")

(NYSE:PLTR)")

Thesis Summary

Palantir (NYSE:PLTR) has reported Q2 earnings in line with expectations, but the stock has dropped nearly 10% so far.

While the company has achieved its third consecutive quarter of profitability, growth has been lacklustre.

Wall Street analyst Dan Ives called Palantir the “Messi of AI”, but like the soccer player, who signed a deal with Inter Miami worth billions, this company is overvalued.

As a Real Madrid supporter, I may be biased about Messi, but when it comes to Palantir, I’m setting my emotions aside.

Palantir’s stock has more than doubled its price in the last six months, and the valuation is too rich. Furthermore, a sell-off is also supported by technical analysis.

I’m changing my Palantir rating from buy to strong sell based on this analysis, but I’ll be more than happy to buy more Palantir shares once we reach the $10 area, as I still believe in the long-term story for Palantir and AI.

Q2 Earnings Overview

Another quarter has flashed through us, and we are now halfway through 2023. Palantir reported Q2 results on August 7th. While these results are more or less in line with expectations, I personally find them disappointing, and I cannot continue to justify the current share price.

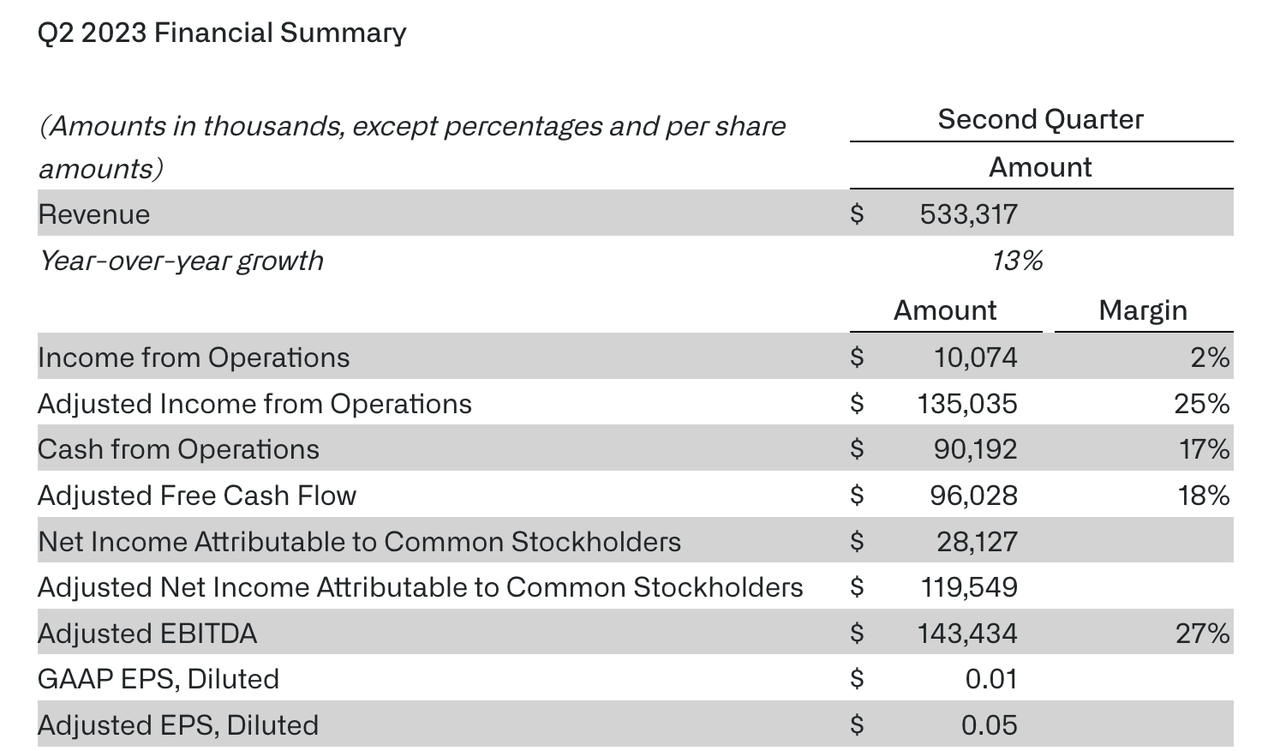

Financial Summary (Q2 earnings)

As we can see in the financial summary, YoY growth came in at a measly 13%. This, in my opinion, is pretty bad when we compare it to the growth rates from last year.

