")

")

")

Intro

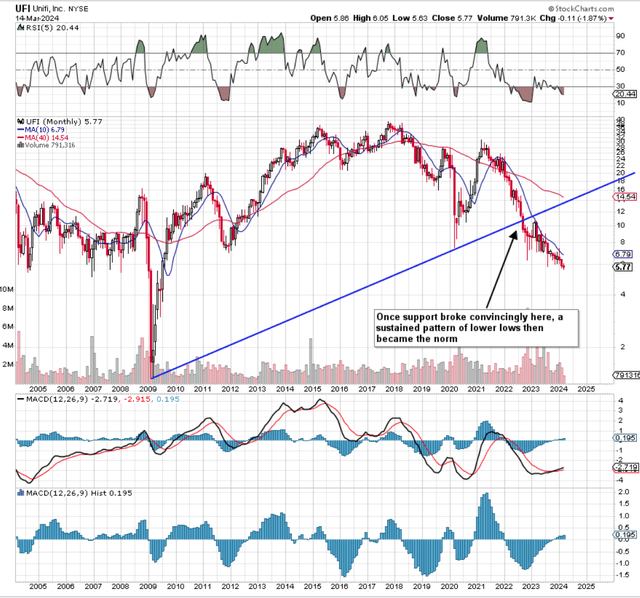

We wrote about Unifi, Inc. (NYSE:UFI) in July of 2022 when we rated the recycled & synthetic product manufacturer a ‘Hold’ for several reasons. Despite sporting a keen valuation at the time, the company’s margins remained under pressure due to US staffing constraints as well as the elevated cost of goods sold. To combat pressurized margins, companies such as Unifi must turn over as much product as possible (through elevated volumes) so economies of scale can somewhat compensate for higher input costs over time. Nevertheless, Unifi at the time was also being affected on the volume side primarily in the Asian region due to sustained pandemic-related lockdowns.

Suffice it to say, given the growth & profitability challenges Unifi was dealing with at the time, the jury was still out on whether shares would be able to maintain multi-year technical support. As we see below, however, long-term support failed pretty comprehensively soon after our 2022 commentary as buyers failed to come to the rescue at approximately $11 a share. This convincing loss of support led to consecutive months of lower lows in the stock resulting in shares being down roughly 58% over the past 20 months or so. This is a sizable opportunity cost considering the S&P500 has risen by close to 29% over the same timeframe.

UFI Long-Term Technicals (Stockcharts.com)

Q2-2024 Earnings

In the company’s recent second quarter announced on the 1st of February this year, $136.9 million was reported in net sales on negative earnings of ($19.8) million. Although the top & bottom-line numbers were closely aligned to the same period of 12 months prior, green shoots may be beginning to form although Unifi remains at the behest of the market conditions it sells into.

Firstly, to protect the income statement, management’s accelerated cost-cutting initiatives have begun to positively impact gross margin. Furthermore, more gains are expected here due to an overhaul of the sales process, improved streamlining as well as a more prudent inventory management model. Moreover, through a sustained reduction in headcount as well as multiple high-level appointments, Unifi aims to become a far more efficient outfit with innovation remaining at the forefront.

Whether a plethora of innovative offerings in the likes of REPREVE & the Beyond apparel areas can result in growth in a cost-cutting environment remains to be seen. From our standpoint, we believe investors need to see significant improvements in both Unifi’s gross margin & free cash flow before shares can begin a sustained move higher.

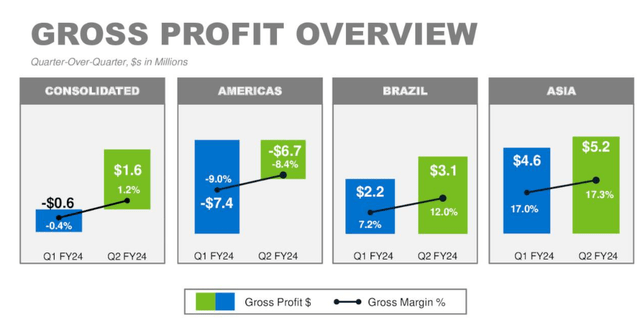

Gross Margin

The encouraging trend from a margin standpoint is that gross profit ($1.6 million in Q2), as well as gross margin (1.2% in Q2), improved in Q2 this year both from a sequential standpoint as well as compared to the same period of 12 months prior. Given how interest expense has been rising upward at the firm, it is imperative to keep gross profit moving higher. The CFO explains below the uptick in this key metric on the Q2 earnings call this year.

