")

The emergence of an explosive bull market in Bitcoin (BTC-USD) has certainly created some winners and losers in the crypto space. I think we’re a long way from being done with this bull market in Bitcoin and other cryptos.

One way to take advantage of that is through mining stocks, one of which is Marathon Digital (NASDAQ:MARA). The last time I covered Marathon, I slapped a buy rating on it. The stock is up over 40% since then; however, it plumbed new lows after my recommendation, and before this epic rally we’ve seen. So while I was proven right eventually, it was a rocky road, to say the least.

Back to the here and now, I’m sticking with my buy rating on Marathon. The stock looks very different than it did three months ago, but overall, I still think the risk is to the upside from here.

Charting the course

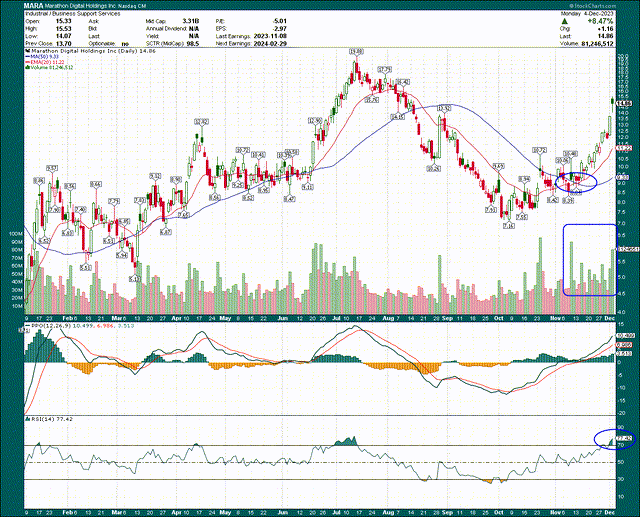

Let’s start with a daily price chart of Marathon to get a baseline. The simple read of this chart is that it’s firmly in an uptrend and exhibiting the price action indicative of a sustainable bull market. However, this is a crypto stock, and one that’s very heavily shorted, so normal rules don’t necessarily apply.

StockCharts

We have the shorter moving average well ahead of the longer MA, and both are sloping upward. So long as the price of the stock is above one or both of these, the uptrend is intact, and it can be bought.

Volume on this leg of the rally has been great, showing massive conviction from the bulls. It is, unsurprisingly, overbought. Both the PPO and 14-day RSI are showing overbought conditions. However, keep in mind during Bitcoin bull runs, both the coin itself and the stocks that track it can stay overbought for weeks or months. So while Marathon looks a bit stretched here, in no way am I suggesting this indicates the rally is about to end.

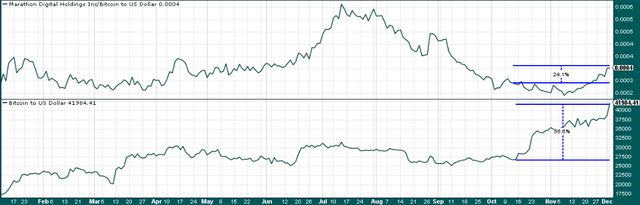

The value of Marathon relative to that of Bitcoin has started to move up, adding 24% since the rally in the coin began about six weeks ago.

StockCharts

However, it’s still well off its 2023 peaks, suggesting that if Bitcoin continues to rally, Marathon’s relative value to Bitcoin is likely to increase, as it has during previous bull cycles. If that occurs, look out above, especially as a quarter of the float is being shorted at the moment.