Granted, profitability has remained quite good, with the Adjusted EBITDA margin reaching 27% and another quarter of positive earnings.

Now, let’s look at some of the investor slides to try to gain some more insights into these results:

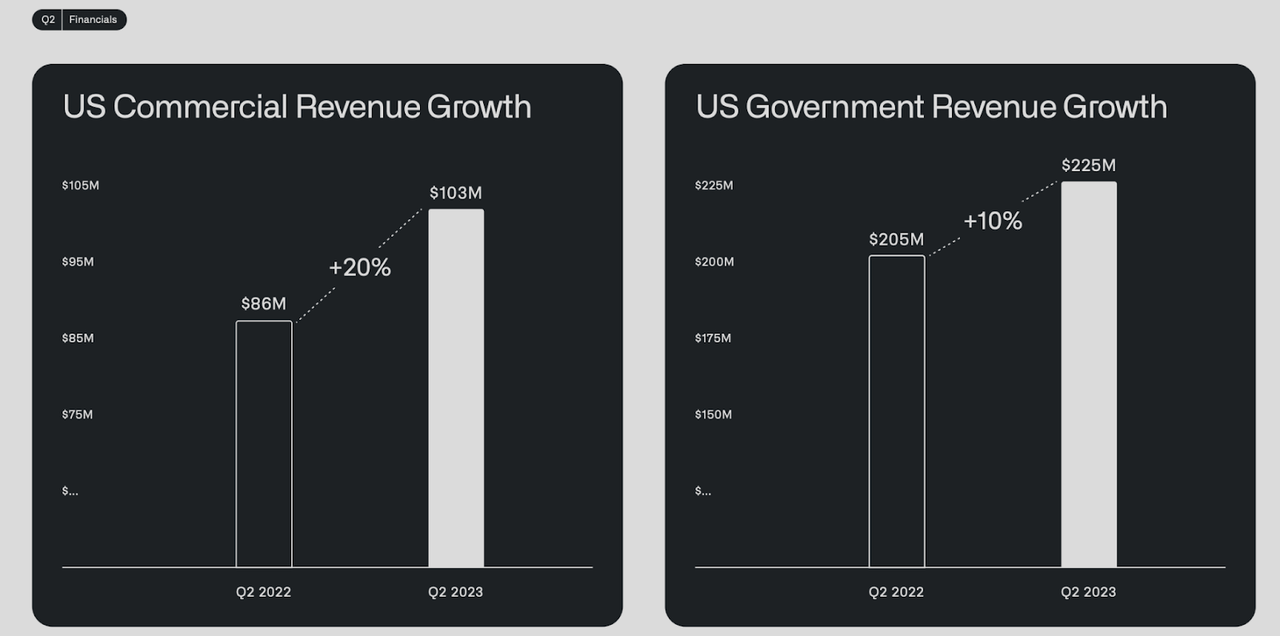

US Revenue growth breakdown (Investor slides)

In the Q1 presentation, we saw an encouraging acceleration of US revenue growth, which climbed 26% YoY towards $107 million. This quarter, we are up 20% from last year and down sequentially.