Lower raw material costs and variable cost management efforts provided for overall improved profitability. However, the seasonally lower volume and weak apparel demand environment in the Americas, combined with the selling price pressures in Brazil continued to unfavorably impact gross profit. Variable cost management benefited the Americas and Brazil segments in Q2.

Unify Q2-2024 Gross Profit Overview (Seeking Alpha)

Irrespective of Unfi’s forward-looking growth plans, continued growth in REPREVE looks like the fastest way to boost profitability. In Q2, REPREVE sales grew both sequentially & compared to the same period of 12 months making up 33% of the total top-lie take. One would feel that sustained growth here will need to take place alongside a recovery in the Chinese economy plus an uplift in apparel production in general.

Free Cash-Flow Is A Powerful Valuation Driver

Given that the company reported a negative free cash flow of ($0.42) in Q2 this year, it was not surprising to see Unifi’s net debt position increase by almost $7 million in the quarter. This goes back to our previous point when we stated that doubts remain whether Unifi can grow significantly in a low-investment environment. For example, only $3 million was spent on capital expenditure in Q2 this year as opposed to $12.8 million in the same quarter of fiscal 2023.

This ‘low-investment’ environment is the key concerning the company’s valuation for the following reasons. Although the company’s sales & book multiples remain compelling as we see below, they do not truly represent Unifi’s inherent value as an investment due to the company’s inability to report positive earnings & cash flow as well as the low-investment dollars. This begs the question (notwithstanding elevated working capital commitments) whether it is a mistake by management not to invest aggressively through this latest downcycle.

| Multiple | UFI | Sector Median | UFI 5-Year Average |

| Price To Sales (TTM) | 0.18 | 0.94 | 0.43 |

| Price To Book (TTM) | 0.36 | 2.15 | 0.82 |

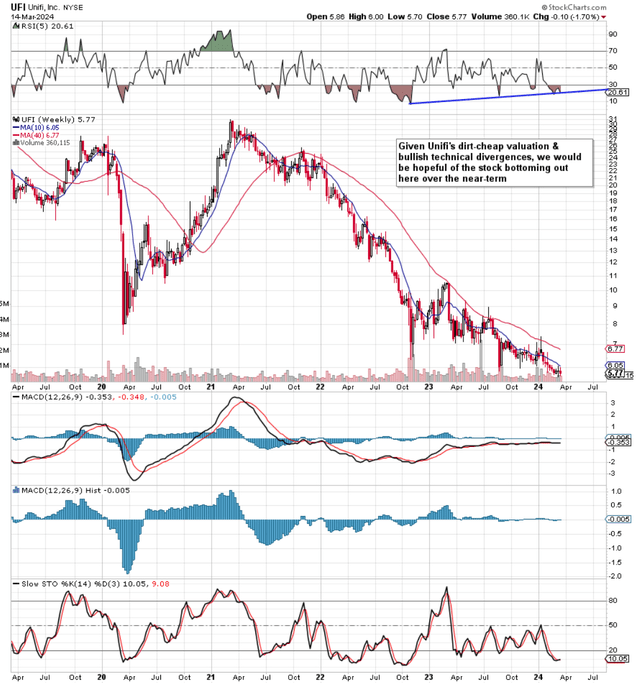

Intermediate Golden Cross Required

A sustained rise in both gross margin & free cash flow should result in the stock finally being able to put a halt to the bear market shown below. The first technical sign of a potential long-term multi-year bottom in Unifi would be an intermediate golden cross (bullish crossover of the stock’s 10-week moving average above its 40-week counterpart) on strong buying volume.

Unifi Intermediate Technicals (Stockcharts.com)

Conclusion

To sum up, Unifi has experienced a horrid time since topping out in March’2021 losing close to 80% of its market cap in the process. The capitalization of the stock in recent years means that one can now attain almost $3 in the company’s assets & more than $5 of the company’s sales for every $1 invested in the company. This looks like an excellent deal considering the lack of intangibles & goodwill on Unifi’s balance sheet. However, as outlined above, the lack of positive earnings & cash flow along with the reduction in capital investment means investors should wait here for the tide to turn. let’s see what the third quarter brings. We look forward to continued coverage.

Read the full article here

")

")

")

")

2026-04-01")

")

")