")

The once-a-decade opportunity in Verizon Communications Inc. (NYSE:VZ) remains valid despite getting hit this month due to the headwinds from its lead-sheathed cables network. Keen investors should recall that the Wall Street Journal’s or WSJ’s investigation had led to a massive selloff in the stock of leading telco operators like AT&T (T) and VZ as investors parsed the potential legal liabilities and clean-up costs that could follow.

I covered the matter in a previous update. As such, investors unfamiliar with the coverage can refer to it for more information. Analysts on Verizon’s recent second quarter or FQ2 earnings call were palpably concerned, as they took turns to ask management about the potential impact of the lead cables issue. However, given the current state of affairs, the company was reticent to provide a detailed response. Still, it highlighted that “Verizon is taking this matter very seriously and is conducting scientific and fact-based assessments.” In addition, management also informed investors that the company has engaged third-party experts to “review and measure the potential exposure to lead.”

The Department of Justice or DoJ and the Environmental Protection Agency or EPA have moved forward with their investigations on the issue, putting more pressure on Verizon and its exposed peers to accelerate their investigation and provide more clarity. In addition, the EPA “has issued a directive to AT&T and Verizon, demanding inspections, investigations, and environmental sampling data concerning their lead cables within 10 days.”

As such, investors assessing the recent opportunity in Verizon must continue to keep tabs on the developments on the lead cables as they unfold. Despite that, I believe the market has already reflected significant pessimism in VZ’s price action, even as it stymied its initial attempt to bottom out in June. Notwithstanding that failed attempt, VZ dip buyers returned robustly since last week as they attempted to hold the critical $34 zone.

With that in mind, I parsed that investors are likely assured with management’s commentary at its recent earnings call, suggesting that Verizon is on track to meet its full-year guidance.

Accordingly, Verizon delivered a solid performance in Q2, with an adjusted EPS of $1.21, surpassing analysts’ estimates. The company also improved its underlying metrics, posting an addition of 8K postpaid phone net adds, reaching 612K retail postpaid phone subs.

Notably, its critical average revenue per postpaid account or ARPA rose by 4% YoY and 1.5% QoQ. As a result, it delivered a 3.5% growth in wireless service revenue, as Verizon benefited from its pricing action and more fixed-wireless or FWA adoption.

The company is confident that its FWA target rate of 4.5M subscribers at the midpoint by the end of 2025 is achievable, up from 2.3M subscribers in the recently reported quarter. The company has also started segmenting its FWA business, further customizing its offerings to potentially improve ARPA. Coupled with its 400K broadband net adds, I assessed Verizon’s first-half growth underscored the market’s confidence that its full-year guidance should be achieved.

Despite that, the market’s concern about the lead-sheathed cables continues to dominate recent pessimism, and justifiably so. Risk-averse income investors have likely bailed out or stayed on the sidelines as they anticipate the worst outcomes leading to a significant increase in CapEx or a dreaded dividend cut.

While management’s outlook suggests that it expects its CapEx projections to have peaked, uncertainties in the lead cables issue could inflict more unforeseen expenses subsequently. Despite that, with VZ falling to a new low in July, it’s hard for VZ bears to argue that the market didn’t reflect such challenges as it attempts to price in Verizon’s exposure.

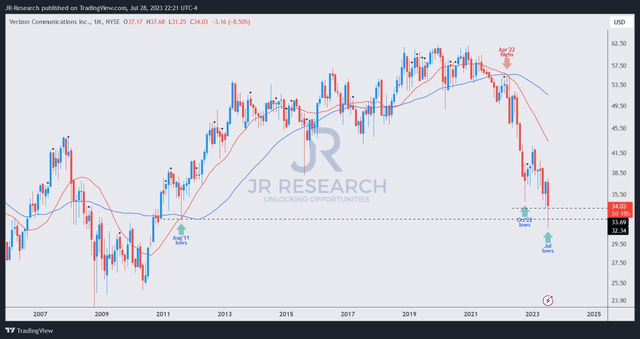

VZ price chart (monthly) (TradingView)

VZ’s “A-” valuation grade, rated by Seeking Alpha Quant, suggests it isn’t demanding. As such, significant bottoming opportunities should be assessed, corroborating that value-seeking dip buyers have returned as they attempt to defend against market pessimism, as VZ weak holders capitulated.

As seen above, VZ fell below its August 2011 lows this month, taking out more than ten years of gains in the process, likely spooking many investors to give up as they anticipated more punishment.

Despite that, VZ dip buyers returned as they fended a further selloff, helping VZ recover the $34 level, incidentally VZ’s June 2023 lows. As such, I believe it’s a pivotal development, indicating that VZ’s June lows are a significant level that attracted robust buying sentiments. Coupled with management’s strong execution and confidence about turning the tide in the second half, I maintain my conviction about the current buy levels for VZ.

Therefore, investors waiting for more robust buying support before returning should leverage VZ’s constructive price action to add more shares.

Rating: Maintain Strong Buy.

Important note: Investors are reminded to do their due diligence and not rely on the information provided as financial advice. Please always apply independent thinking and note that the rating is not intended to time a specific entry/exit at the point of writing unless otherwise specified.

We Want To Hear From You

Have constructive commentary to improve our thesis? Spotted a critical gap in our view? Saw something important that we didn’t? Agree or disagree? Comment below with the aim of helping everyone in the community to learn better!

Read the full article here

Q4 2025 Earnings Call Transcript")

")

")

")