")

Company Snapshot

EZCORP, Inc. (NASDAQ:EZPW) is a small-cap stock (~$600m market-cap), known primarily for its pawn loan activities in the US (it is the second biggest pawn loan entity in the nation, at least by store count) and Latin America. In total the company operates close to 1,250 stores across both regions. Besides the core activity of pawn loans (pawn service charges account for 63% of total group gross profit), EZPW also sells merchandise, which largely consists of the collateral initially pawned and then forfeited by its clients.

A Good Environment for Pawn Activities.

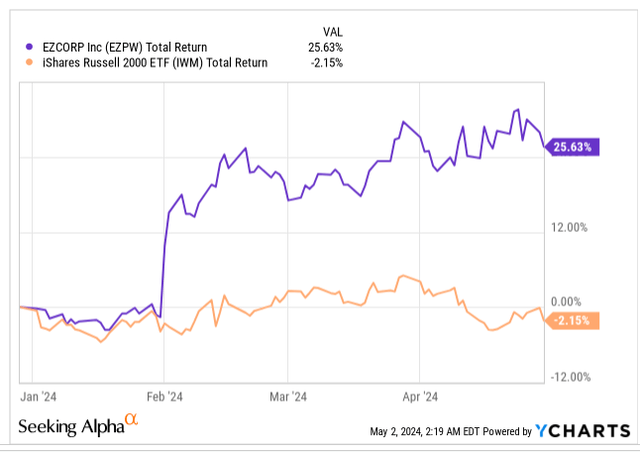

Note that over the last six months, EZPW’s stock has been in fine fettle with its price jumping over 25%, even as its peers from the small-cap space have eroded wealth.

YCharts

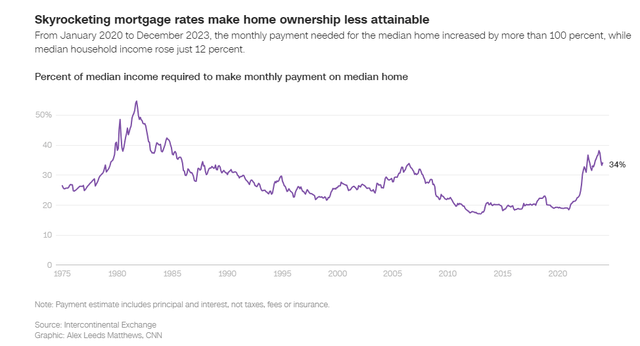

EZPW’s popularity in the current environment is quite understandable, given the underlying cost of living conditions that are currently prevalent across the nation.

Interest rates in the US are now at two-decade highs, and yesterday the Federal Reserve implied that, there wouldn’t be any light at the end of the tunnel any time soon. Before the pandemic, only around 20% of median income used to go towards monthly payments related to home ownership. These days well over a third goes to this endeavor, leaving US citizens with less disposable income to meet other rainy-day needs.

ICE

It isn’t just homeowners who are grappling with tighter budgets; at least their net worth is in decent shape (the median net worth of a homeowner is 38x that of a renter; for context in 1992, it was lower at 30x). But consider the situation of renters (estimated to be 35% of US households as per the Census Bureau), who are typically perceived to be further down the income strata. Rent prices are now 30% higher than the pre-pandemic era, and around half of these renters are spending over 30% towards rent and utilities.

Then America’s infant population continues to grow, but infant childcare expenses are growing at a rapid pace (the price of a nanny for a single infant has grown by 35% from 2019), eroding budgets even further. There are plenty of Americans who can’t even afford to resort to external childcare; currently close to 40% of infants live in households with incomes that are less than 2x the Federal Poverty Line.

Amidst all this, it also looks like Americans don’t have a great deal of savings stocked up, that would otherwise have served as a useful buffer. For context, as of March, the personal savings rate stood at a lowly figure of just 3.2%, over 500bps lower than the long-term average of 8.5%

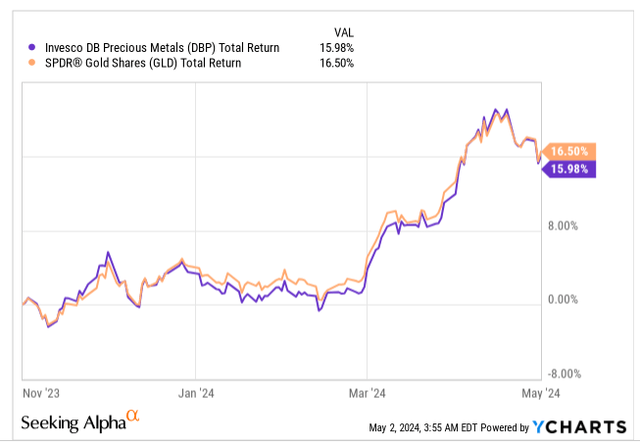

Amidst all these cost of living challenges, where spare cash is also scarce, you also have a situation where precious metal momentum is quite high. For context, gold and other precious metal prices have seen an increase of mid-teens over the past six months.