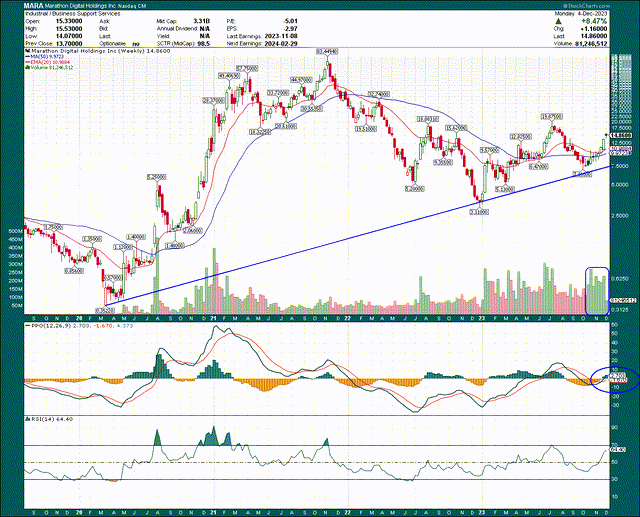

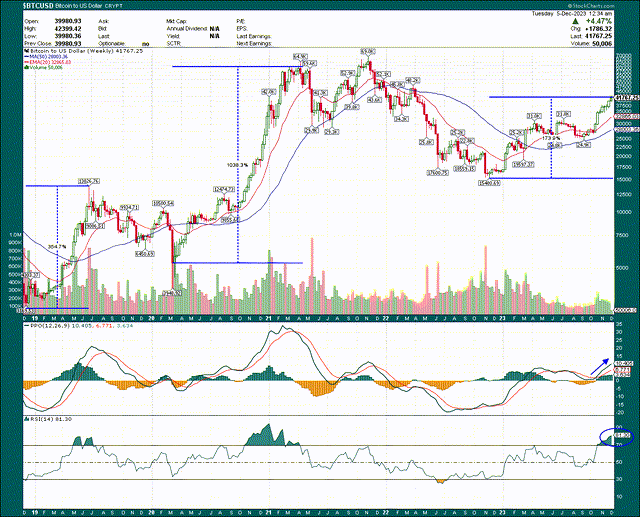

If we zoom out briefly to the weekly chart, we can see long-term support held, and that the stock is not only not overbought, it’s looking pretty neutral.

StockCharts

That leaves a huge runway to the upside longer-term if this run ends up being like prior cycles, so again, if you’re looking to manage risk, it looks planted firmly to the upside right now to me.

Now, we know Marathon trades roughly with Bitcoin, but by how much? Below we have the 50-day correlation of the coin and the stock to give us some clues.

StockCharts

Generally, they trade together, although there are temporary disruptions every now and then. Right now, the 50-day correlation is 0.81, which is extremely high, so it follows that we should look at Bitcoin itself for clues as to Marathon’s next move.

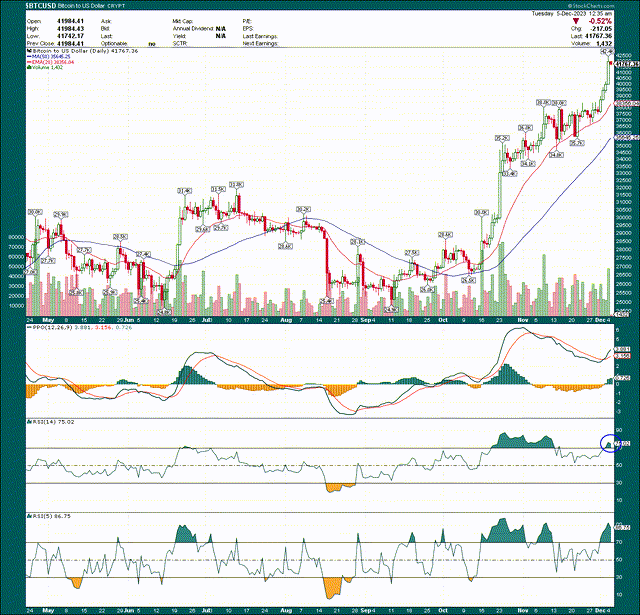

Bitcoin has been on an epic run, adding more than half its value in the span of several weeks. It’s overbought, but like I said above, it’s nowhere near the overbought levels we’ve seen in prior bull runs.

StockCharts

Is it extended? Yes. Do I think this rally is done? Absolutely not.

Bitcoin’s 2019 bull run saw a peak-to-trough move of 355%, while 2020/2021 saw an eye-watering 1,000%+ move.

StockCharts

This current move is at 174%, so unless Bitcoin puts in what would amount to a weak peak-to-trough move this time (which is possible), it has a long way to go. In fact, I think there’s a reasonably good chance we’re going to see it challenge its $69k high in 2024. We shall see, but my point is that trying to bet against a soaring crypto is a fool’s errand.

Fundamentals not for the faint of heart

I feel like I probably don’t need to say this, but Marathon is an extremely volatile stock, with extremely volatile business results. That’s not going to change, so if that isn’t your thing, there are thousands of other stocks you can own instead. However, that volatility creates opportunity, and right now, it is my belief Marathon is on the right side of that volatility.

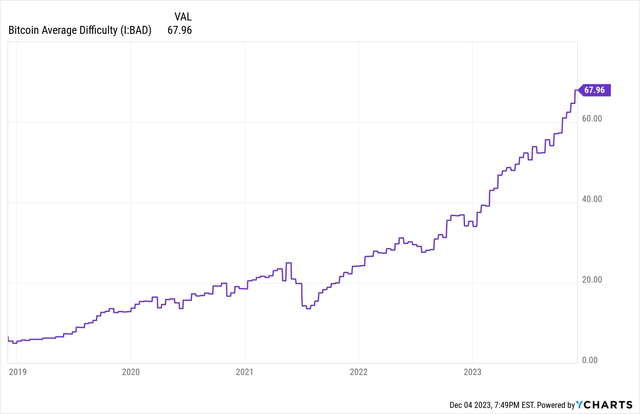

Revenue is heavily dependent upon a number of factors for a Bitcoin miner, some of which are outside of its control.