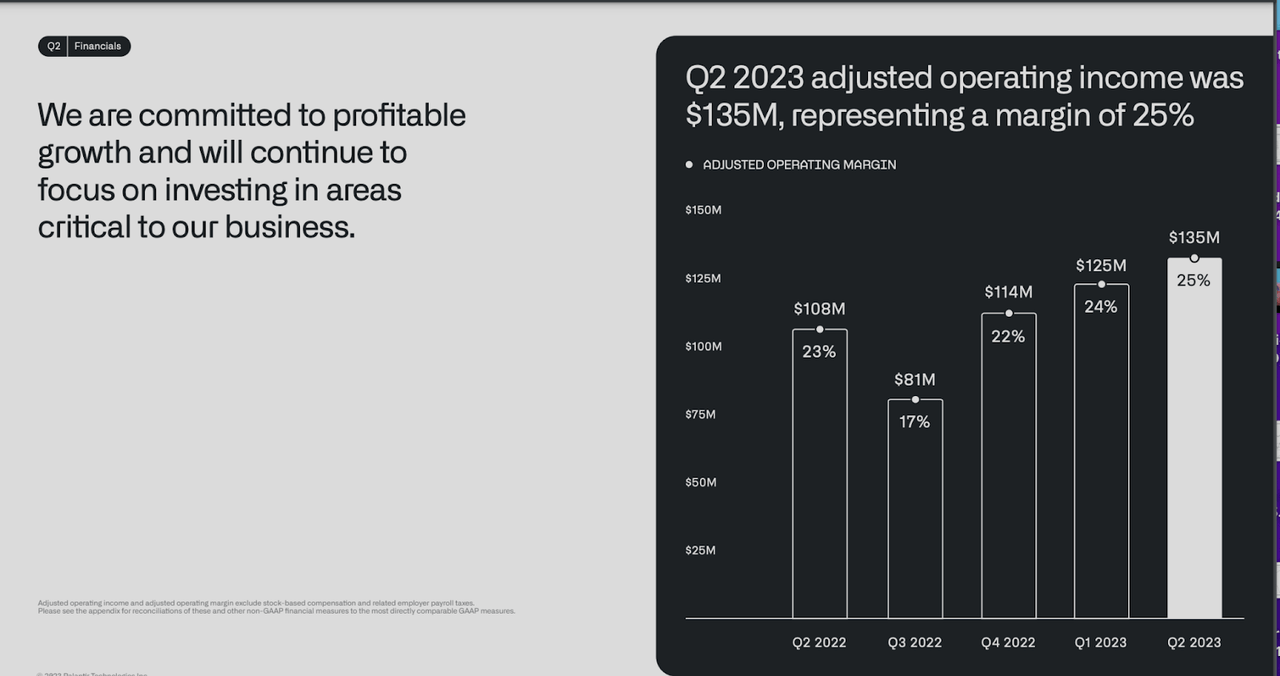

Operating income margin (Investor slides)

The silver lining here is that Operating Income continues to climb, even on a QoQ basis. Palantir achieved 25% OI this quarter.

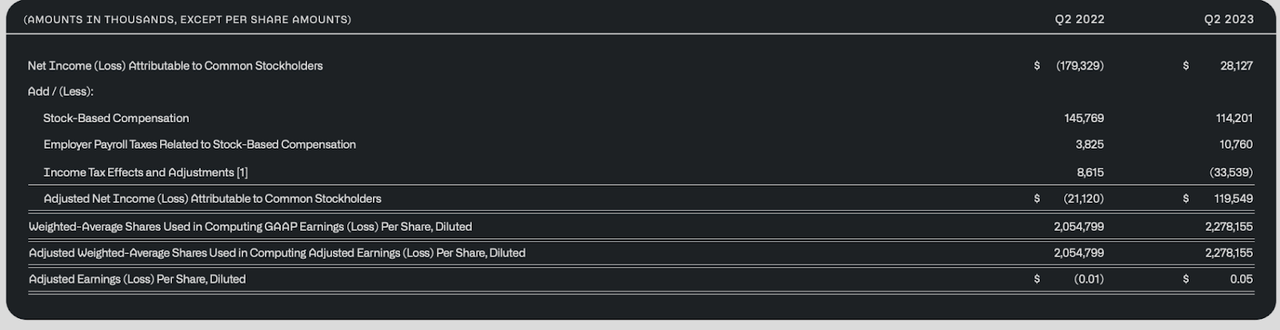

Net Income (Investor slides)

Lastly, it’s also with mentioning that Stock-Based Compensation continues to trend down. In Q2 of 2022 Palantir’s SBC had a cost of $145 million, while this quarter it was $114 million. This has been a key contributing factor in achieving GAAP profitability.

In conclusion, we can see a continued trend of increased profitability, but growth has been very disappointing. Even the US business segment is struggling, and this actually flies in the face of the AI growth story.

Has Palantir’s growth peaked, or can we expect more moving forward?

Karp’s Shareholder letter

Alongside the financial results, CEO Alex Karp issued his signature letter to shareholders.

