")

")

Robinhood (NASDAQ:HOOD) initially captured the spotlight as a platform reshaping how people invest in stocks. Reaching peak attention during the meme stocks frenzy in 2021, the company has undergone restructuring and significant transformations since then. What once was just an accessible gateway to the markets and a way to trade options on meme stocks has evolved into an efficiency-focused corporation that is attractive for long-term investment. The results of this can already be seen in the latest financial results for Q2 2023.

Robinhood’s focus on operational excellence is brutal but necessary

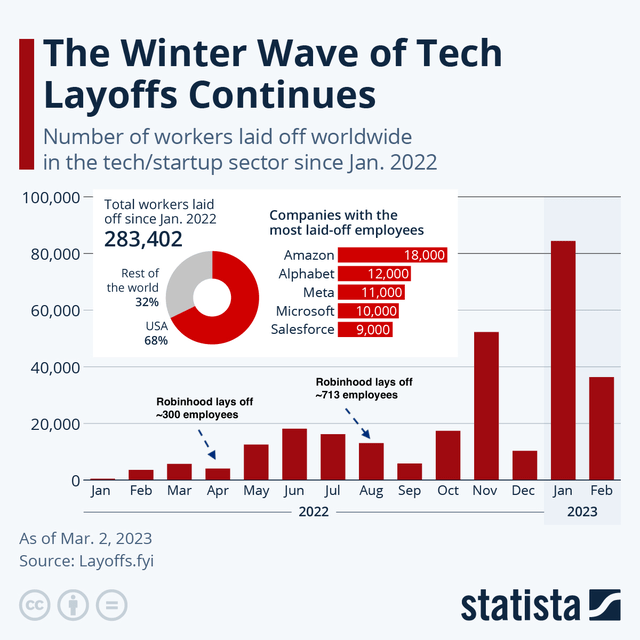

Robinhood was one of the first companies in 2022 to do mass layoffs, slashing its workforce by 9% (around 300 workers) in April and another 23% (or about 713 employees) in August. In total, the corporation reduced its workforce by more than 1000 people in just 3 months, which, according to the company, impacted all functions.

To remind, in the first half of 2022, mass layoffs were still seen as something extraordinary, and the extent of the economic slowdown we experience today was not that clear yet. For example, “only” around 5,800 workers were laid off in tech in April 2022, compared to ~50,000 in November the same year, ~100,000 in January 2023, and ~30,000 in April this year. (the exact numbers vary depending on the source)

Number of workers laid off in the tech/startup sector between Jan 2022 and Feb 2023 (Statista, commentary by the author)

Furthermore, at the end of Q2 this year, the corporation did another, 3rd round of layoffs, cutting its workforce by another 7%.

Yes, these measures are undeniably adversary for the affected workers, and some of it could have potentially been avoided with better strategic planning. However, from a corporate governance standpoint, the management’s early recognition of the need for reorganization, anticipation of the slowdown, and willingness to implement these unpopular measures represent positive indicators for shareholders.

The latest quarterly report shows Robinhood is cracking the code of profitability

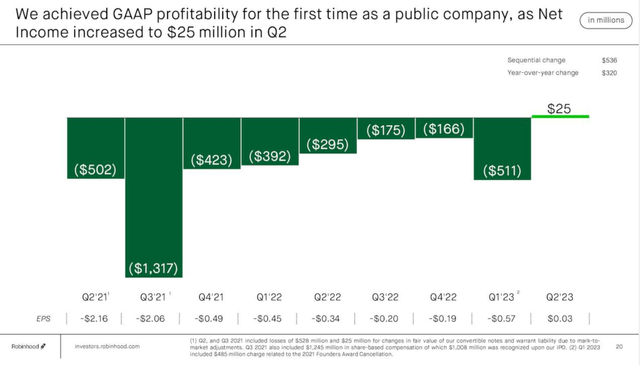

The company’s actions outlined above have already impacted the bottom-line financial efficiency, evident by the latest quarterly report: earlier this month, Robinhood released its financial results for Q2 2023, surpassing expectations for both revenue and earnings.

Here is the key headline: ~53% year-over-year revenue growth and, for the first time since the company went public, positive EPS – Robinhood has achieved GAAP profitability.

Robinhood Q2 2023 earnings presentation

GAAP profitability is a critical milestone for the corporation, especially in the current market:

- Investors tend to focus on value plays, and profitability is the number-one priority for most investors at the moment. By achieving positive GAAP EPS HOOD stock will get onto the watchlists of many additional investors, which can catalyze the stock’s growth.

