")

As investors search for disruptive companies within the biotech sector, it is helpful to consider disruptive technologies that necessarily precede them. Specifically, the revolutionary CRISPR/Cas9 gene-editing platform has recently made headlines with FDA approval of a revolutionary drug named Casgevy. This therapy, pioneered by CRISPR Therapeutics (NASDAQ: CRSP), amazingly recognizes the correct segment of DNA to edit by using a piece of RNA as a guide.

The Cas9 protein then cuts the patient’s DNA chain, allowing for insertion of a new gene, in this case to remove a defective gene. The pioneering work that led to this powerful discovery was also awarded the Nobel Prize for Chemistry in 2020. In case you were unaware, one of the Nobel-winning scientists, named Charpentier, is also a scientific founder of CRISPR Therapeutics.

CRISPR acquired exclusive rights to intellectual property encompassing CRISPR/Cas9, massively accelerating the promise of academic research into clinical practice. The science behind CRISPR has been developing for years and several companies have emerged to capitalize and bring new therapies to patients, including: CRISPR Therapeutics (CRSP), Editas Medicine (EDIT), Intellia Therapeutics (NTLA) and Beam Therapeutics (BEAM). As mentioned above, the first FDA approved CRISPR/Cas9 therapy, named Casgevy, was developed by CRISPR Therapeutics and was designed to treat sickle cell disease (SCD). It was approved in November 2022 and discovered through a collaboration between Vertex (VRTX) and CRISPR Therapeutics.

Investors looking for a less speculative play in the CRISPR space would be well-advised to research Vertex: a large-cap biotechnology company with robust cash-flows from approved and commercialized therapies and drugs. However, a more aggressive play would be investing directly in CRISPR Therapeutics. CRISPR has a much smaller enterprise value than Vertex, $3.38B vs. $92.38B respectively. As such, CRISPR will be much more leveraged to the success or failure of Casgevy. As is often the case in the stock market, more risk equates to more reward, and an investment in CRISPR is a pure play on the emerging cash flows of Casgevy and other novel CRISPR/Cas9 therapies that may come to fruition.

What Does An Investment in CRISPR Entail?

CRISPR Therapeutics has accomplished the remarkable feat of having the first ex vivo CRISPR-Cas9 therapy. In addition, the therapy has been FDA approved for two indications: Vertex and CRISPR announced a new therapy for Sickle cell disease (SCD) and transfusion-dependent beta-thalassemia (TDT).

In other words, CRISPR’s ex-vivo CRISPR/Cas9 therapy Casgevy (exagamglogene autotemcel) has been approved by the FDA to treat TWO separate diseases: Sickle cell disease (SCD) & transfusion-dependent beta-thalassemia (TDT). SCD is inherited by having two genes encoding the disease, and is characterized by the presence of an abnormal form of hemoglobin. This leads to a distorted shape for the red blood cells of a person suffering from this serious disorder. Having the condition SCD can lead to sickle cell anemia, a chronic and potential deadly disease. TDT is also an inherited blood disorder, which affects hemoglobin. Thus, CRISPR’s attempt to ‘kill two birds with one stone’ is a wonderful strategy.

An interesting feature of CRISPR’s stock is that while both these treatments have been FDA approved, the stock has traded sideways for five years. As such, the market appears to be rather pessimistic about the commercialization of these therapies. After all, shouldn’t a stock trade higher as the commercial prospects for its therapies have obviously increased?

CRISPR Stock Chart – Past 5 Years (Google Finance)

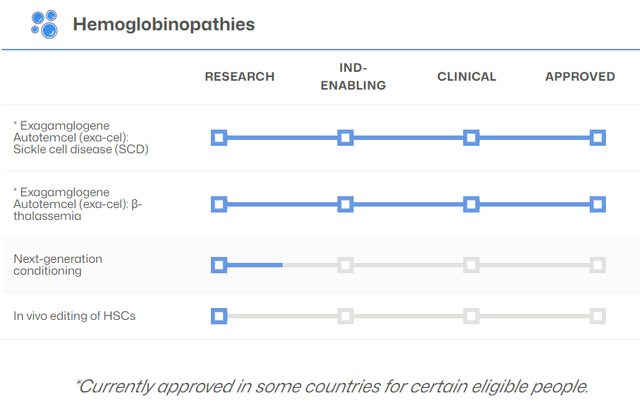

Both the programs listed above take an ex vivo approach, meaning that the cells are edited outside the human body prior to administering these gene-editing therapies to the patient. By contrast, an in vivo approach would entail delivery of a CRISPR-based therapeutic directly to the target cells within the human body. Perusing the website, this explains the pipeline: with the two approved indications relying on ex vivo treatment, which is necessarily more expensive. However, the company remains invested in in vivo editing, but that remains a long way off. In the clinical setting, CTX310 and CTX320 are being investigated but remain unapproved.

In total, this leads to a robust pipeline, including the approved treatments Casgevy, for SCD and TDT along with an exciting (but unproven) portfolio of approaches in CAR-T therapy and also the ‘holy-grail’ of in vivo gene editing.

