its CCS business. I believe this could have the effect of tilting the market’s growth expectations up and reducing the perceived risk of growth, which could potentially drive multiple expansion.

Secondly, the push into CCS could, at a minimum, alleviate any “hydrocarbon discount” and may eventually lead to an ESG premium.

Thirdly, with its large cash balance (n.b., C$64.2MM at Q1 FY2024, ~9% of market cap), CMG has a lot of dry powder for acquisitions. Considering that the Company has no debt, there is also substantial upside in tapping its latent debt capacity to fund larger acquisitions or to finance buybacks.

Valuation

Downside Case

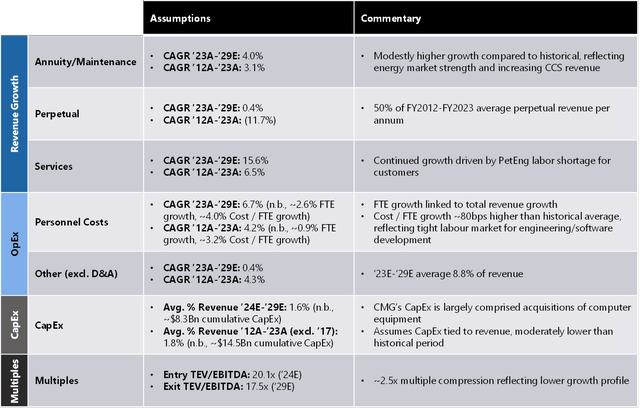

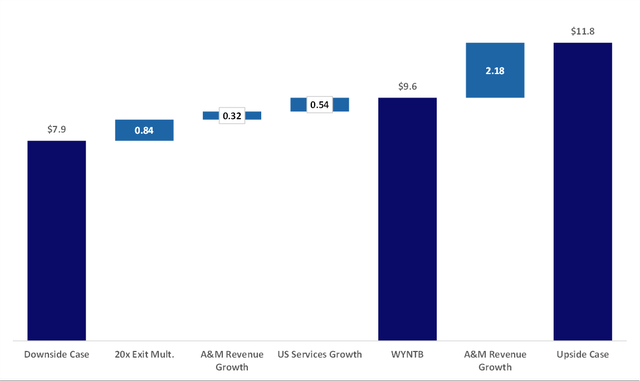

My valuation starts with a downside case. A&M revenue growth is slightly higher than the historical average. While this is a downside case, I believe this is a reasonable assumption given the strong demand for CCS solutions seen in recent quarters and the positive near-term O&G fundamentals. Due to the unpredictable nature of perpetual license sales, I simplistically assume 50% of the annual average historical sales. Services revenue growth remains elevated relative to historicals in all geographies, reflecting customers’ need to outsource simulation workflows due to the PetEng labor shortage. The downside case results in a target price of ~C$7.9/share assuming a 12% discount rate and 2.5x of EBITDA multiple compression, implying ~9% downside. Note that assuming no multiple compression, the target price is in line with the current share price.

Author

Central Case

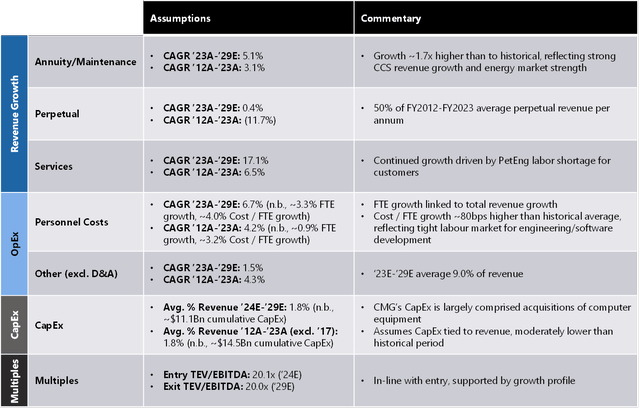

The central “What You Need to Believe” (“WYNTB”) case assumes a total revenue CAGR ~120bps higher than the downside case and no multiple compression, and results in a ~C$9.6/share target price at a 12% discount rate, implying ~10% upside.