- This achievement demonstrates that the strategy is working and validates Robinhood’s viability as a business.

- Profitability was achieved despite ongoing product improvements (more on that later in the article), which are usually expensive. This means the company did not need to compromise on quality to achieve favourable financial numbers.

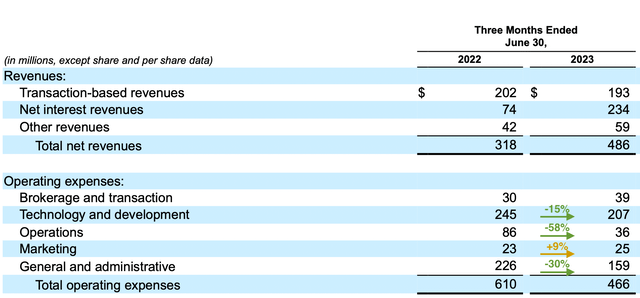

On the revenue front, growth was primarily driven by net interest revenues, which increased by 13% from the previous quarter and 216% year over year, totaling an impressive $234 million. More specifically, interest on corporate cash and investments and interest on segregated cash and deposits were the primary growth drivers, surging 640% and 767% year over year, respectively.

However, I would like to focus our attention on the cost structure.

The cost reduction measures are paying off

The impact of the company’s efficiency-focused measures is evident in the report: Robinhood’s operating expenses went down by a significant 24% in Q2 2023, compared to the same period last year. In comparison to revenue, operating expenses were 192% of revenues in Q2 2022 and 96% in Q2 2023. This illustrates where HOOD’s profitability came from.

The decrease is noticeable across all expense categories, with operations-related expenses making the most significant impact, showing a 58% reduction. General and administrative costs decreased by 30%, providing reassurance to investors after a substantial increase in Q1 2023, driven by a $485 million share-based compensation expense related to RSU cancellations. Technology and development costs also decreased by 15%, despite aggressive delivery on the product roadmap.

Robinhood Q2 2023 10-Q, notes by the author

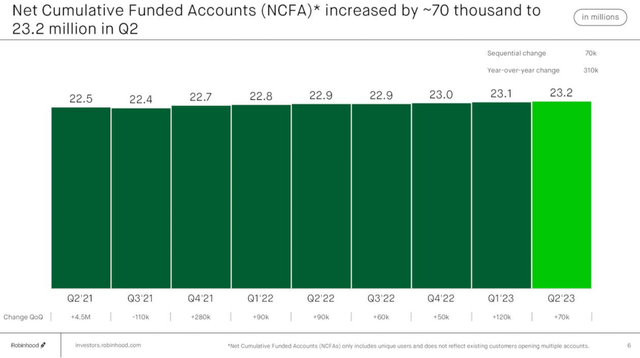

Moreover, marketing expenses remained relatively low and only increased by 9%. Importantly, low marketing expense didn’t hinder the company from expanding its Net Cumulative Funded Accounts, one of the key measures signifying the number of long-term users, in the quarter.

Robinhood Q2 2023 earnings presentation

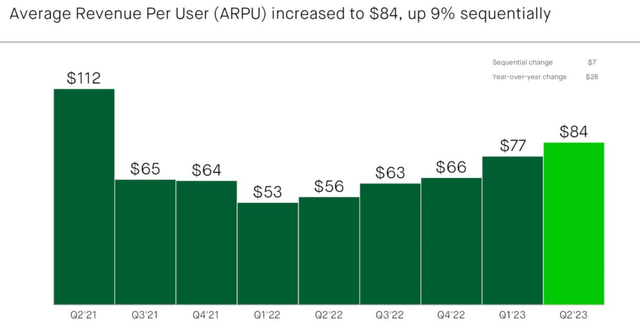

Revenue per user is rebounding higher towards the levels seen during the pandemic-driven trading activity

Another key metric we should keep our eyes on is average revenue per user. Robinhood has shown significant progress in getting ARPU closer to the levels seen during the pandemic, when ARPU fluctuated around $100-110.

The general trend here is encouraging: Q2 2023 was the sixth quarter in a row with positive ARPU growth. The metric reached $84 during the period, which is the highest in 2 years.

Robinhood Q2 2023 earnings presentation

One of the sources of ARPU growth was Robinhood Gold offering. It can be expected that with more premium features being added to Gold, we will see further increase in ARPU.

