")

Thesis

Bank of Hawaii Corporation, (NYSE:BOH), despite being one of the largest banks in Hawaii, faces challenges in revenue growth due to market saturation and limited opportunities in the tourism and real estate sectors. As one of the island’s premier financial institutions, the bank’s reliance on the Hawaiian tourism industry contributes significantly to its revenue, but it is also exposed to risks arising from the sector’s vulnerability to economic downturns. The study employs the Residual Earnings model to project a stock price target, indicating a potential upside opportunity of around 22%, making it a potential target for traders seeking undervalued opportunities but less appealing for long-term investors cautious of the various risks involved. However, the value proposition has diminished since the bank has already experienced a substantial recovery from the March banking panics.

Overview

Bank of Hawaii faces little competition in what seems like an oligopoly with other Hawaiian banks. However, there is a potential risk due to online banking, which allows Hawaiians to open accounts and mortgages with other banks. Additionally, the bank tries to compete in the tourism sector by strategically placing Point-of-Sale systems, as the growth in tourism directly impacts the bank’s earnings through these systems. Despite these efforts, the bank’s growth prospects appear limited as it operates in already saturated markets like Hawaii and small islands such as Palau, Guam, and Saipan, which heavily rely on tourism.

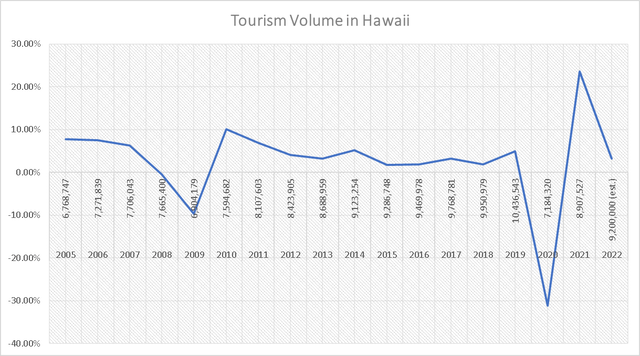

Presently, Hawaii is witnessing a return of tourism following the pandemic, which could potentially lead to increased revenue for the bank.

Tourism Volume in Hawaii (Author’s Calculations)

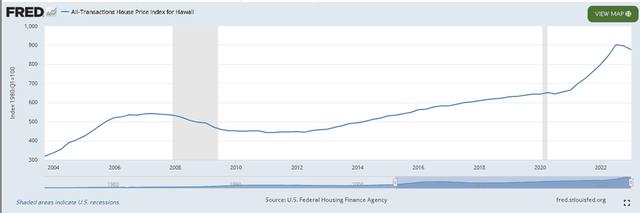

However, I believe the housing market in Hawaii is inflated, though this does not necessarily imply a crash but rather suggests that prices may stabilize without significant growth. This stabilization may prompt Hawaiian banks to reduce mortgage rates, ultimately affecting their net-interest margin.

Evolution of Hawaiian Real Estate Prices (Federal Housing Finance Agency)

In conclusion, significant growth for Bank of Hawaii seems unlikely unless it decides to venture into larger communities. It’s worth noting that the bank previously expanded its operations into Arizona, California, Fiji, Australia, Japan, South Korea, Singapore, Hong Kong, French Polynesia, Marshall Islands, Solomon Islands, and Micronesia. However, a lack of control over this expansion resulted in the 2000s bad loans crisis, leading to the divestment of those operations. As a result, the bank is now hesitant to undertake a similar risky expansion into larger markets.

Despite the challenges, there may be a potential value opportunity for Bank of Hawaii. The bank’s stock price experienced a significant drop during the March bank panics, triggered by the collapse of Silicon Valley Bank. Additionally, Bank of Hawaii offers a promising dividend yield of 5.2%.

Financials

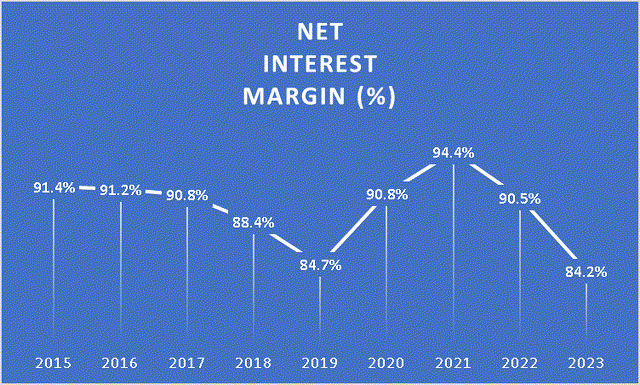

Bank of Hawaii’s Net Interest Margin, currently at 84%, has declined from 94% in 2021, and it has consistently hovered around this number since as far back as 2015.