Though I failed to see encouraging financial results, Karp’s letter does have in it some bullish takeaways:

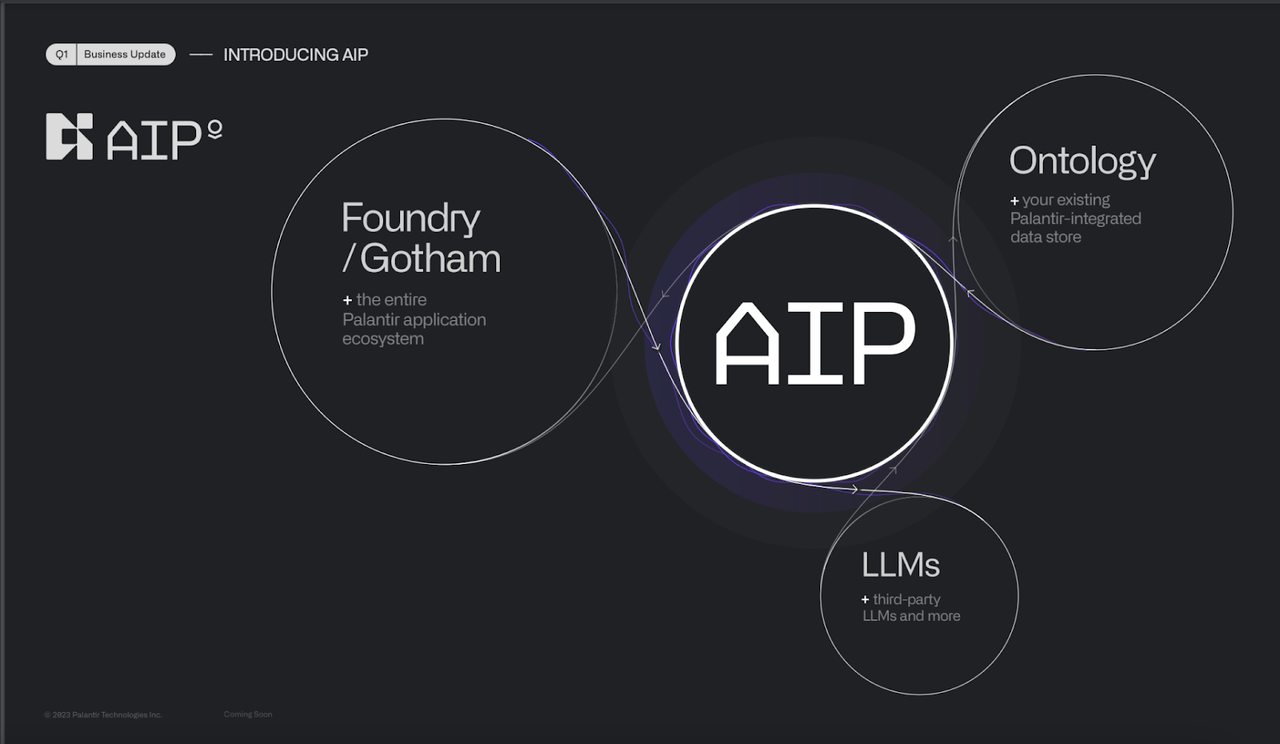

A few months ago, Palantir released its Artificial Intelligence Platform, which promises to bring the power of Large Language Models to its existing products:

AIP (Investor slides)

A scramble is taking place throughout the United States and around the world to deploy the software solutions that will allow institutions to domesticate the large language models that have thus far operated primarily in the wilds of the open internet…We have built the integration platform that they require, and the traction we are seeing, only months after its release, has been transformative for our company.

Source: Alex Karp, Letter to Shareholders

According to Karp, Palantir is in discussions with over 300 companies to deploy AIP. This should be a motor of growth for the future. I’ll believe it when I see it.

“We expect to remain profitable on both a quarterly and annual basis this year. As a result, we anticipate that we will become eligible for inclusion in the S&P 500 after we report our financial results for Q3 2023 in early November. At that point, we will have been profitable on a cumulative basis over the preceding four quarters.

Source: Alex Karp, Letter to Shareholders

On a good note, if Palantir achieves its objective of remaining profitable over the coming quarter, then the stock could be eligible for S&P 500 inclusion, which could act as a bullish catalyst.

With strength comes freedom.

Our board of directors has approved a common stock repurchase program, the first in our history as a public company. The program is authorized to repurchase up to $1 billion of the company’s Class A common stock.

The scale of the opportunity that lies ahead has increased significantly in recent months. And we intend to capture it.

Source: Alex Karp, Letter to Shareholders

And it’s also worth noting that the company intends to repurchase $1 billion in shares. However, I find the last sentence somewhat contradictory. If Palantir has such a large opportunity ahead of it, why is it repurchasing stock instead of reinvesting in itself?

