Fixed income credit markets play a vital role in enabling issuers to access capital while offering investors the opportunity to earn excess returns by taking on additional risk.

Treasury bonds provide investors with yields based on prevailing interest rates, but corporate bonds may carry an additional premium based on the issuer’s creditworthiness, among other factors. Higher yields for corporate bonds generally correspond to higher credit risk based on an issuer’s credit rating.

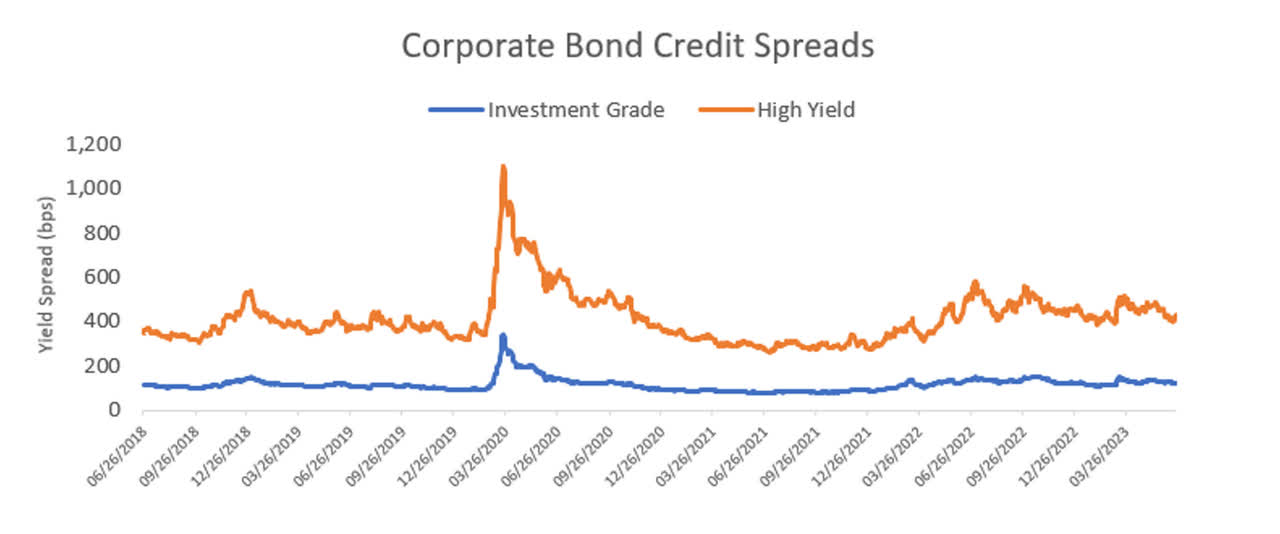

While 2022 was a challenging year for fixed income markets that resulted in credit spreads increasing significantly, particularly for high-yield issuers, higher yields have offered investors additional sources of income return and a higher cushion to protect from price declines from rising interest rates.

The spread increase over Treasuries was due to various factors, including the U.S. Federal Reserve (Fed)’s aggressive interest rate hikes, fears of persistent inflation and a global growth slowdown, pressure on corporate balance sheets, and tightening banking and lending standards.

Source: Barclay’s data; Bloomberg U.S. Credit Index, Bloomberg High Yield Bond Index, based on option-adjusted spreads.

What opportunities do higher yields present?

When credit spreads widen, it can signal that investors are demanding higher premiums for accepting higher risk. However, higher yields also offer opportunities for fixed income investors to add additional sources of income return to their portfolio by identifying bonds that have been mispriced based on perceived risks despite strong fundamentals at the issuer level.

The importance of credit selection

To benefit from higher yields while managing downside risk, credit selection has become increasingly important, particularly as dispersion within corporate earnings by sectors and issuers has increased.

Case-in-point: In May, U.S. large cap stocks exhibited a notable difference in earnings – the highest since 2020 – due to a rebound in tech stocks and a decline in many other sectors during the month.

This example is a case where active management can shine and where experienced credit researchers and portfolio managers can make distinctions to identify opportunities for return and protect against downside risk.