Net Interest Margin (Author’s Calculations)

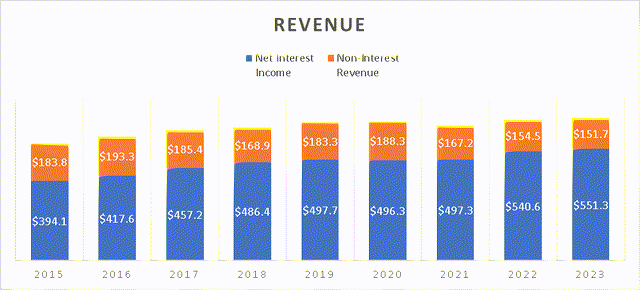

However, its revenue hasn’t shown significant improvement, remaining in a flat trend since 2019. In my opinion, this stagnation is a result of the already saturated Hawaiian market, which limits growth opportunities for the bank. Moreover, this situation may even pose a downside risk as smaller Hawaiian banks could compete with Bank of Hawaii and erode its market share.

Revenue Evolution (Author’s Calculations)

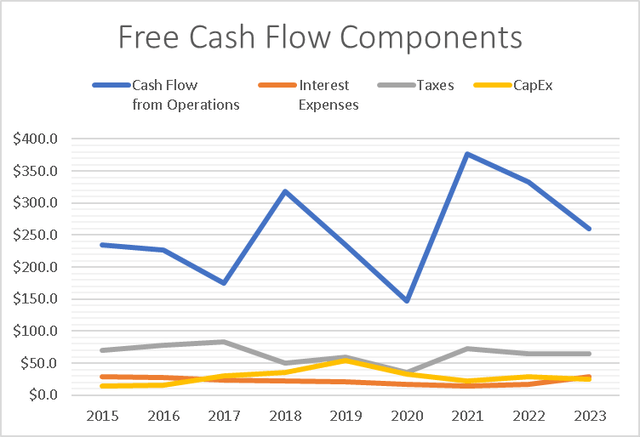

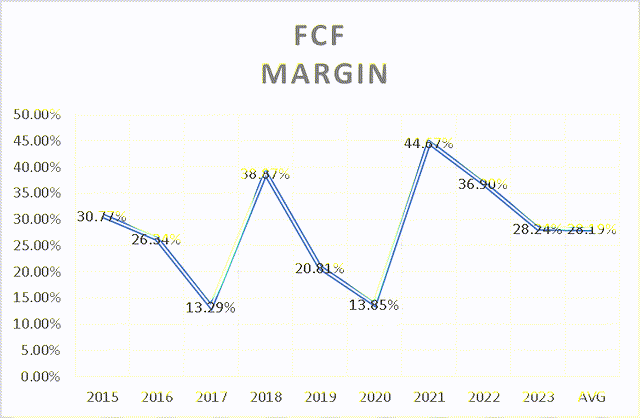

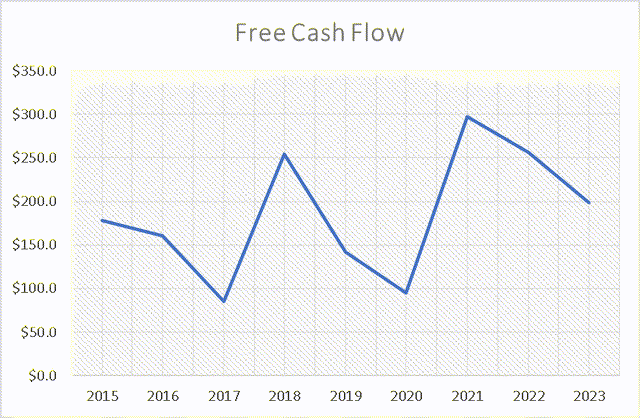

While the bank’s free cash flow stands at a decent 28% ($198.5 million), it has decreased from the highs of $296 million (44.6%) in 2021.