Valuation and Technical Analysis

When I last wrote about Palantir, the stock had just released Q1 earnings and its price was close to $10. Since then, the stock has almost doubled, and the valuation doesn’t make sense anymore:

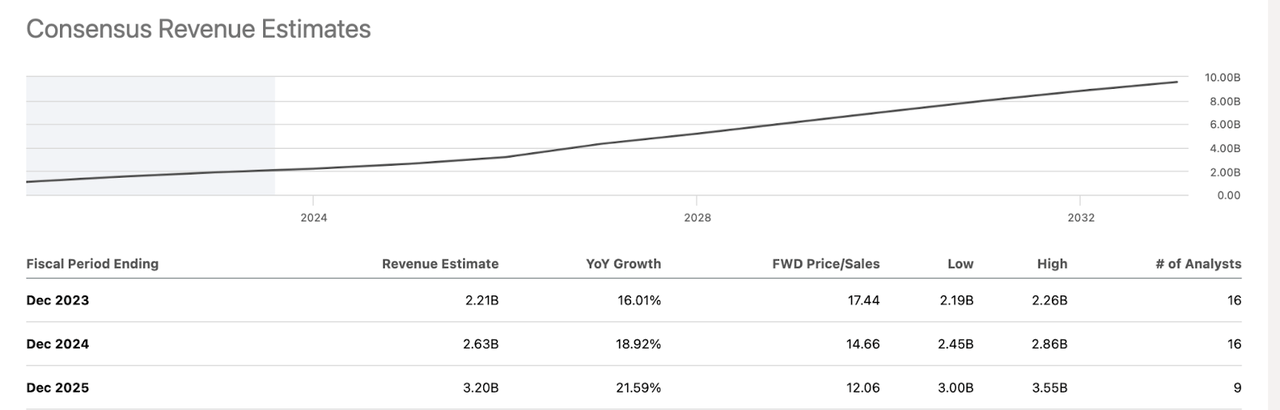

Revenue Estimates (Seeking Alpha)

Analysts estimate revenues will grow by close to 20% from here until 2025.

First off, this seems optimistic, given the current trend in earnings. However, even if we do apply a generous growth rate, Palantir is still trading at a 2025 P/S of over 12, which seems very generous.

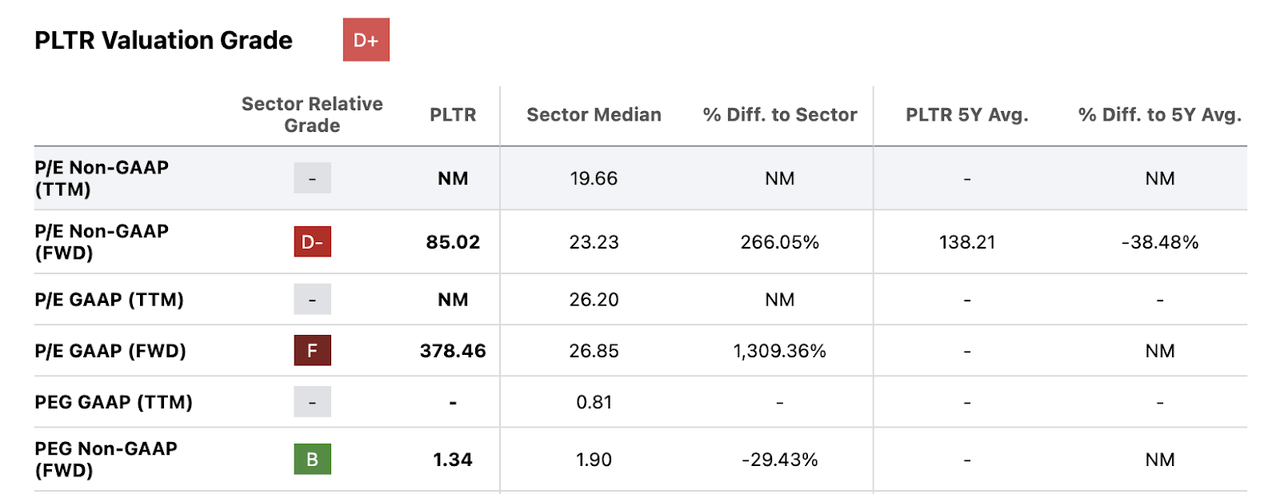

However, I will say that Palantir looks a lot less overvalued if we look at one of my favourite valuation metrics. Price-to-Earnings growth, or in this case, Fwd PEG:

PLTR Valuation multiples (Seeking Alpha)

Palantir currently trades at a 1.30 fwd PEG, which is actually below the sector median. Still, fair value would be a PEG of 1, which means that at the current price, PLTR is still around 25% overvalued.