CRSP Therapeutics Corporate Presentation (Investor Presentation – Page 3)

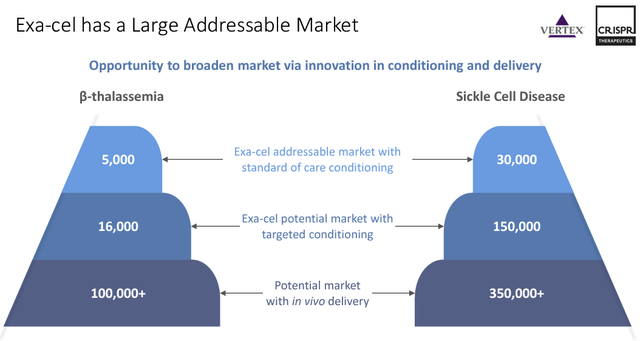

While ex-vivo treatment is an amazing proof of concept, in-vivo treatment would hugely expand the addressable market and substantially lower the therapies’ cost. According to the most recent investor presentation, the currently approved ex-vivo approach leads to an addressable market of 5,000 patients for TDT and 30,000 patients for SCD, respectively. The early stages of this therapy contribute to its massive cost, estimated to be approximately $2.2 million per patient.

CRISPR Pipeline for Hemoglobinopathies Only (CRSP Website)

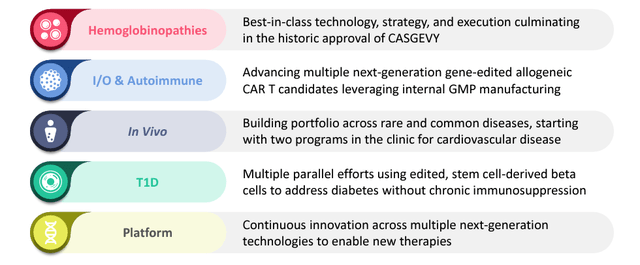

Readers are encouraged to peruse the pipeline listed on the company website. The graphic above relates only to the most recent advances and does not include: Immuno-Oncology & Autoimmune Diseases, In Vivo Approaches, Regenerative Medicine or Other Disclosed Partnered Programs, which may one day be as exciting as ex vivo gene editing for SCD and TDT.

However, even these two therapies have markets that will contribute meaningfully to creating shareholder value. SCD has a potentially addressable market of 30,000 persons, while TDT has 5,000 persons suffering from the disease.

CRSP Therapeutics Corporate Presentation (Corporate Overview: Q1 2024 Page 7)

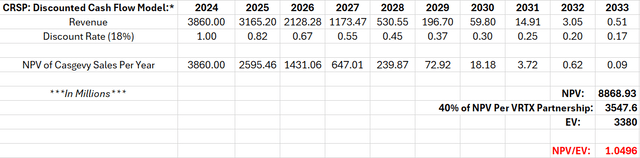

All this progress is incredibly exciting, however, can investors in CRISPR expect to be reasonably compensated? As an intellectual exercise, let us consider the net-present value (NPV) of only CRISPR’s approved therapies. Should they be reasonably valued, the rest of the pipeline could be had for free, leading to an exciting opportunity to invest in the future of human health, while also guarding against undue risk.

Let us consider the NPV of Casgevy, to accomplish this a number of considerations must be made:

- Total Addressable Market (TAM): if CRISPR could monetize all patients in the US and EU suffering from SCD and TDT (30,000 and 5,000 respectively) this would be the maximum Total Addressable Market (TAM)

- Market Penetration Rate (MPR): The maximum penetration rate will be highly dependent on societal acceptance, the cost of $2.2M per patient is prohibitive and may not be covered by insurance companies. Further complicating the analysis is, patients come from multiple geographic locations, which may not be inclined to reimburse for treatment.

- Pricing: The average price reported above is $2.2M per patient. Bear in mind: the cost of treating an SCD patient is $1.2M over a lifetime, while the price of treatment for a TDT patient is lower at $0.52M.

- Discount Rate: Considering the risk, the discount rate for biotechnology is applied (18%). For the purposes of this model, a high discount rate is applied because of the preponderance of risk factors above.

The major unknown for current financial modeling of CRISPR is the MPR: How many patients will be treated with its new ex-vivo drug Casgevy? SCD is a huge-unmet need and while existing treatments exist, they are expensive ($1.2M over the patient’s lifetime). The economic burden of TDT is lower: around $0.52M over a patient’s lifetime. Casgevy therapy is a cure, it edits the patient’s DNA permanently to solve either SCD or TDT. However, the long-term effects are as yet unknown. It may be possible that some as yet unknown risks could present itself.