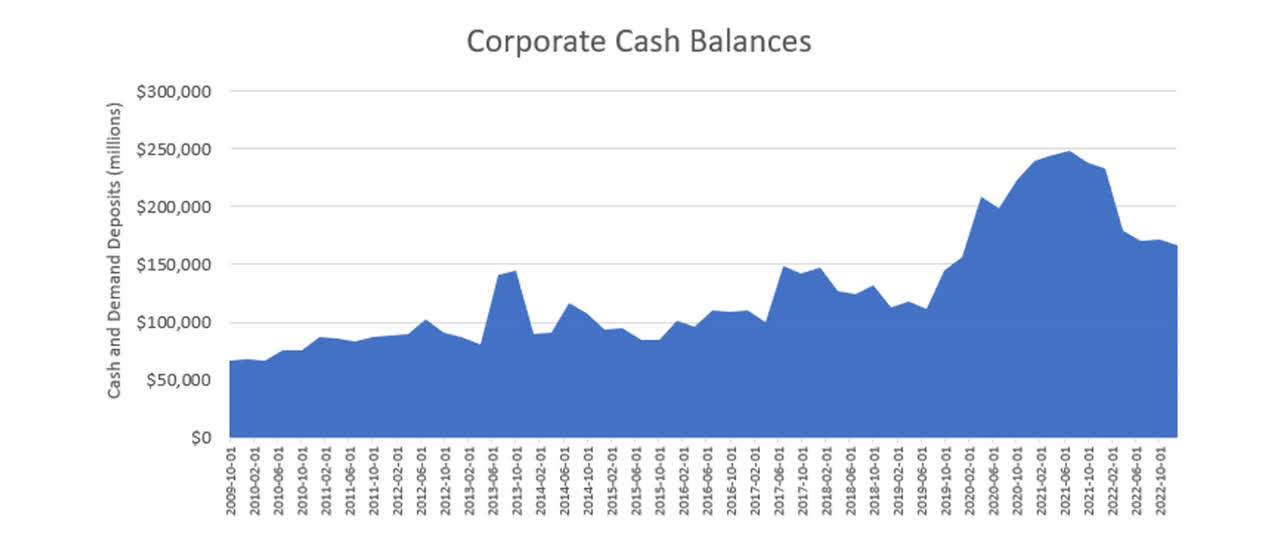

Additionally, while lending standards have tightened since 2021, corporate cash balances have also started to decrease, which is a key indicator of companies’ ability to service and repay debt. However, balances still remain well above historical levels:

Source: Federal Reserve Economic Data, Federal Reserve Bank of St. Louis

The bottom line

While higher yields offer more income potential, risks remain in fixed income markets. Amid this backdrop, we see active management as increasingly crucial in effectively navigating market volatility while also capturing opportunities. Ultimately, we believe skilled managers are well-equipped to help investors optimize their fixed income portfolios while minimizing potential downside risks.

Disclosures

These views are subject to change at any time based upon market or other conditions and are current as of the date at the top of the page. The information, analysis, and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual or entity.

This material is not an offer, solicitation or recommendation to purchase any security.

Forecasting represents predictions of market prices and/or volume patterns utilizing varying analytical data. It is not representative of a projection of the stock market, or of any specific investment.

Nothing contained in this material is intended to constitute legal, tax, securities or investment advice, nor an opinion regarding the appropriateness of any investment. The general information contained in this publication should not be acted upon without obtaining specific legal, tax and investment advice from a licensed professional.

Please remember that all investments carry some level of risk, including the potential loss of principal invested. They do not typically grow at an even rate of return and may experience negative growth. As with any type of portfolio structuring, attempting to reduce risk and increase return could, at certain times, unintentionally reduce returns.

The information, analysis and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual entity.

Frank Russell Company is the owner of the Russell trademarks contained in this material and all trademark rights related to the Russell trademarks, which the members of the Russell Investments group of companies are permitted to use under license from Frank Russell Company. The members of the Russell Investments group of companies are not affiliated in any manner with Frank Russell Company or any entity operating under the “FTSE RUSSELL” brand.

The Russell logo is a trademark and service mark of Russell Investments.

This material is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Russell Investments. It is delivered on an “as is” basis without warranty.

UNI-12267

Original Post

Read the full article here

")

2026-02-11")

")

")

")