In this situation, fundamentals and technicals line up nicely, as I also expect Palantir’s stock to sell-off in the coming weeks:

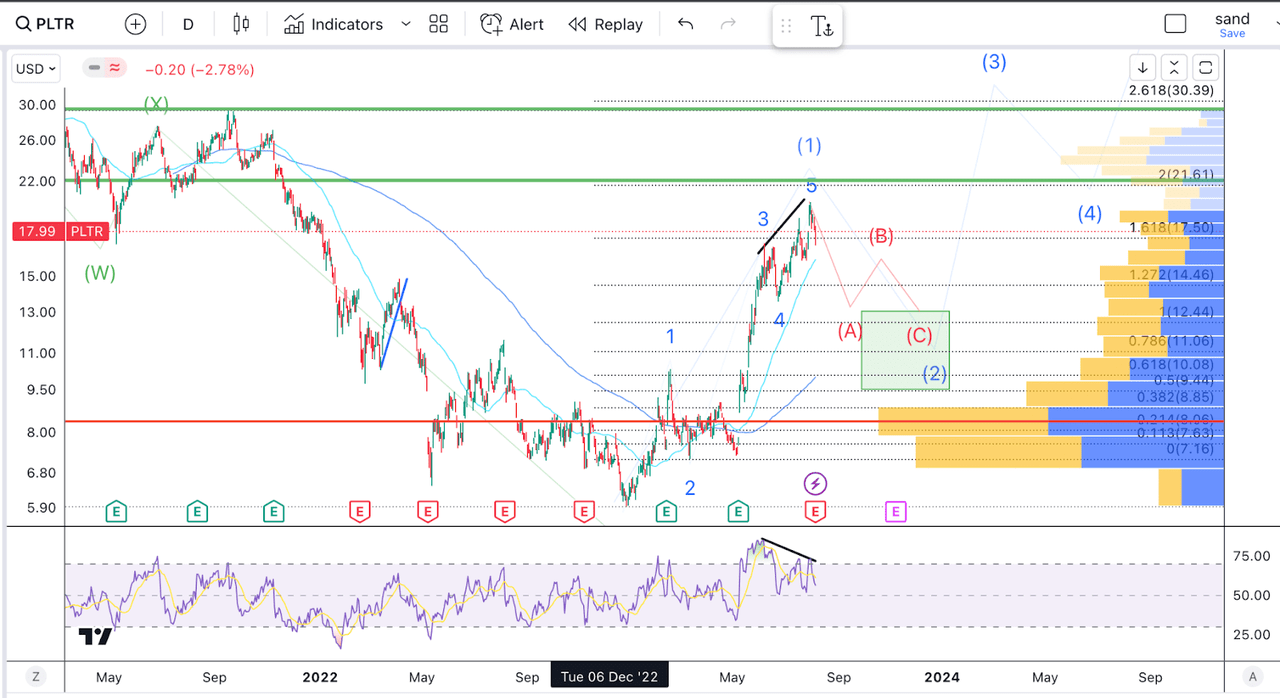

PLTR Technical Analysis (Author’s work)

As we can see in the chart above, Palantir’s stock has reached a natural point of inflection. First off, looking at our Elliott Wave count, we are nearing the 2 ext of our wave 1 measured from the bottom of 2. This would be a good target to finish the five-wave impulse we have been forming since we bottomed in December 2022.

A reversal around these levels also makes sense if we look at the VRVP: We have significant volume coming in the $22-$26 range.

And finally, we can see a bearish divergence in the daily RSI forming. I believe we could see PLTR attempt one more high into the $22 range, with the RSI getting back near overbought territory but further confirming the bearish divergence (failing to make a higher high).

If we measure the whole rally from the bottom, the 50% retracement level lands us a little under $11. This is also just above the 200-day MA, so I’d expect this to act as strong support.

Takeaway

Palantir is a great company, no doubt, but the “Messi of AI” has come too far in the last three months. The stock has doubled in price, and the recent earnings don’t support such a high price. Fundamentals and technicals line up here, and though I still hold some of my Palantir position, I’m looking to add more on the dip.

Read the full article here

")

")

")

Analyst/Investor Day Transcript")

")