2026 Q1 – Results – Earnings Call Presentation (NASDAQ:ERIC) 2026-04-17")

")

")

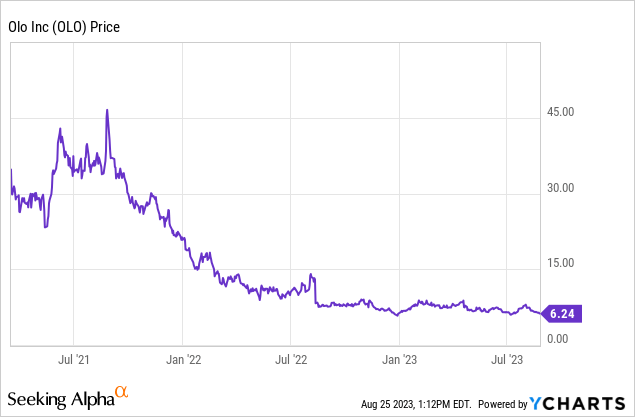

In case you are an investor looking to put some money at work into the digital transformation of the restaurant industry then Olo Inc. (NYSE:OLO) may be the stock you’re looking for and this thesis aims to assess whether the current price of $6.24 constitutes a suitable entry for those interested in investing.

In this regard, this SaaS, or Software as a Service company beat both revenue and non-GAAP EPS expectations when it reported its second quarter 2023 (Q2) financial results back on August 1. This is a remarkable achievement in view of the current macro-level economic uncertainty as interest rates remain high while some level of inflation still percolates in the system.

I start by providing insights as to how the company operates within the industry and the products it offers with the objective of assessing whether good results can be sustained going forward.

Digitally Transforming the Industry

First, the restaurant industry is one which is characterized by a lot of margin pressure, as, on the one hand, the prices of ingredients like food, vegetables, and meat, have increased rapidly during the last two years because of rising inflation. On the other hand, there is also wage inflation, which makes labor costs expensive, but, this is not an industry where you can easily replace human beings with automated processes as in Information Technology. As a result of these two factors, restaurants, and other takeaway owners tread on a thin line, constantly trying to balance revenues with costs in order to continue generating sufficient profits, sometimes just enough to survive.

In these circumstances, any means to improve operations while not increasing HR costs while at the same time ensuring that the service level is maintained tends to be most welcome.

Olo’s Website (www.olo.com)

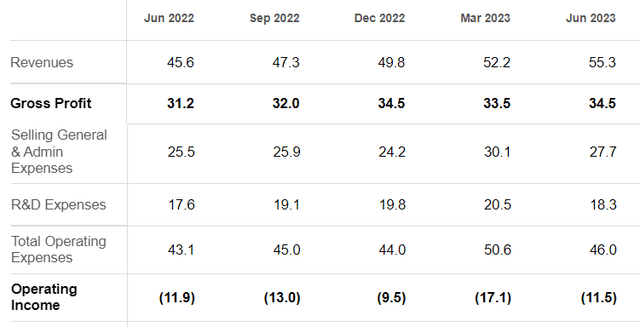

This explains the success of Olo’s three main modules, which consist of Order, Pay, and Engage, and, their rapid adoption has translated into revenues of $55.3 million in Q2 or a 21% YoY increase. More importantly and from a profitability standpoint for this loss-making company (on a GAAP basis), its products have enjoyed better penetration within its existing customer base which has resulted in higher average revenue per user or ARPU of $716, which represents a 32% year-on-year surge.

Now this ability to drive more product usage within the existing customer base means relatively less effort and expenses to win new ones, in turn resulting in higher gross profits as shown below. Trickling down the income statement, these have partly offset the operating expenses, in turn reducing losses from $11.9 million to $11.5 million in the latest reporting quarter.

Income Statement (seekingalpha.com)

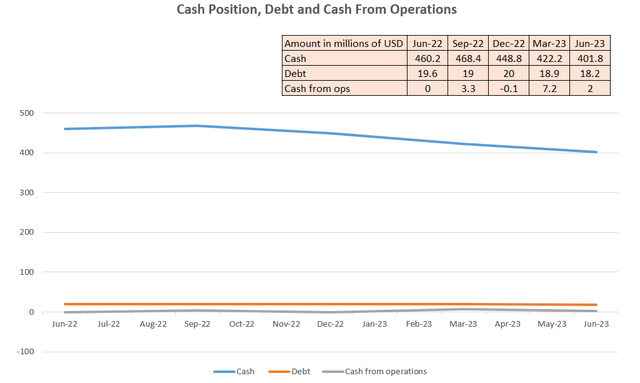

However, with $402 million of cash in the balance sheet, and the company still having to spend for growth in view of the competition, it is important to assess whether there is a clear path to profitability.

Profitability and Competition

First, encouraged by the traction for its products, Olo has raised revenue guidance for the third quarter of 2023 (Q3) to $56.3 million (mid-point) which would represent a 19% growth over Q3-2022. Second, after investing in sales and marketing in the first half of the year to meet the needs of enterprises as well as investing in the development of more specialized features for its software modules (Pay, Order, and Engage) more modest progression in expenses is anticipated for the rest of 2023. As a result, there should be an improvement in margins.

