")

")

Investment Thesis

MYT Netherlands Parent B.V. (NYSE:MYTE) is a global luxury e-commerce platform headquartered in Munich, Germany. In this thesis, I will analyze its first-quarter results along with its future growth prospects. I will also be analyzing its valuation at the current price level and the upside potential in the stock price. I believe MYTE presented poor results with muted sales growth and contracting gross and net profit margins, with no clear signs of recovery in the near future. Hence, I assign a sell recommendation for MYTE.

Company Overview

MYTE is an e-commerce platform engaged in providing luxury products globally across 130 countries, operating under the name Mytheresa. The majority of its revenues are accounted for by Europe, followed by North America and Asia. It offers ready-to-wear shoes, bags, and accessories for womenswear, menswear, and kidswear. Recently, it has introduced home decor and lifestyle products with the introduction of the category Life. It hosts 200 brands on its platform with a primary focus on luxury brands such as Bottega Veneta, Burberry, Gucci, Loewe, Loro Piana, Moncler, Dolce&Gabbana, Prada, Saint Laurent, and Valentino.

Investor Relations MYTE

Q1 FY2024 Result

MYTE posted weak first-quarter results, experiencing a significant decline in the profit margins, primarily due to increased advertising costs and higher sales costs. The net sales growth was in the single digits, growing 6.8% y-o-y. I think the company was more focused on minimizing its customer acquisition cost, which resulted in lower-than-expected revenue growth. I would like to highlight one positive move that could help it improve operational efficiency in the coming years, and this is the opening of the new central distribution center in Leipzig, Germany. This facility became operational in late September this year and has an area of 55,000 square meters. The following amounts will be in € EURO.

Investor Presentation MYTE

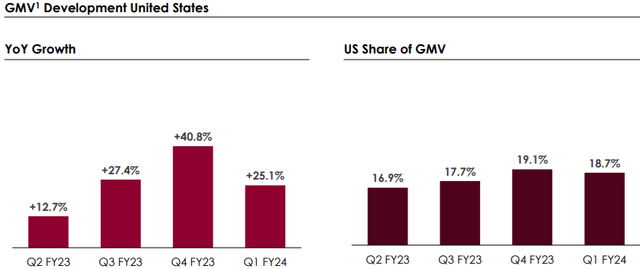

It reported net sales of €187.8 million, up 6.8% compared to €176 million in the same quarter last year. As per my analysis, a 25% y-o-y increase in gross merchandise value (GMV) primarily drove the revenues, partially offset by a slowdown in the Asia-Pacific market. GMV indicates the total value of sales, including the taxes and transportation cost, but is net of all returns. The revenue growth in the US market is a positive for the company. However, the management expects a softer H1 in FY24 with expectations of a slowdown in the US economy. The gross profit for the quarter witnessed a decline of 9.1% to €79.8 million, compared to €87.8 million in the same period last year. I believe the increased cost of promotional expenses resulted in this decline. Despite its plan to reduce the costs, the costs have actually increased much higher than the rate at which the revenues grew. The gross margin of the quarter stood at 42.5%, down from 49.9% in the corresponding quarter the previous year. The operational expenses followed the same trend, leading to an operational loss of €13.1 million, compared to an operational loss of €0.83 million in the same quarter last year. I think the new supply facility in Leipzig will help the company reduce its operational costs to an extent, but with high inflation expected to continue in FY24, the operational expenses will continue to rise. The diluted loss per share was reported at €0.14, compared to a loss per share of €0.04 in Q1 FY23.

Overall, the company failed to impress on multiple parameters. The gross profit and net loss margins deteriorated significantly during the quarter. The revenue growth remained muted, and the future guidance by the management doesn’t instill much confidence either. It provided FY24 guidance, with both revenues and gross profits expected to grow in the range of 8%-13%. However, the management commented that the results are expected to be in the lower range of the guidance. I believe the company might continue to underperform even in the coming quarters, given the expectations of a recession in the US economy and a slowdown in the European market. Not only this, but the net profit seems elusive, with the company expected to end FY24 with a loss, and even in FY25, there are no clear signs of profits, which I believe is a major concern for the company.

Valuation

MYTE is currently trading at a share price of $3.24, a YTD decline of 64%. It has a market cap of $267 million. It is trading at a forward non-GAAP P/E multiple of 24.8x, with an FY24 EPS estimate of $0.13. Comparing this to the sector P/E of 15.65x, I believe it is overvalued at its current price, even with a steep decline in the share price. I do not see any significant reason for it to trade at this premium valuation. I would recommend existing investors take advantage of any pullback in the share price and exit their positions, and for the new investors, taking any fresh buying position is not advisable.

Conclusion

MYTE is facing a consistent increase in costs and deteriorating profit margins. The revenue growth has been muted and is not expected to grow significantly in the coming quarters. The FY24 guidance by the management clearly reflects a slowdown in its performance. The company is trading at a premium valuation at a P/E multiple of 24.8x, which I believe makes it overvalued. Considering all these factors, I assign a Sell rating for MYTE.

Read the full article here

")

: Why I Changed My Mind Recently")

Q4 2026 Earnings Call Transcript")

")

")

")