Author

Upside Case

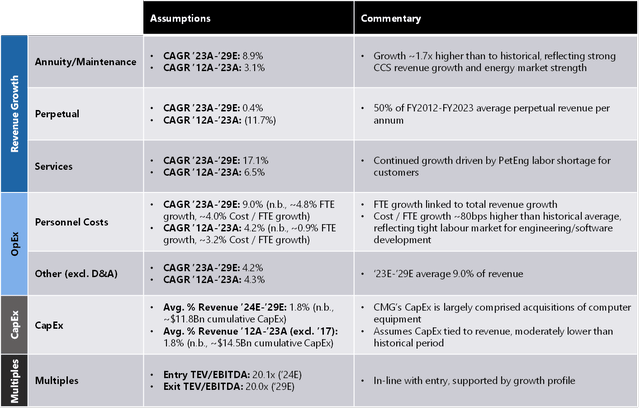

The upside case assumes total revenue growth ~280bps higher than the WYNTB case due to a slower taper of the growth rates. It also assumes a constant multiple and a 12% discount rate. This case results in a ~C$11.8/share target price, implying ~35% upside.

Author

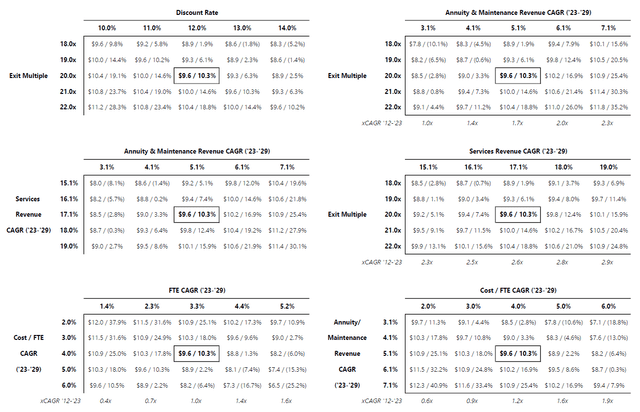

Sensitivities

The sensitivities below refer to the WYNTB case. Additionally, it is worth noting that the perpetual segment accounts for ~C$0.5/share in my model (i.e., assuming zero perpetual license sales would reduce the target price by ~C$0.5/share).

Author

Author

Analysis of Peers

CMG is the only public pure-play reservoir simulation company. Its main competitors are either large, diversified conglomerates (e.g., SLB and BKR) or smaller, private companies (e.g., ResFrac and Rock Flow Dynamics).

Capital IQ, PitchBook

The market is quite opaque, with detailed information on pricing and market share either unavailable or maintained behind paywalls. However, based on CMG’s historical revenue evolution, and anecdotal reports on reservoir engineering forums, I believe the market shares have remained relatively stable over time. Without a technical background or industry experience, it is difficult to determine the relative strength of each company’s product offerings. However, there are some data points that I believe reinforce the quality of CMG’s software. CMG’s software is taught in many university-level reservoir engineering courses and reservoir engineering research labs. This is a testament to its products’ prevalence, ease of use, and functionality. I believe it also has the added benefit of perpetuating the industry’s use of CMG, similar to how Adobe has remained industry standard, largely due to the fact it is taught in design programs.

Risks

Through my analysis, I have gained sufficient comfort with CMG’s business model and the market dynamics. Here are the main risks that have the potential to change my mind:

CCS Demand Risk: Uptake of CCS offerings is slower than expected, or business is lost to competitors.

Mitigation: With oil demand expected to continue increasing through 2030, and flatline through 2050, CCS will be a cornerstone of the decarbonization agenda. Government incentives should support adoption.

Commodity Risk: A sharp and/or prolonged downturn in oil markets would depress core reservoir simulation and services revenue.

Mitigation: Increasing contribution of CCS revenue should mitigate the cyclicality of the core O&G business. Recent actions by OPEC and a chronic under-investment on the supply side should support oil prices in the near- and medium-term.

M&A Risk: Although I have not assumed any M&A in my valuation and left it as a speculative upside, there is always risk of value-destructive M&A.

Mitigation: M&A within the industry (i.e., acquiring smaller competitors) would only serve to improve CMG’s competitive position by consolidating an already concentrated industry, and is unlikely to be value-destructive unless management significantly overpays. To date, management has been prudent with capital (e.g., share buybacks, targeted M&A), so I view this as unlikely.

Conclusion

Despite at ~50% rally YTD, current prices likely present an opportunity to acquire a high-quality software business with a huge growth runway at a reasonable price.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

")

2026-05-21")

")

: Why I Changed My Mind Recently")