FCF Components Evolution (Author’s Calculations) FCF Margin (Author’s Calculations)

Free Cash Flow Evolution (Author’s Calculations)

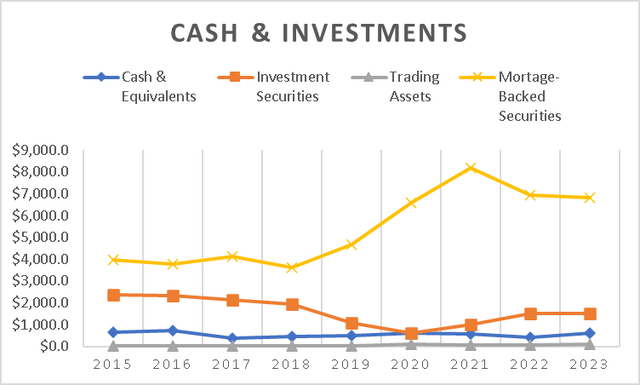

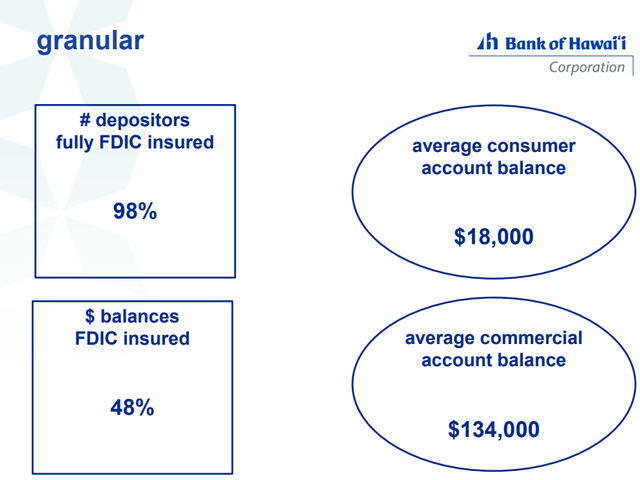

Regarding the bank’s survival in a bank run, approximately 48% of the balances are insured by the FDIC, leaving $10.6 billion in uninsured deposits. To address this, the bank holds $612 million in cash reserves and other current assets in the form of available-for-sale securities, amounting to a total of $8.4 billion in liquid reserves.

Cash & Investments Evolution (Author’s Calculations)

| Cash &Equivalents | Investment Securities | Trading Assets | Mortgage-Backed Securities | |

| 2015 | $656.4 | $2,365.7 | $14.0 | $3,952.8 |

| 2016 | $726.2 | $2,336.7 | $13.7 | $3,761.3 |

| 2017 | $374.7 | $2,139.9 | $10.5 | $4,108.9 |

| 2018 | $453.7 | $1,950.4 | $14.6 | $3,625.5 |

| 2019 | $490.3 | $1,063.5 | $28.9 | $4,682.4 |

| 2020 | $614.1 | $621.0 | $96.2 | $6,576.4 |

| 2021 | $560.4 | $999.3 | $42.0 | $8,198.2 |

| 2022 | $401.8 | $1,496.4 | $47.7 | $6,937.9 |

| 2023 | $612.0 | $1,507.5 | $85.1 | $6,810.1 |

FDIC insured Deposits (Q1 2023 Investors’ Presentation)

However, there are concerns about the losses on its securities portfolio, which amount to $1.4 billion compared to equity of $1.3 billion. This implies that any issues with these securities could have negative consequences for the bank’s shareholders, similar to what happened with First Republic.

Loss on Bonds Portfolios (Q1 2023 Earnings Release)

On the positive side, the bank’s deposit base appears stable as there are no SIB banks operating in Hawaii, making all banks in the region “regional lenders.” As one of the largest banks, Bank of Hawaii may be perceived as a safer option since it cannot be compared to banking giants.

Overall, the bank maintains a decent balance sheet and financial position, with the exception of the point of unrealized losses. Unless a catastrophic event occurs, Bank of Hawaii could be considered a value play. However, it is important to note that significant revenue growth is not to be expected, given the limited growth prospects in the tourism and Hawaiian real estate markets. In fact, there might be a possibility of slight short-term downward revenue trends, and without a growth plan, revenue could simply remain flat in the medium term.

Valuation

To value Bank of Hawaii, I have opted to utilize a Residual Earnings model. For revenue projections (from which I will derive the operating income), I considered that approximately 15% of its revenue comes from the Hawaiian tourism sector. Based on the expectation that the Hawaiian tourism market will experience a Compound Annual Growth Rate [CAGR] of 5% until 2033, the bank is likely to receive the following revenues from the tourism sector:

| Hawaiian Tourism Sector Revenue | BOH Revenue from Tourism | |

| 2025 | $ 20.243 | $ 105 |

| 2026 | $ 21.255 | $ 111 |

| 2027 | $ 22.318 | $ 116 |

| 2028 | $ 23.434 | $ 122 |

Using a simple rule of three, I calculated the remaining 85% of the revenue, which amounts to the following:

| BOH Revenue from Tourism | |

| 2025 | $ 13.500,00 |

| 2026 | $ 13.506,67 |

| 2027 | $ 13.513,33 |

| 2028 | $ 13.520,00 |

Next, I need to calculate other variables, such as operating income, net operating assets, and book value, which will be used in proportions. For instance, operating income represents approximately 39% of the bank’s revenue, book value is 1.92 times revenue, and net operating assets represent 96% of book value.