YCharts

Under these circumstances, EZPW’s clientele will be incentivized to pawn their jewelry to meet their monthly budgets. For context, over the past couple of quarters, EZPW’s pawn loan outstanding (PLO), a gauge of business momentum, has been growing at a commendable annual pace of 13-14% per quarter. Note that well over two-thirds of EZPW’s US PLO consists of jewelry alone. Firstly, EZPW stands to gain from some rather elevated monthly interest rates that range from 12-25% across different regions, and even if its customer chooses not to redeem their pawned jewelry, EZPW is rather well placed to liquidate it quite efficiently, given the current appetite for precious metals.

Yet, EZPW May Not Make For A Great Buy Here

Broadly, the environment for pawn activities looks to be in good shape, but that doesn’t necessarily mean that one should buy this business at any price.

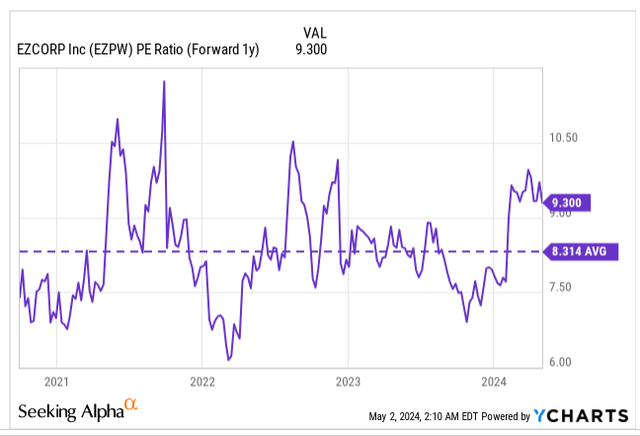

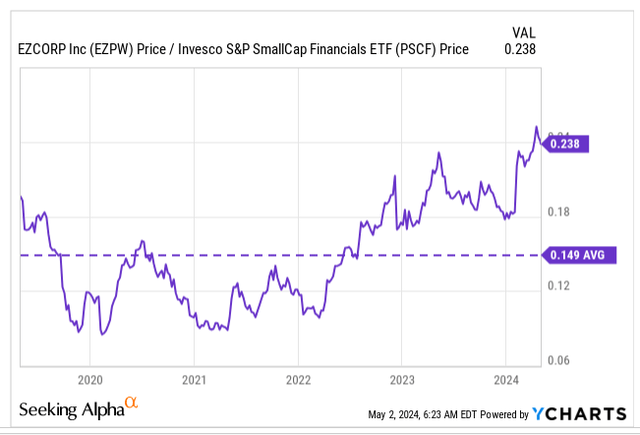

Firstly, it must be said that EZPW’s stock no longer offers great value at the current price. Based on consensus EPS estimates for FY25, the stock is now priced at a forward P/E of 9.3x, which represents a 12% premium over its long-term average.

YCharts

One could be open to paying that premium, if you were getting an improving cadence of earnings growth going forward, but that isn’t quite the case.

Lately, EZPW hasn’t been getting a great deal of operating leverage, as expense growth is coming in at a faster pace than topline growth. In Q2, revenue growth came in at 11%, but a higher store count, increased store labor expenses (Latam stores are also being impacted by minimum wage increases), and loyalty-related expenses all saw store expenses grow at a greater pace of 13%. EZPW’s share price has been growing in stature, but that also reflects quite strongly on the general and administrative cost base which rose by 17% in Q2. EZPW is also undergoing a digital transformation process with the aid of Workday, and costs related to this initiative are likely to double all through FY25.

