")

")

There has been a lot of buzz about NET Power (NYSE:NPWR) on Seeking Alpha since it SPAC’ed earlier this year. Much of that discussion has revolved around whether it is worth waiting for the company to generate profits. To answer that question, I draw on company reports, analyst research, and conversation with a colleague in the industry to model NPWR’s long-term risk-reward profile. NPWR is inherently an ultra-high-risk investment, since its product is not yet commercially available, and it has no real sales or profits. But on the other hand, I think that valuation techniques which look out only a few years significantly understate NPWR’s long-term growth potential. Consensus estimates imply that NET Power shares could compound at over 20% p.a. for the next 20 years. I think that this potential makes NET Power worth the risk.

The Business

NET Power has over 300 patents in 33 countries to something called the Allum-Fetfedt Power Cycle, a new power plant design. are currently two other widely used designs, but this one has a significant advantage: it burns pure oxygen and natural gas, meaning that it only generates H20 and CO2. This makes it much more economical to extract pure CO2 from the exhaust. Liquid CO2 is used as the medium for power generation, which drives further efficiency, and then pure CO2 can be either stored or used in industrial and other applications. In short, NET Power owns the IP for the only cost-effective natural gas power plant design that does not emit CO2. My industry contact emphasizes how much further along NPWR’s technology is than other carbon capture technologies currently in development. And at current market rates, the efficiency and cost of NET Power’s design is basically competitive (more on this below). According to my industry contact, NET Power’s proposed carbon capture system is the most commercially developed one on the market today. Interested readers can read more about it in the MIT Technology Review and Barron’s.

They have built a small-scale demonstration plant in Texas, and project their first full-scale plant to come online in 2026. After that, their plan is to license their IP to power plant manufacturers, who would pay up-front (~$30 mil. over three years) and annual licensing (~$5 mil.) fees to NPWR.

investor presentation

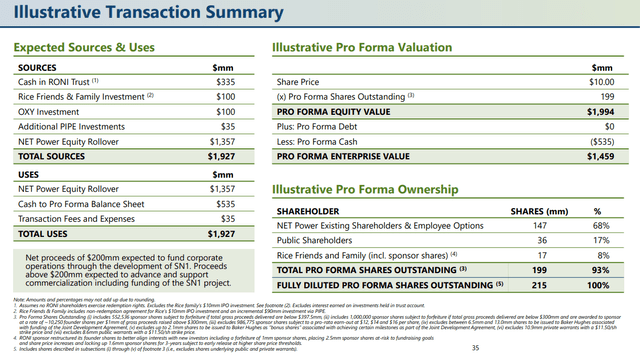

The IP was developed by renowned British engineer Rodney John Allum and his collaborators, and as shown in the slide above, NET Power has since received significant investments from a number of major players in the energy industry, namely Occidental Petroleum, Baker Hughes, the Rice brothers, one of whom is now CEO, and even Warren Buffett through Berkshire’s 28% stake in Occidental. David Einhorn’s Greenlight Capital has also built a sizable stake in the company over the last six months. This blue-chip backing gives me confidence that NET Power will be able to commercialize its IP.

Forecasts

TAM x Market Share x Licensing Fee x EBITDA Margin x EV/EBITDA

This is my basic formula for determining NPWR’s valuation. Below, I’ll walk through my assumptions for each of these variables, and then show several possible scenarios based on minor adjustments to them.

TAM

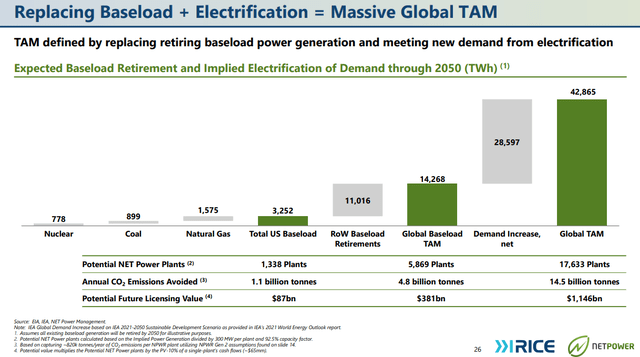

Global demographic growth and the transition to green energy should require a significant expansion of current power generation capacity over the next 20 years. There are currently over 60,000 power plants in operation. Given average lifespans of around 50 years, we would expect something like half of them to need replacement between now and 2050. In reality, estimates for new power plants are lower than that: NET Power management and Janney both project demand of over 15,000 plants through 2050. These numbers seem plausible to me, and below I will use them as a baseline.

investor presentation

Market Share

Any estimate of NPWR’s potential market share is almost a guess. With that being said, here are some of the relevant factors.