As we’ve attracted and engaged more Gold customers, we’ve seen them deposit more into their Robinhood accounts. And this continues to drive strong ARPU and revenue growth from our Gold customers.

Robinhood’s future appears promising, with ample growth opportunities on the horizon

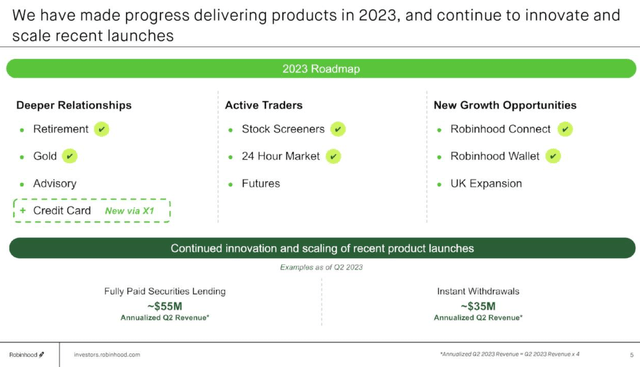

Notably, cutting down the workforce also did not slow down Robinhood’s product development. Over the last year, the platform has successfully rolled out such trader tools as 24-hour access to the markets and stock screeners, new opportunities like Robinhood Connect, Robinhood Gold and Robinhood Wallet, and enabled new products like Retirement (with matched IRA).

Robinhood Q2 2023 presentation

Retirement is a particularly compelling product, which can be a solid source of growth for the company in the future.

It is no secret that Robinhood has garnered particular popularity among younger audience, with 80% of its user base being under the age of 35, many of whom are first-time investors. As the users progress through different life stages, they will need a reliable place to keep their retirement savings. A familiar and engaging platform that they’ve been accustomed to over the years seems like the perfect fit. This combination of financial security and sticking with the platform could make the retirement option a strong and lasting source of income.

As a reminder, in January, we launched Robinhood Retirement, the first IRA with a 1% match, no employer necessary, and it’s great to see that IRA assets are now close to $1 billion. We believe retirement can grow into a much larger part of our business, especially as we add additional products like Advisory. (source)

Other promising innovations include 24-hour trading and IPO access, which can establish new revenue streams and attract an entirely new customer base. Given that 24-hour trading is particularly popular during the earnings season and was only made available in July, an uptick in revenue from this product is likely to be seen in the upcoming quarterly results.

We finished the rollout to 100% of our customers in July and we love the early uptake we see. We’ve seen strong volumes in our extended hours offering, particularly during earnings season, and Robinhood 24 Hour Market makes it even easier for customers to trade whenever they want.

HOOD’s valuation and price action suggest there is solid room for growth

Now, let’s talk about valuation. Currently, Robinhood stock trades at about 5 P/S ratio and ~94 forward P/E (based on 2024 projections). This is certainly not cheap.

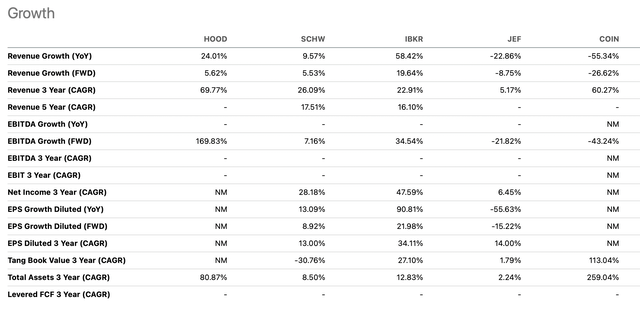

However, the valuation does not look that crazy when factoring in potential growth and further progress towards profitability. Among its peers, Robinhood has one of the highest current revenue growth rates, the greatest revenue growth potential in the next 3 years, and the most substantial forward EBITDA growth.

Seeking Alpha

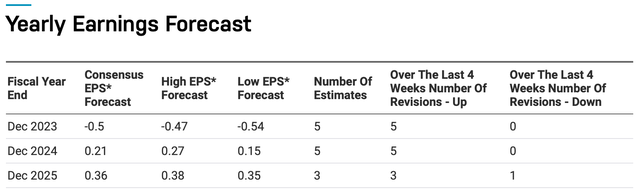

If we assume Robinhood will continue focusing on profitability (which is likely, given the recent round of layoffs) and sustainable revenue growth, we can expect 2025 EPS to reach as high as $0.5. Now, the consensus 2025 EPS forecast sits at around $0.36, but Robinhood tends to beat on EPS more often than not.