Singling out the Engage module, the company is leveraging historical data to more accurately profile diners and their habits so that Olo’s clients can recommend to them the most appropriate dining experience. An example is California Pizza Kitchen combining Olo’s guest data platform and sentiment analysis to boost customer loyalty for its casual dining chain. Remaining in the same business line, Denny’s has deployed the marketing automation platform to promote guest engagement.

Now, these two are classified as enterprise clients which means that Olo is progressing beyond its traditional customer base of individually-owned restaurants towards franchises and dining chains. As such, it now competes with big players like Zendesk (ZEN) whose services also promote long-term relationships with diners by effectively responding to praise or complaints, and recording who made them.

Thinking aloud in today’s highly dynamic IT world, Olo’s customers do have the possibility of directly subscribing to Microsoft’s (MSFT) Azure, Amazon’s (AMZN) AWS, or even Salesforce (CRM)’s cloud to lease IT services and take advantage of the OPEX-based charging model. However, this distracts them from focusing on core restaurant operations like customer retention. Also, smaller restaurant owners do not have the financial clout of the likes of Chipotle Mexican Grill (CMG) which have their own IT teams to deploy cloud, analytics, data lake, and AI across their restaurants.

This ultimately means that in an industry that has historically been resistant to change and operates with relatively lower margins, Olo is appropriately positioned with its SaaS products to help both smaller restaurant owners and now larger dining chains gain access to data-driven customer experience solutions, which are the very basis for moving towards AI and ML (machine learning).

Looking at the financial model, it has not been profitable using GAAP metrics, but, Olo still generates cash from operations while debt has been kept below the $20 million level as shown below.

Table and Charts Built Using data from (www.seekingalpha.com)

Now, since the enterprise business category is normally synonymous with better margins compared to small and medium-sized ones, this is one of the reasons why the company has upgraded its full-year 2023 non-GAAP operating income in the range of $17 million and $17.8 million up from the projection of $11.4 million, and $13 million in February.

Valuing the Company

The second reason for the upgrade is cost reduction mainly relating to R&D, and reattributing some of the savings to support strategic priorities. It is precisely by using the strategic perspective that I value the company, not simply doing an academic comparison with peers to find out that it is overvalued.

To this end, Olo is not only gaining market share through promoting the use of existing products across the industry but at the same time creating new ones in order to take on opportunities, associated with the path towards 100% digitalization in the restaurant industry, as per its CEO. Thus, from OrderReady AI, an ML-based tool for identifying more accurate quote times to Olo Engage which leverages Generative AI for marketing purposes, the company has been innovating. Also, its revenue growth rate of 21% is three times the expected compound annual growth rate of about 6.7% for the hotel and hospitality management software between the 2021 and 2028 period to reach $4.9 billion.

Therefore, it deserves better valuations in my view.

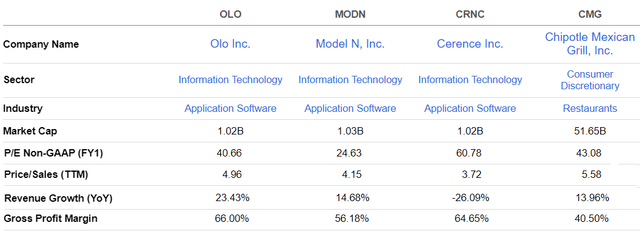

For this purpose, I perform a comparison with Model N (MODN) and Cerence (CRNC) which provide cloud-based solutions for life sciences and mobility/transportation markets respectively. For comparison with the Consumer Discretionary sector, I have also listed Chipotle which also forms part of the restaurant industry.

Now, Olo’s gross margins exceed all others as illustrated below. Thus, considering its lower Price-to-Earnings multiple of 40.66x with respect to Chipotle’s 43.08x, I obtain a target of $6.61 (43.08/40.66 x 6.24) based on its current share price of $6.24. This represents only a 6% upside.

Comparison of Key Metrics (www.seekingalpha,com)

Investors will also note that I have refrained from using the price-to-sales multiple of 4.96x for valuing the stock, which would have resulted in a higher target. This has been done deliberately for two reasons.

First, looking at momentum indicators, the 50-day and 200-day moving averages all being higher than the share price hint that the downtrend could continue. Second, while the economy continues to be resilient this year, even in light of aggressive interest rate hikes as of 2022, with the Federal Reserve having seen a large degree of success in its fight against inflation, the victory is not yet final. Here, a scenario including a mild recession is not excluded, and, in case this materializes would primarily impact the Consumer Discretionary sector to which Olo has deep exposure.

In conclusion, despite showing an operating loss status on a GAAP basis, Olo remains financially healthy as it generates cash, has relatively little debt, and is growing in a sustainable fashion with its high ARPU. However, due to the risks I have mentioned above, there could be a downside to the $6 support level if economic conditions were to deteriorate as the latest update from Jackson Hole indicates that more hikes are expected as the Fed maintains its 2% inflation target. Thus, I have a hold position on the stock, but, this remains a strong company to put on your watchlist.

Read the full article here

2026 Q1 – Results – Earnings Call Presentation (NASDAQ:ERIC) 2026-04-17")

")

")