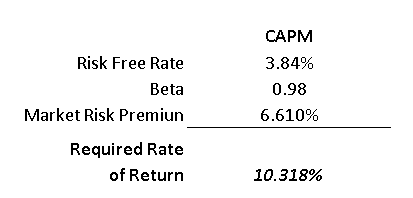

Before assembling the Residual Income model, I must determine the Required Rate of Return [RRR]. For this purpose, I used a Beta of 0.98, a 10-year market return of around 10%, and a Risk-Free Rate of 3.84%.

Required Rate of Return (Author’s Calculations)

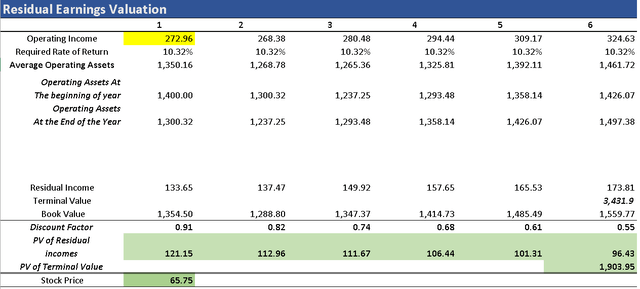

Residual Earnings Valuation (Author’s Calculations)

Based on the model’s calculations, the stock price target stands at $65.75 per share, indicating a 22.4% upside from the current stock price of $53.69. Although this presents an attractive return, I remain cautious as there is little room for error. Nevertheless, it is likely that the stock will experience an increase, especially considering the significant drop in March due to bank panics during that period. However, the potential for value strategy is diminishing, given the remaining return of just 22.4%, which would have been around 96% for those who purchased the stock at its low in May, priced at $33.46.

Risks to Thesis

The main risks to this thesis are Bank of Hawaii potentially missing estimates in 2023 and 2024, as well as losing market share to its rivals, which could reduce earnings from the Hawaiian tourism sector – the most critical growth driver for the bank. Additionally, the tourism sector itself can be vulnerable to the impact of a recession.

Furthermore, there is the inflated Hawaiian Real Estate Market, which is expected to remain stable. However, inflated real estate makes the region susceptible to a recession. It’s important to note that any potential drop in the market would likely be less severe than the one experienced in 2008, as most banks have since improved their lending standards, one of the contributing factors to the 2008 recession.

I’d also like to address Seeking Alpha’s Quant having a “sell” rating on the stock. However, this rating seems to be influenced by the “momentum” category, which I do not consider as a fact-based reason for a rating. It’s worth noting that the Quant Rating also acknowledges that the stock is currently more cheaply valued compared to its pre-March valuation, holding a grade of “B-.”

Moreover, I wouldn’t personally buy the stock due to its limited upside potential. However, for those interested in trading with the stock, it might be a worthwhile purchase. At its current stock price, it appears to be undervalued due to the banking panics that occurred in March. In my opinion, the likelihood of a bank panic affecting Bank of Hawaii is low, given its status as one of the largest banks in Hawaii and the absence of direct competition from SIB banks that dominate the mainland United States.

Conclusion

Bank of Hawaii faces challenges in terms of revenue growth due to the saturated Hawaiian market and limited opportunities in tourism and real estate. Potential risks include missing revenue estimates, competition from other Hawaiian banks, and the vulnerability of the tourism sector to economic downturns. Despite these challenges, the bank maintains a decent financial position with stable deposits and liquid reserves.

Using the Residual Earnings model, analysts project a stock price target of $65.75 per share, suggesting a 22.4% upside from the current price. However, this value opportunity may have decreased as the stock has already recovered significantly from the March banking panics.

Seeking Alpha’s Quant “sell” rating is influenced by the “momentum” category, which I consider as “not-based on hard-facts and fundamentals”. Nevertheless, the stock is deemed undervalued, making it attractive for traders seeking short-term gains.

In conclusion, Bank of Hawaii’s growth prospects seem limited, and the stock’s potential for long-term investors may not be significant. However, it could be an appealing option for traders looking for undervalued opportunities. It is essential to consider the various risk factors, including revenue uncertainties, competition, and the tourism sector’s vulnerability before making any investment decisions.

Read the full article here

")

2026-02-11")

")

")

")