A blended cost for SCD and TDT is:

- Sickle Cell Disease (SCD): $1.2M x 30,000 = $36B

- beta- thalassemia (TDT): $0.52M x 5,000 = $2.6B

- Totaling: $38.6B

In other words, if Casgevy is completely effective and equal in cost to current treatment options, the total spend on its implementation would total $38.6B (revenues due to the company over some time into the future). In this case, it seems less reasonable to estimate an MPR (based on complete unknowns) than to estimate an MPR as a percentage of the overall market that would justify the value of CRISPR Therapeutics. To be clear, this is the value of Casgevy alone! We are ignoring any value in the rest of the pipeline and simply concerning ourselves with how much revenue a therapy for SCD and TDT is worth given what healthcare payers are already reimbursing for it.

In other words, the two unknowns in our model (Pricing and MPR) can converge to a single value, the market share of Casgevy. What percentage of the $38.6B spent to treat SCD and TDT can be captured over time by these new therapies? Can this justify the purchase of CRISPR for its present enterprise value ($3.38B)?

With a high discount rate of 18%, imagine the implications of treating ALL patients over the next 10 years (i.e. spreading $38.6B in revenue over 10 years). In other words, $38.6B spent equally over 10 years and discounted by 18% per year generates an NPV of $8.868B. However, CRSP’s partnership with VRTX receives 40% of revenues, resulting in an adjusted NPV of $3.548B.

Thus, treating all SCD and TDT patients at their present cost to the system over 10 years would completely justify CRSP’s enterprise value. Again, please note: this is only the value of Casgevy.

CRSP: Discounted Cash Flow Model (Excel)

This assumption may be unduly optimistic in some respects and pessimistic in others:

Major Downside Risks:

- MPR Risk: The major risk is payers in the healthcare marketplace refusing to reimburse a seemingly astronomical $2.2M per treatment cost for Casgevy therapy. As such, our model assumed a blended cost equal to the present net cost of SCD and TDT patients to the healthcare system over the course of their lifetimes.

- Execution Risk: Patients may not be forthcoming to be treated with this exciting new therapy. There are very real ethical questions, particularly highlighted by the public’s fascination with the genetic editing of human embryos. Clearly, editing a gene from a sick patient is very different from editing the genes of a human embryo, but where will the line be drawn? Furthermore, months of hospitalization are required for the current ex vivo gene editing technique. A strong partnership with Vertex Pharmaceuticals somewhat offsets this risk.

- Profit-sharing: CRISPR has entered a partnership with Vertex Pharmaceuticals. As such, only 40% of profits for Casgevy will be retained, with the remaining 60% belonging to Vertex. The model has been adjusted to reflect this.

Potential Upside Benefits:

- DCF Valuation of Casgevy Alone Nearly Supports Valuation: CRISPR is a best-in-breed company with established partnerships and platform technology. The above valuation negates any value for the remaining portfolio beyond Casgevy. While a further review of the portfolio is too broad for this article, opportunities in: Immuno-oncology & Autoimmune Disease, In-Vivo CRISPR/Cas9 Therapy (the holy grail), Regenerative Medicine along with Other Undisclosed Partnerships could fuel growth well into the future.

- DCF Valuation Assigns only Cost: CRISPR’s costs include the future valuation of the company. Investing in the business through research and development (R&D) encompasses much of the cost in our DCF valuation above. If an investor believes that these endeavors will bear fruit, then this is money well spent.

- Is 40% of Casgevy worth $3.38B? Simple math indicates that 40% of a drug costing $2.2M per patient with 35,000 patients treated is $30.8B (if they were all treated today). Clearly, this is overoptimistic, but is 11.0% of this value realistic? Only time will tell, but CRISPR Therapeutics may have justified its present valuation with only its first FDA approved product.

- A Promising Pipeline: It must be emphasized that Casgevy is only the first successful commercialization of a rich pipeline. While costs to the first patients are astronomical, the promise of in vivo gene editing is invaluable. It is likely that Casgevy will not be the final commercialized product to be discovered in the labs of CRISPR Therapeutics.

The prospects of CRISPR Therapeutics draw historical parallels with Genentech, another pioneer in biotechnology that demonstrated the vast potential of recombinant DNA technology: the insertion of DNA encoding human proteins into bacteria to produce bioactive proteins. Genentech (once listed under the NASDAQ ticker: DNA), proved disruptive and hugely effective, leading to many therapies that were impossible to predict at the time.

CRISPR Therapeutics (CRSP), with its CRISPR/Cas9 platform, bears great similarities. The FDA’s approval of Casgevy proves the potential commercial application of its approach to gene-editing, a huge and exciting scientific milestone. This first fruit is the beginning of what should be a major cash-flow stream. Thus, Casgevy should satisfy the market’s insatiable demand for cash, while researchers at the company search for the holy grail of in vivo gene editing. Should this come to fruition, the rewards to investors today could be incredible.

Disclaimer: All investment opportunities carry inherent risk, including potential loss of principle. Carefully consider your investment objectives, level of experience and risk appetite before making any investment. The above discussion is a framework for assessing economic value, not a prediction, and should not be considered investment advice.

Read the full article here

: Why I Changed My Mind Recently")

Q4 2026 Earnings Call Transcript")

")

")

")