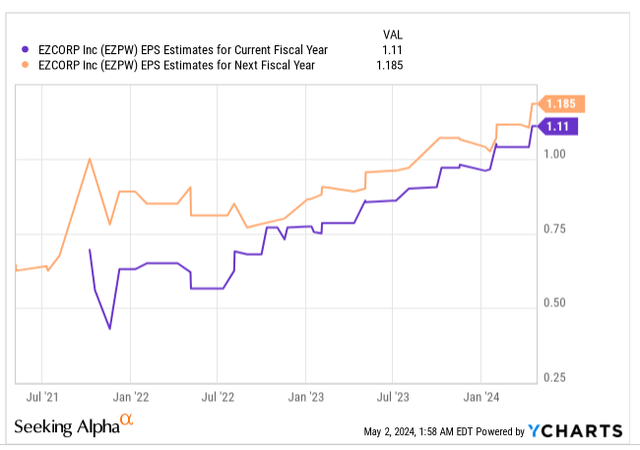

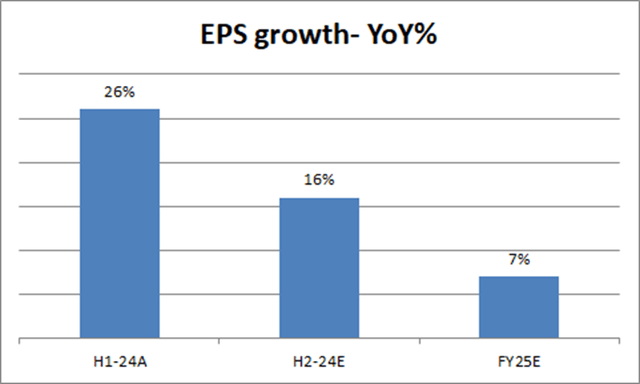

All in all, after delivering 26% EPS growth in H1, the implied earnings growth for H2 is likely to be 1000bps lower if one is going by FY24 EPS consensus estimates of $1.11 (the FY23 adjusted diluted EPS was $0.92).

YCharts

Crucially, EPS estimates for FY25 suggest a drastic slowdown in the bottom line growth, with an implied figure of only 7%.

YCharts

What investors also need to consider is that some of EZPW’S non-jewelry related inventory (handbags and the like) won’t find too many takers in the current environment, where sellers appear to be dwarfing the buyers. Admittedly it’s fair to say that EZPW isn’t necessarily staring at a glut of inventory, unlike some of its peers, but getting rid of aged inventory (inventory of over one year) is not going to be easy without taking a hit on the merchandise margin. For context, in the US, aged inventory which stood at just 1.1% in Q1, almost tripled, hitting levels of 3% in Q2, (driven mainly by a spike in luxury handbags).

Then, rotational specialists who focus on the small-cap financial space, are unlikely to have the EZCorp stock as one of the top names on their watchlist. We say this because EZPW’s relative strength versus other small-cap financials is at its highest point in five years, and around 60% higher than its 5-year average. Given this scenario, a few investors may choose to book profits and rotate towards other beaten-down small cap financials.

YCharts

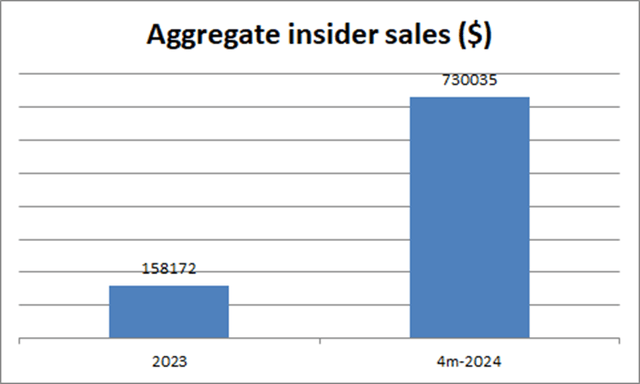

In fact it looks like some key insiders are very much looking to take profits at these relatively higher levels. For the whole of last year, we only saw aggregate discretionary insider sales to the tune of 158K. but this year, in just four months, we’ve already witnessed aggregate sales to the tune of $730K.

Barcharts

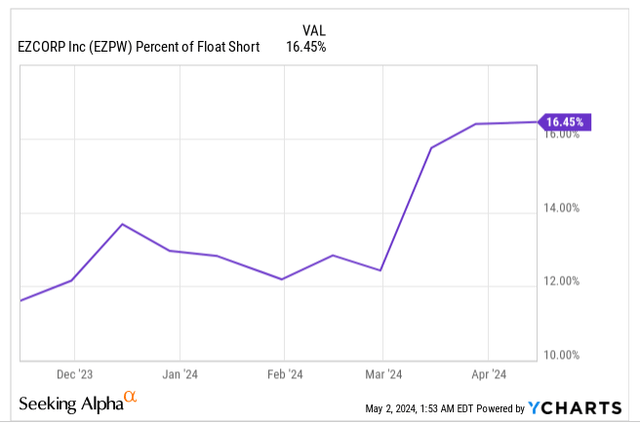

Separately, it’s also worth noting that bearish sentiment has gone up of late. Until March, the percentage of the float that was shorted hovered around the 12-14% level, but in recent months, we’ve seen a spike to the 16.5% levels.

YCharts

Finally, note that EZPW’s price movements over the last four years have happened within a certain ascending channel (two black lines), and it has generally helped if you buy the stock close to the lower boundary, and take profits when it gets closer to the upper boundary. We’ve seen four separate instances (area highlighted in yellow) where the stock has come close to the upper boundary and failed to break past. Regardless, given how far the stock is from the lower boundary of the channel, we don’t think the risk-reward is too conducive for a long position here.

Investing

Read the full article here

: Why I Changed My Mind Recently")

Q4 2026 Earnings Call Transcript")

")

")

")