")

Petróleo Brasileiro S.A. (NYSE:PBR) aka Petrobras recently announced a change in its dividend policy to 45% of free cash flow (“FCF”). However, on the other hand, the company also now has the ability to potentially increase its share buybacks. As we’ll see throughout this article, this is better for shareholders in the long run, with the company’s strong financials.

Petrobras Financial Results

Petrobras has continued to generate strong financial results.

Petrobras Investor Presentation

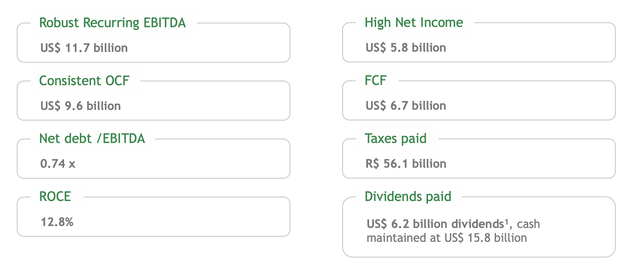

The company earned almost $7 billion in FCF, or almost $30 billion annualized. That’s in a much weaker oil price environment, when the company’s earnings dropped substantially. The company has maintained a strong cash position and paid out a massive $6.2 billion in dividends in the quarter. That’s a roughly 7% dividend yield for the quarter, an incredibly strong rate.

The company’s Q2 results were partially impacted by massive tax payments. However, overall, the company has remained committed to strong financial returns for shareholders and maintaining a reasonable financial picture.

Petrobras Volatile Environment Earnings

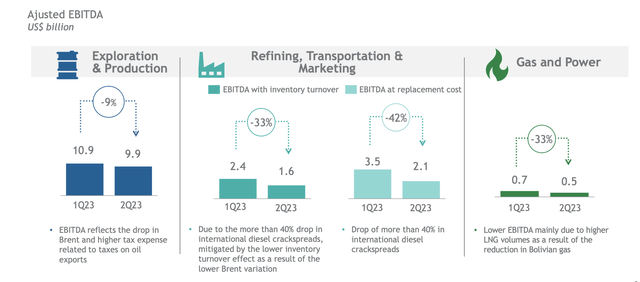

The company’s earnings have been volatile, but upstream earnings have actually been a lower impact than refining.

Petrobras Investor Presentation

The company’s largest impact to its earnings was refining, transportation, and marketing, as crack spreads decreased substantially. That’s not surprising given that crack spreads were substantially above normal in recent quarters and prior years. Of course, that poor performance was impacted by weakness in gas and power and e&p as well.

However, the takeaway is the company’s earnings decrease is unlikely to decrease by the same amount going forward.

Petrobras Cash Flow Strength

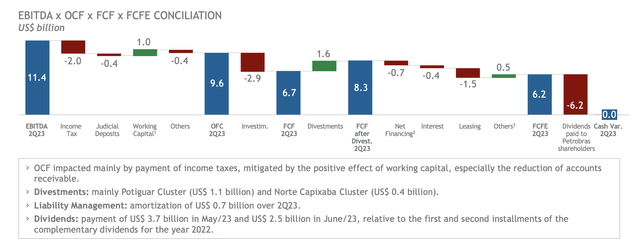

The company’s cash flow picture provides an indication of how strong its financials have remained.

Petrobras Investor Presentation

The company’s $11.4 billion in EBITDA turned into $9.6 billion in OFC. The company continued to invest heavily in its portfolio, with more than $11 billion in investments. The company had a 13% reinvestment rate on its market capitalization, a high investment that shows the continued strength of its portfolio.

The company’s divestments helped it pull its FCF to $8.3 billion ($6.2 billion in FCFE after a variety of expenses). The company spent that all on dividends to end up with no cash variance. These are continued massive investments in shareholder returns, with a comfortable double-digit shareholder return rate.

Petrobras Debt

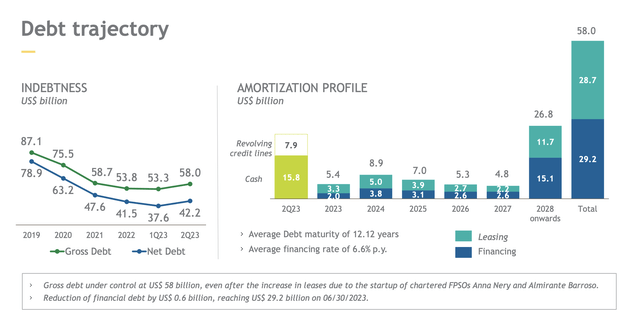

The company’s debt was once a concern for the company, but it’s improved substantially.

Petrobras Investor Presentation

The company’s net debt has dropped to a mere $42.2 billion as the company maintains a strong cash position on hand for any uncertainties. The company’s debt due per year is minimal, with a 12.1 year average maturity, and enough cash for the next 3-years. However, the company’s earnings each year is still enough to cover debt due.

The company’s 6.6% financing rate is relatively high, but we think the company should just pay-off its debt as it comes due versus trying to refinance.

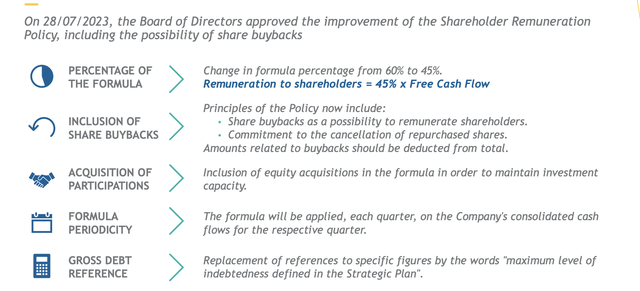

Petrobras Shareholder Returns

The company is focused on increasing shareholder returns, from this impressive portfolio of assets.

Petrobras Investor Presentation

The company is decreasing its FCF from dividends from 60% to 45%. However, the company is enabling additional FCF to be used for share repurchases, which in our view is substantially overdue. Share buybacks at the company’s current rate of return will enable much more substantial long-term shareholder returns.

The company’s FCF is comfortably in the double-digits as investors continue to worry about geopolitical and political risk. We expect that the company, with its debt at its target level, will be able to drive substantial shareholder returns.

Thesis Risk

The largest risk to our thesis is crude oil prices. The company’s profits took a big impact from oil prices and the negative impact on refining spreads. However, that’s after Saudi Arabia has put a lot of effort into support prices and cutting production. There’s no guarantee that’ll continue especially with a demand decrease, which could substantially hurt earnings.

Conclusion

Petrobras has a unique and impressive portfolio of assets. The company is rapidly reorienting around low-cost production, improving its margins, while growing overall production. At the same time, the company is building a strong integrated asset portfolio enabling it to increase refining and midstream margins to generate strong overall returns.

The company’s debt load is at an incredibly manageable level with its long-term goals. It can pay-down its debt from cash as it comes due. The company continues to maintain a strong cash position due to the risk in the industry. At the same time, the company’s reduced dividend enables share buybacks, which at its current valuation, we expect will result in much higher returns.

Overall, the company is a valuable investment.

Read the full article here

")

")

Analyst/Investor Day Transcript")

")