YCharts

One of those things outside its control is the difficulty of mining Bitcoin, the chart of which you can see above. Mining Bitcoin gets more and more difficult as more are mined, and this chart will probably look just like this in five years’ time. The point being, that it will take Marathon and others ever-increasing amounts of computing power to mine the same amount of Bitcoin. That means capex and operating expenses climb all the time, so this is not a business that someone looking for stability or relative value is going to like. There are plenty of times when Bitcoin miners cannot operate profitably, and Marathon is one of those. If you’re going to own this stock, that’s something you have to be okay with.

However, as I mentioned, so long as you’re on the right side of the volatility, the rewards can be enormous.

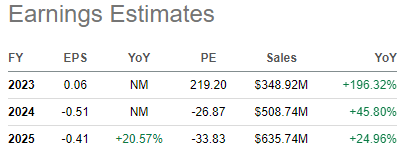

Seeking Alpha

Revenue is set to double this year, add another 45% next year, and a further 25% in 2025. The thing is that if I’m right about Bitcoin’s rally is nowhere near complete, Marathon’s revenue will likely be much better than these numbers over time. We’ll have to see, but that’s why the stock and coin are so closely correlated. If you’re bullish on Bitcoin, you’re bullish on Marathon, and vice versa.

A cash-burning machine

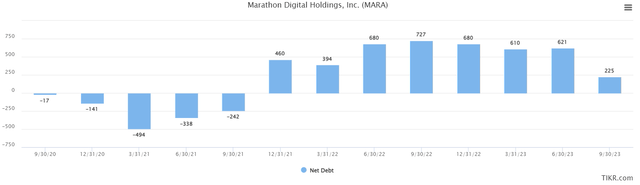

I mentioned capex above, and that’s an absolutely massive expense for a miner. The need for more and more equipment of ever-increasing efficiency is just a cost of doing business. However, this isn’t a business that throws off a lot of cash, so you end up with alternative funding methods to stay in business.

TIKR

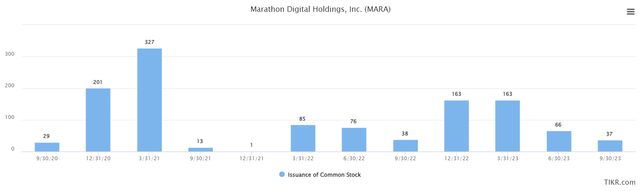

To Marathon’s credit, it has drastically reduced its net debt so far in 2023, which is now down to just $225 million. That’s great, but the problem is that it has simply replaced debt with even more common stock issuances.

TIKR

Issuing tens of millions of dollars in stock is a normal thing for Marathon, and its share count has ballooned from 52 million to 223 million in just the space of three years. I don’t see a scenario where this won’t continue to happen, so that’s yet another headwind longer-term for the stock. I honestly don’t know where the limit is here, but the business is free cash flow negative, so there’s no end in sight for share issuances, it would seem. Put simply, there’s no other source of sustainable funding.

Let’s wrap this up

As I mentioned, this stock is only for thrill seekers looking to add some volatility – and the potential reward that comes with it – to their portfolio. It’s heavily shorted and moves off of the whims of the Bitcoin market, so Marathon makes big moves in both directions.

I think there’s upside potential to current revenue estimates, Marathon’s value relative to Bitcoin, and the Bitcoin price itself. The technical picture looks great, apart from a short-term overbought condition.

Valuing the stock fundamentally is challenging given the lack of earnings, but we can use P/S, which has been below for the past couple of years and a bit.

TIKR

Marathon’s valuation has ranged from 0.9X to 14.4X in the past couple of years, so as I mentioned, this one is volatile, to say the least. Today’s valuation is 6.5X, so it’s pretty much in the middle of the historical range, but certainly higher than the past 1.5 years. It is my belief this is also not done rising, as higher Bitcoin prices will see investors pay more for exposure to mining, which should result in a higher P/S ratio for Marathon shares.

The bottom line here is that I think the risk for Marathon is higher, but I also acknowledge there is a huge risk in both directions. However, with the points I’ve made above, and 24% of the float being short, I think this rally has legs, and that we’re going to see Marathon go potentially a lot higher. I’m maintaining my speculative buy rating here for those who want Bitcoin exposure.

Read the full article here

")

")

")

")

")