- NPWR has partnerships with key industry players who will presumably want to use their design.

- Given current carbon-capture tax credits, NPWR’s design is much cheaper than any of the existing alternatives. According to my sources in the industry, these credits have wide bipartisan support, since Republicans want to support fossil fuel-based power generation. Using natural gas has helped America achieve energy independence, and it seems likely that this will continue to be an important political consideration for the U.S. government in the future. And even if these national regulations were eliminated under a Republican administration (i.e. if Trump won the election in November), carbon capture mandates could continue to spread at the state level. In the longer-term, it seems likely that other developed countries pursue similar avenues to reduce carbon emissions, potentially driving demand for NPWR’s designs abroad.

- U.S. natural gas reserves are currently 20 times annual demand: we have 20 years of natural gas left. But U.S. reserves are only 10% of global reserves, and since foreign consumption is lower, this amounts to 50 times global annual demand. And our knowledge of the natural gas reserves available has been continually increasing over the last 20 years. So, although annual energy consumption has increased, so have the (known) reserves. Given these remaining supplies, natural gas will probably remain one viable fuel source for at least the next 15-20 years. NPWR’s plant design can also be used for coal-burning plants, but this is not the company’s primary focus at this time.

In my opinion, prevailing market share estimates are reasonable. Janney gives an estimate of ~800 plants deployed in 2050, a number which corresponds to the bear (“high capex and gas price”) case given by DeSolve, the firm of Dr. Jesse Jenkins, a Princeton engineering professor who consulted on the SPAC. This estimate implies that NET Power takes a 5% market share of new power plants. Below, I take this as my baseline assumption.

Fees, Profits, Multiples

Generally, I am convinced that the licensing business model will produce high margins. While fees and margins may change, I don’t see them as predictable at this stage, so I will just discount management guidance to build in a margin of error. Management forecasts a 90% gross margin, and Janney forecasts a 70% EBITDA margin. Given that NPWR has no debt and virtually no hard assets, I think that these high margins should be attainable. I adopt an EV/EBITDA multiple of 10, somewhat below long-term averages for utilities.

Base Case Valuation

If NPWR is able to meet the goals outlined above, then EV in 2050 would be over $200 billion, more than 150 times that of today. (For comparison, today there are around six American utilities with market caps above $50 billion. At $200 billion, NET Power would be the largest by market cap.) This would translate into an annual return of slightly over 20% for the next 23 years. In other words, the base case agreed upon by Janney and DeSolve is that NPWR is on track to become a 100-bagger. I think this is what David Einhorn was talking about when he said in Greenlight’s Q2 letter that: “NPWR is in the early stages of its commercial deployment, and if it doesn’t work out, the downside is more than we would usually stomach…However, the upside also appears to potentially be a multi-bagger, and we have managed our risk by sizing the position appropriately.” As of the end of Q3, Greenlight has 2.29% of its assets invested in NPWR.

Obviously, there are many optimistic assumptions baked into this projection. I won’t go through all of the potential scenarios here, but there is a linear relationship between their market share and profits. You can estimate NPWR’s valuation in different scenarios with the formula given above.

It’s worth highlighting several factors which could provide further upside.

First is faster growth. Management’s base-case scenario is that they will be able to contract for over 1,900 power plants by 2050, more than twice the number used in my base case.

Second, the company should pay dividends. Utilities average gross margins of around 70% and net margins in the high single digits. They then pay out over 50% of these earnings in dividends. Utility dividend yields average around 4%. NPWR’s proposed operating model is very capital-light, and I would expect them to be able to exceed industry average margins once plants come online. This should be able to sustain an industry-beating dividend yield as well. That yield would drive the base case annual return up into the mid-20s.

Why is this opportunity available?

The base case scenario outlined above seems almost unbelievable. Why would a well-known company with such incredible long-term return potential be trading at such a low valuation? This question has led some Seeking Alpha readers to conclude that NPWR’s technology must be less effective than management says. I find this interpretation unconvincing, for the simple reason that the stakeholders involved in commercializing NET Power’s technology are very heavily invested in the company, both personally and financially. I do not think it is plausible that NET Power is a scam. Instead, I think shares are undervalued for three simple reasons: risk, time, and float.