Nasdaq

With the market expecting 40-50% annual earnings growth, forward P/E ratio should also be approximately 40 to maintain a PEG ratio of 1, which is regarded as the “golden standard.” Consequently, by combining the projected 2025 EPS range of $0.36-0.5 with a forward P/E ratio ranging from 35-45, we arrive at a conservative price target of $12.6, a realistic target of $17.2, and an exceptionally bullish target of $22.5 by the end of 2024.

The recent price action also appears to validate bullish sentiment in the stock. HOOD’s price has been fluctuating around $10 over the last 1-1.5 years. However, we are now seeing that significant upward moves are usually coupled with rising trading volumes, while volumes are going down if the stock price declines. This indicates a potential alignment between bullish sentiment and higher activity, while reduced volumes during price declines may suggest a lack of conviction in downward movements.

TradingView, notes by the author

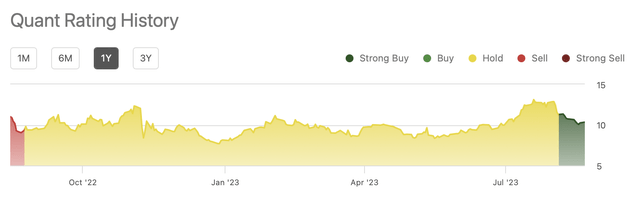

Notably, Seeking Alpha quant rating also switched its recommendation to Strong Buy for the first time during the recent selloff, confirming the point we made above. This was driven primarily by growth, price momentum, and target revisions by analysts.

Seeking Alpha

Risks

It is worth outlining the risks that can impact HOOD’s performance in the near- to medium-term future.

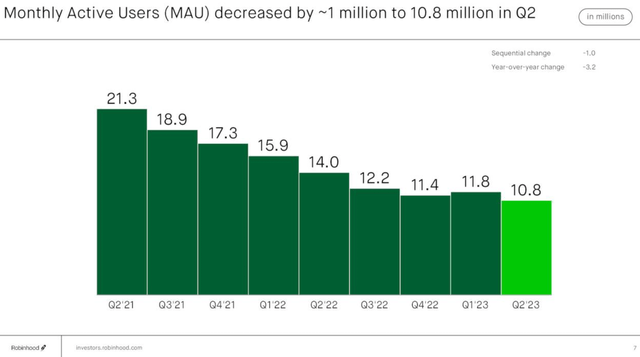

First of all, monthly active user numbers are volatile and have been declining since the pandemic. In Q2, Robinhood reported 10.8 million MAU, which was ~1 million lower sequentially and ~3.2 million lower year over year. While new product features and a potential bull market could rejuvenate growth, the current trend is concerning.

Robinhood Q2 2023 earnings presentation

Secondly, Robinhood’s performance is significantly influenced by the overall state of the economy: it can be assumed that the downturn in the markets we have seen in the last 1.5 years has negatively affected the number of individuals willing to trade and invest. It can take a while for the market to recover, which means Robinhood’s core business will continue to experience headwinds in the near term.

Finally, in the realm of investment platforms, it is paramount for Robinhood to uphold its reputation and cultivate user trust, especially among younger generations that will be the engine of the company’s future growth. Robinhood’s reputation took a hit due to its practices during the meme stock frenzy, and a similar situation might potentially occur in the future. Such missteps can prove costly, as retaining funds on a platform requires complete trust in this platform’s ability to act in the users’ best interests.

Key takeaway: HOOD presents a solid risk-reward opportunity

Even though there are certain risks that could potentially hinder the company’s performance, the stock’s significant upside potential renders it an appealing option for long-term investment. Robinhood has successfully navigated shifts and challenges in the markets, making the company more lean and efficient and achieving profitability in the process. Despite significant cost and workforce reductions, Robinhood has continued to deliver on its ambitious product roadmap and has launched several key products, such as Retirement and 24-hour trading, which should help the company diversify its revenue streams and ensure future expansion.

With the stock price down over 70% from its IPO levels, coupled with enhanced profitability, robust revenue growth, and a healthy balance sheet, the downside risk appears limited. Therefore, HOOD stock can be recommended as a buy, presenting roughly 60% upside potential in the upcoming 2-3 years.

Read the full article here

")

")

")

")

")