1. Risk: As I outline in more detail below, there is a chance that NPWR’s technology does not turn out to be durably profitable. There are lots of remaining unknowns about the commercialization pathway for NPWR’s power plant design and licensing model. Some portion of NPWR’s outsized expected return, then, can be explained by this high, unquantifiable level of risk.

2. Time: The expected payoff is decades in the future. It will be at least 5 years before NET Power is “worth” anything in the traditional sense of having significant revenues and profits. In an era in which almost all investing is done by institutions, and the average mutual fund holding period is less than 12 months, NPWR is almost inconceivable as an investment for almost everyone.

3. Float: With a market cap of only $2 billion and high institutional and insider ownership, there are not that many shares left to buy. Estimates of insider ownership vary from 60% to 100%. I would estimate that it’s ~80%, which means that NPWR’s real float is in the neighborhood of $500 million. In other words, despite the hype, NPWR is effectively a microcap stock, and thus outside the purview of most institutional investors.

These are exactly the types of situations which privilege retail investors who can take big risks, wait a long time, and invest in small companies.

Risks

The risks are many and hard to quantify. I see these as the most pressing:

- disruptive innovation: carbon capture is one of the central problems of the 21st century, and many people are working actively on solving it. It is very possible that better power plant designs or carbon filtration systems are commercialized in the next 20 years, denting NPWR’s profits.

- subsidies end: it is possible that governments do not have the political will or funding to subsidize carbon capture, and that NPWR’s plants are therefore not significantly cheaper than current plant designs, and are therefore unable to take significant market share.

- regulated profits: if NPWR is too successful, there may be a political backlash on the extent of their profits derived from government subsidies, and there could be higher taxes placed on their profits.

- natural gas: if natural gas reserves are rapidly depleted and the price of natural gas rise, NPWR’s designs might become uneconomical sooner than expected, or customers could shift to different power sources.

- execution: NPWR has not yet proven that they can design full-scale power plants, and technological or organizational roadblocks could prevent the commercialization of their technology.

- imitation: while NPWR has patents, the idea behind their plant design is public and could inspire imitation, cutting into licensing profits.

- funding: given NPWR’s powerful backers, I doubt that NPWR would run out of money accidentally. But if the economics don’t work, they may let it fail.

One additional risk is dilution, since the company does not yet have sales and could run out of cash. On the Q2 call, management explicitly addressed this, saying that the equity raise was priced to give NPWR the necessary capital to get through to 2027. As of Q3 2023, NET Power has $645 million in cash and no debt. Due to high rates, in Q3 interest income from NPWR’s cash position was enough to pay all operating expenses. Management expects CapEx to increase as they work towards developing their first full-size plant, but the costs are far below NPWR’s cash position: 2023 full-year CapEx is expected to be around $25-$30 million, which would be equivalent to a 4-5% interest rate on available cash, something very achievable in the current environment. Given that NPWR only needs this cash to last 3-5 years at most, I think the risk of dilution is not excessively high.

Rather than attempting to quantify these risks in a specific bear case scenario, I would just say that any one of them, much less several, could make NPWR basically worthless in ten years’ time. I am investing in it with ‘speculative’ capital, for which I am willing to accept the potential for a 100% loss. I would encourage readers to think about NPWR in these terms. NPWR’s valuation is a multiple of the number of plants which use their technology. If any of these larger shifts take place, making NET Power’s design not economically viable, I think that profits could well be negligible, and NPWR will not deliver competitive shareholder returns.

Bottom Line

NET Power owns a complete package of immensely valuable IP, and they are well on the way to commercializing it. NET Power’s technology offers a transformative new approach to power generation that doesn’t release carbon into the atmosphere. If they can successfully commercialize it as expected, the stock would become an amazing compounder, potentially generating annual returns of over 20% for the next 20 years. But if, for technological, economic, or organizational reasons, this commercialization fails, NET Power’s shares could become worthless. I think this high-risk, high-reward scenario is worth it for investors with a long time horizon and a strong tolerance for risk. Investors can take David Einhorn’s advice to manage their risk exposure by sizing their position appropriately. I plan to open a small position and will consider building a larger one over time as the commercialization process unfolds.

Read the full article here

")

")

")

")

")

2026-04-01")

")